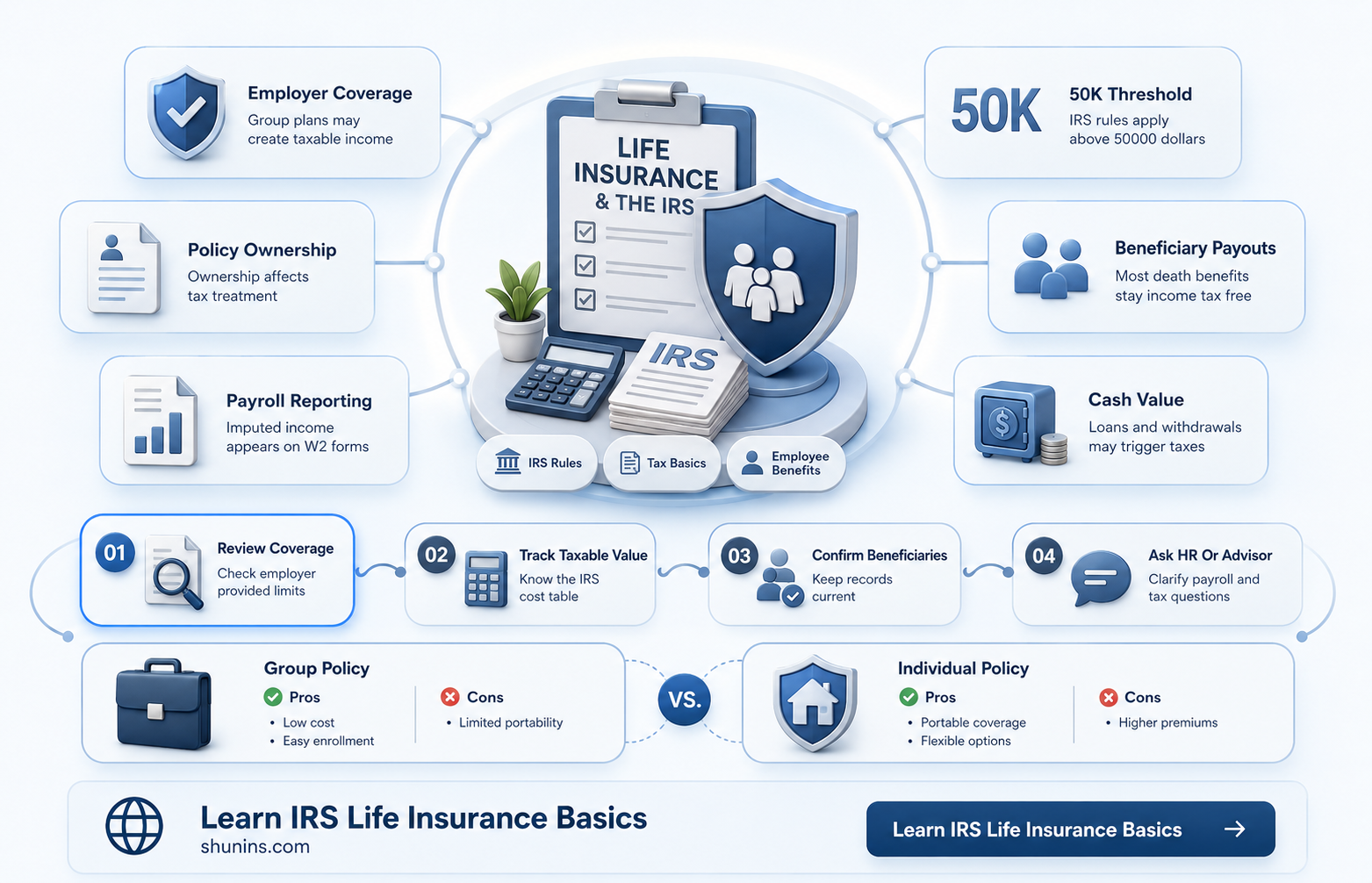

Life insurance is a financial product that provides a lump-sum payout to beneficiaries upon the death of the insured. While the proceeds of life insurance are generally not taxable, there are certain situations where taxes may apply. For instance, if the policy was transferred for cash or other valuable consideration, the exclusion for proceeds may be limited. Additionally, if the beneficiary receives the payout in installments, any interest accrued on those payments is typically taxable. Understanding the tax implications of life insurance is crucial, especially when an employer provides coverage as part of a compensation package. In such cases, the portion of the premium paid on policy amounts exceeding $50,000 is generally considered taxable income for the employee.

