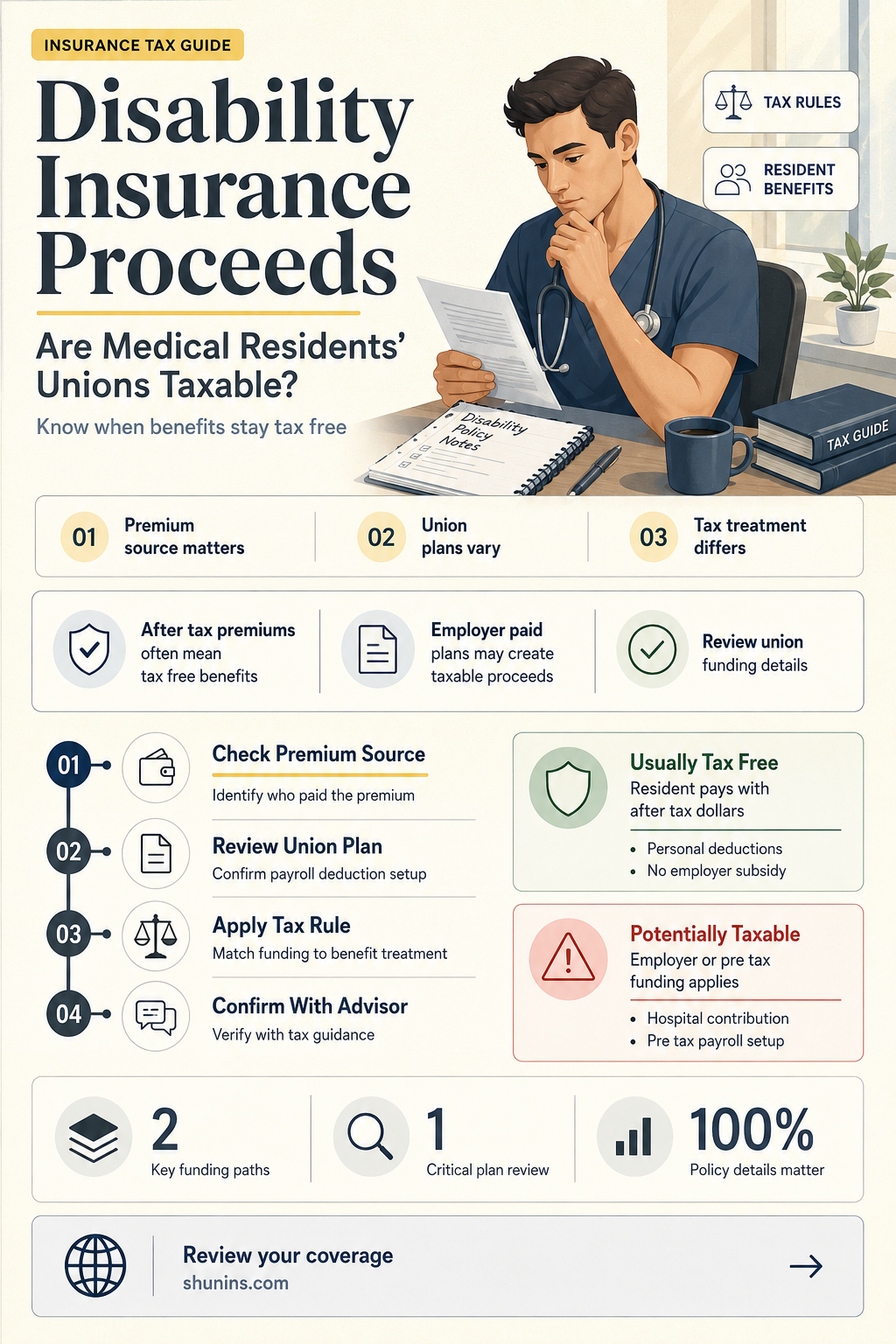

Whether disability insurance proceeds are taxable depends on several factors, including the type of coverage, how it was paid for, and the nature of the disability. In the United States, disability insurance provides financial protection for those who are unable to work due to injury or illness, with benefits varying based on the length of the disability. Short-term disability insurance typically covers disabilities that keep individuals out of work for a few weeks or months, while long-term disability insurance is designed for more permanent conditions. The taxation of benefits depends on whether premiums were paid with pre-tax or post-tax dollars, with pre-tax premium payments making benefits taxable and post-tax premium payments resulting in tax-free benefits. Additionally, certain expenses, such as out-of-pocket medical costs, may be deductible. So, are disability insurance proceeds for medical residents union taxable?