| Characteristics | Values |

|---|---|

| Are employee life insurance proceeds taxable? | Generally, life insurance proceeds received as a beneficiary due to the death of the insured person are not includable in gross income and do not need to be reported to the IRS. |

| Are there any exceptions? | Any interest received on the proceeds is taxable and should be reported. If the policy was transferred for cash or other valuable consideration, the exclusion for the proceeds is limited to the sum of the consideration paid, additional premiums paid, and certain other amounts. |

| What if the employer pays for the life insurance? | If the employer pays for life insurance coverage exceeding $50,000, the premium paid on the amount above $50,000 is considered part of the employee's taxable income. |

| Are life insurance premiums tax-deductible? | Life insurance premiums are not usually tax-deductible. However, they may be deductible as a business expense if you are not directly or indirectly a beneficiary of the policy. |

Explore related products

What You'll Learn

![]()

Interest on life insurance proceeds is taxable income

Generally, life insurance proceeds are not taxable if you receive them as a beneficiary following the insured person's death. However, if you receive interest on these proceeds, it is considered taxable income and must be reported. This means that if you choose to receive the life insurance payout in instalments instead of a lump sum, any interest accumulated on those payments is subject to tax.

The interest earned is reported to the Internal Revenue Service (IRS) by the insurance company and is taxable to the beneficiary. While the death benefit itself is typically not taxed, the interest that builds up on those payments is treated as regular taxable income. Therefore, beneficiaries should be prepared to report this interest on their tax returns.

It is important to note that there are some exceptions to the rule that life insurance proceeds are non-taxable. One exception is when the policy was transferred to the beneficiary for cash or other valuable consideration. In this case, the exclusion for the proceeds is limited to the sum of the consideration paid, additional premiums paid, and certain other amounts.

Renewing Your Massachusetts Life Insurance License: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Death benefit to the estate may trigger estate taxes

Death benefits from life insurance policies are not subject to ordinary income tax, but they may be subject to federal or state estate tax if the death benefit is paid to the estate and exceeds the estate tax exemption amount. The estate tax exemption amount is generally equal to the filing requirement. For 2023, the basic exclusion amount is $12,920,000.

The federal estate tax return doesn’t generally need to be filed unless the total value of lifetime transfers and the estate is worth more than the basic exclusion amount for the year of death. However, a complete and timely filed return is required if a deceased spouse’s estate elects portability of any unused exclusion amount for use by the surviving spouse.

The death benefit is a payout to the beneficiary of a life insurance policy, annuity, or pension when the insured person or annuitant dies. With life insurance policies, death benefits are not usually subject to income tax and named beneficiaries typically receive the death benefit as a lump-sum payment.

Death benefits from pensions are treated differently from benefits from life insurance policies, and they may be subject to taxation.

While life insurance death benefits paid in a lump sum are not subject to ordinary income tax, if the beneficiary receives the death benefit in installments that include interest, then the interest will be taxable.

Zoloft Use: Life Insurance Impact and Implications

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Cash value withdrawals exceeding premiums paid are taxable

If you are a beneficiary receiving life insurance proceeds due to the death of the insured person, you generally do not need to include them in gross income and don't have to report them to the IRS. However, if you are the policy holder who surrendered the life insurance policy for cash, and the amount you received is more than the cost of the policy, then the cash value withdrawals exceeding premiums paid are taxable.