Explore related products

What You'll Learn

- Are disability insurance proceeds taxable if paid with pre-tax dollars?

- Are disability insurance proceeds tax-free if paid with post-tax dollars?

- Are short-term disability insurance proceeds taxable?

- Are disability insurance proceeds taxable if paid by the employer?

- Are disability insurance proceeds taxable if paid by the employee?

![]()

Are disability insurance proceeds taxable if paid with pre-tax dollars?

Whether or not disability insurance proceeds are taxable depends on the source of the disability income and the nature of the insurance policy. If you pay the entire cost of a health or accident insurance plan with pre-tax dollars, you do not need to include any amounts received for your disability as income on your tax return. However, if you pay the premiums of a health or accident insurance plan through a cafeteria plan and did not include the premium amount as taxable income, the premiums are considered paid by your employer, and the disability benefits are fully taxable.

If both you and your employer have paid the premiums for the plan, only the amount you receive for your disability that is attributable to your employer's payments is reported as income. Disability benefits from a policy you bought yourself with after-tax dollars or an employer-sponsored policy you contributed to with after-tax dollars are also not taxable. These rules apply to both short-term and long-term disability policies.

If you receive disability benefits through an accident or health insurance plan paid for by your employer, you must report as income any amount you receive for your disability. Amounts received from your employer while sick or injured are considered part of your salary or wages. You can generally exclude from income payments received from qualified long-term care insurance contracts as reimbursement of medical expenses for personal injury or sickness under an accident and health insurance contract. Additionally, certain accelerated death benefits received under a life insurance contract on the life of a terminally or chronically ill individual are excluded from income.

Navigating the tax treatment around disability payments can be complex, and it is always recommended to seek professional tax advice for specific situations.

Launching a Medical Insurance Company: Where to Begin

You may want to see also

Explore related products

![]()

Are disability insurance proceeds tax-free if paid with post-tax dollars?

Whether or not disability insurance proceeds are taxable depends on the source of the disability income. If you pay the premiums of a health or accident insurance plan with post-tax dollars, then the proceeds are generally not taxable. This includes a policy you bought yourself with after-tax dollars or an employer-sponsored policy that you contributed to with after-tax dollars. However, if you pay the premiums of a health or accident insurance plan through a cafeteria plan and did not include the amount of the premium as taxable income, the premiums are considered paid by your employer, and the disability benefits are fully taxable.

If you receive disability benefits from an employer-sponsored disability insurance policy, worker's compensation plan, or Social Security disability, the benefits may be taxable depending on your provisional income. If your provisional income is more than the base amount, up to 50% of your Social Security disability benefits will generally be taxable. The base amount is $25,000 if you're filing single, head of household, or married filing separately (living apart all year). If your provisional income is more than the adjusted base amount, up to 85% of benefits will be taxable. The adjusted base amount is $34,000 if you're filing single, head of household, or married filing separately (living apart all year). It is important to note that income from a worker's compensation fund is not taxable if it is compensation for an on-the-job injury or sickness.

Medicaid and Copays: Understanding Primary Insurance Coverage

You may want to see also

Explore related products

![]()

Are short-term disability insurance proceeds taxable?

Whether short-term disability insurance proceeds are taxable depends on how and when the payments were made. If you received short-term disability payments under an insurance policy, these are not exempt, but you may not be liable for additional taxes if you have already borne the cost of taxation through the plan.

If your employer pays 100% of the premiums, all your short-term disability income is taxable. If you decide to split premium payments with your employer, there are two possible outcomes. If the premiums are automatically deducted from your paycheck, you may have to pay taxes on your portion of the short-term disability benefits. However, if you pay your share of the premiums with after-tax dollars, half of the benefit would be taxed. If you and your employer share the cost of a disability plan, you are only liable for taxes on the amount received due to payments made by your employer. If the amount of the premiums is paid by your employer or by you with before-tax dollars, you generally need to report any payments received as taxable income. Reimbursements for medical care are not taxable but may reduce the amount of any medical costs deduction.

You can submit a Form W-4S, Request for Federal Income Tax Withholding From Sick Pay to the insurance company or make estimated tax payments by filing Form 1040-ES, Estimated Tax for Individuals. Amounts you receive from your employer while you're sick or injured are part of your salary or wages. Report the amount you receive on the line "Total amount from Form(s) W-2, box 1" on Form 1040, U.S. Individual Income Tax Return or Form 1040-SR, U.S. Tax Return for Seniors. You must include in your income sick pay from any of the following: ... You can generally exclude from income payments you receive from qualified long-term care insurance contracts as reimbursement of medical expenses received for personal injury or sickness under an accident and health insurance contract. Also, you can exclude from income certain payments received under a life insurance contract on the life of a terminally or chronically ill individual (accelerated death benefits).

Understanding HMO and PPO Insurance: Key Differences Explained

You may want to see also

![]()

Are disability insurance proceeds taxable if paid by the employer?

Whether or not disability insurance proceeds are taxable depends on several factors, including the source of the income, who paid the premiums, and the type of insurance policy.

If you receive disability benefits through an accident or health insurance plan paid for by your employer, you must report as income any amount you receive for your disability. However, if you pay the entire cost of a health or accident insurance plan yourself, you do not need to include any amounts you receive for your disability as income on your tax return. If both you and your employer have paid the premiums for the plan, only the amount you receive that is attributable to your employer's payments is reported as income.

If you pay the premiums of a health or accident insurance plan through a cafeteria plan and you did not include the amount of the premium as taxable income, the premiums are considered paid by your employer, and the disability benefits are fully taxable. Amounts you receive from your employer while you are sick or injured are considered part of your salary or wages and must be reported as income on your tax return.

It is important to note that disability insurance can come from different sources, such as a disability insurance policy, an employer-sponsored disability insurance policy, a worker's compensation plan, or Social Security disability. Each of these sources may have different tax implications, so it is essential to review the specific rules and regulations that apply to your situation.

Summit Medical Group: Insurance Coverage and Acceptance Details

You may want to see also

![]()

Are disability insurance proceeds taxable if paid by the employee?

Whether or not disability insurance proceeds are taxable depends on who paid the premiums for the plan. If you pay the entire cost of a health or accident insurance plan, you do not need to include any amounts you receive for your disability as income on your tax return. However, if both you and your employer have contributed to the cost of the plan, you must report as income any amount you receive for your disability that's due to your employer's payments. If you pay the premiums of a health or accident insurance plan through a cafeteria plan and you didn't include the amount of the premium as taxable income to you, the premiums are considered paid by your employer, and the disability benefits are fully taxable.

Disability insurance can be provided by your employer or bought by yourself from an insurance company. Disability benefits may or may not be taxable. You will not pay income tax on benefits from a disability policy where you paid the premiums with after-tax dollars. This includes a policy you bought yourself with after-tax dollars or an employer-sponsored policy you contributed to with after-tax dollars. These rules apply to both short-term and long-term disability policies.

If the amounts are taxable, you can submit a Form W-4S, Request for Federal Income Tax Withholding From Sick Pay to the insurance company or make estimated tax payments by filing Form 1040-ES, Estimated Tax for Individuals. Amounts you receive from your employer while you're sick or injured are part of your salary or wages. Report the amount you receive on the line "Total amount from Form(s) W-2, box 1" on Form 1040, U.S. Individual Income Tax Return or Form 1040-SR, U.S. Tax Return for Seniors. You must include in your income sick pay from any of the following: ... You can generally exclude from income payments you receive from qualified long-term care insurance contracts as reimbursement of medical expenses received for personal injury or sickness under an accident and health insurance contract. Also, you can exclude from income certain payments received under a life insurance contract on the life of a terminally or chronically ill individual (accelerated death benefits).

Medical Malpractice Insurance: Understanding the Cost of Coverage

You may want to see also

Frequently asked questions

If you paid the premiums with pre-tax dollars, then your disability income is taxable.

If you paid the premiums with post-tax dollars, then your disability income payments are free from federal taxes.

If your employer pays the premiums, the IRS considers those premium payments to be untaxed income. So, taxes will be deducted from your benefits.

Life insurance proceeds received as a beneficiary due to the death of the insured person are generally not includable in gross income and you don't have to report them.