The IRS treats life insurance differently from other types of financial products because it is intended to support one's beneficiaries. The tax rules vary depending on the type of life insurance plan and the specific situation. For example, if you receive life insurance proceeds as a beneficiary, they are generally not taxable. However, if you choose to receive the payout in installments, any interest that accumulates on those payments is considered taxable income. On the other hand, if you are the policy owner and you surrender your policy, the cash surrender value (CSV) may be higher than the amount of premiums you paid. In this case, the excess amount is taxable as ordinary income.

It's important to note that if your employer pays for your life insurance, the premium paid on policy amounts above $50,000 is considered part of your taxable income. Additionally, if you have a whole life insurance policy, the interest generated is not taxed until the policy is cashed out. When you cash out, you will pay taxes on the difference between the cash value received and the total amount of premiums paid.

To summarize, while life insurance proceeds received as a beneficiary due to the death of the insured are generally not taxable, cash value withdrawals exceeding premiums paid are considered taxable income. It's important to carefully review your specific policy and consult with a tax professional to understand the tax implications of your life insurance plan.

Life Insurance: Cashing in While Still Alive?

You may want to see also

Explore related products

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![]()

Life insurance proceeds are not taxable income

Life insurance is intended to provide financial support to your beneficiaries after your death. The IRS treats it differently from other types of financial products.

However, there are some exceptions and special cases to be aware of. If you receive interest on the life insurance proceeds, this is considered taxable income and must be reported. Additionally, if the policy was transferred to you for cash or other valuable consideration, the exclusion for the proceeds may be limited, and you may need to report a taxable amount.

Furthermore, if your employer pays for your life insurance, the premium paid on policy amounts above $50,000 is considered part of your taxable income. This is because the IRS considers it a taxable fringe benefit when the total amount of coverage provided by the employer exceeds this threshold.

In the case of group-term life insurance, the first $50,000 of coverage provided by an employer is excluded from taxation. However, if the coverage exceeds this amount, the imputed cost of coverage in excess of $50,000 must be included in the employee's income and is subject to social security and Medicare taxes.

It is important to carefully review your life insurance policy and understand the tax implications to ensure that your beneficiaries receive the full benefit without unexpected tax complications.

Term Life Insurance: 20-Year Policy Explained

You may want to see also

Explore related products

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)

![]()

Life insurance premiums are not tax-deductible

Life insurance premiums are generally not tax-deductible. The IRS considers them personal expenses, and only in rare instances are they deductible. For example, if you are a business owner offering life insurance to your employees, you can write off those premiums as a business expense.

Other instances where life insurance premiums can be tax-deductible include:

- If you donate your policy to a charity.

- If you have an alimony agreement that went into effect before 2019 that requires you to pay for life insurance on your ex-spouse.

- If you are a small business owner offering group life insurance to employees.

- If you are a business owner with a 162 Executive Bonus Plan, where you can deduct premiums for individual coverage on a key employee if that employee reports the premium as taxable income.

It is important to consult with a tax professional to determine if your life insurance premiums are deductible, as there are many variables that can affect the tax implications of your policy.

Prudential Life Insurance: Is It a Good Choice?

You may want to see also

Frequently asked questions

Generally, life insurance proceeds received as a beneficiary due to the death of the insured person are not includable in gross income and do not need to be reported to the IRS. However, if the policy was transferred to you for cash or other valuable consideration, the exclusion for the proceeds may be limited.

If you receive the life insurance payout in installments instead of a lump sum, any interest that builds up on those payments is considered taxable income.

If the policyholder leaves the death benefit to their estate instead of directly naming a person as the beneficiary, the estate's total value may trigger estate taxes.

If your employer pays for your life insurance, the premium paid on policy amounts above $50,000 is considered part of your taxable income.

No, life insurance premiums are not tax-deductible under most circumstances.

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/512dhP2BIfL._AC_UL320_.jpg)

![[Old Version] TurboTax Home & Business 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71K4wikrrkL._AC_UL320_.jpg)