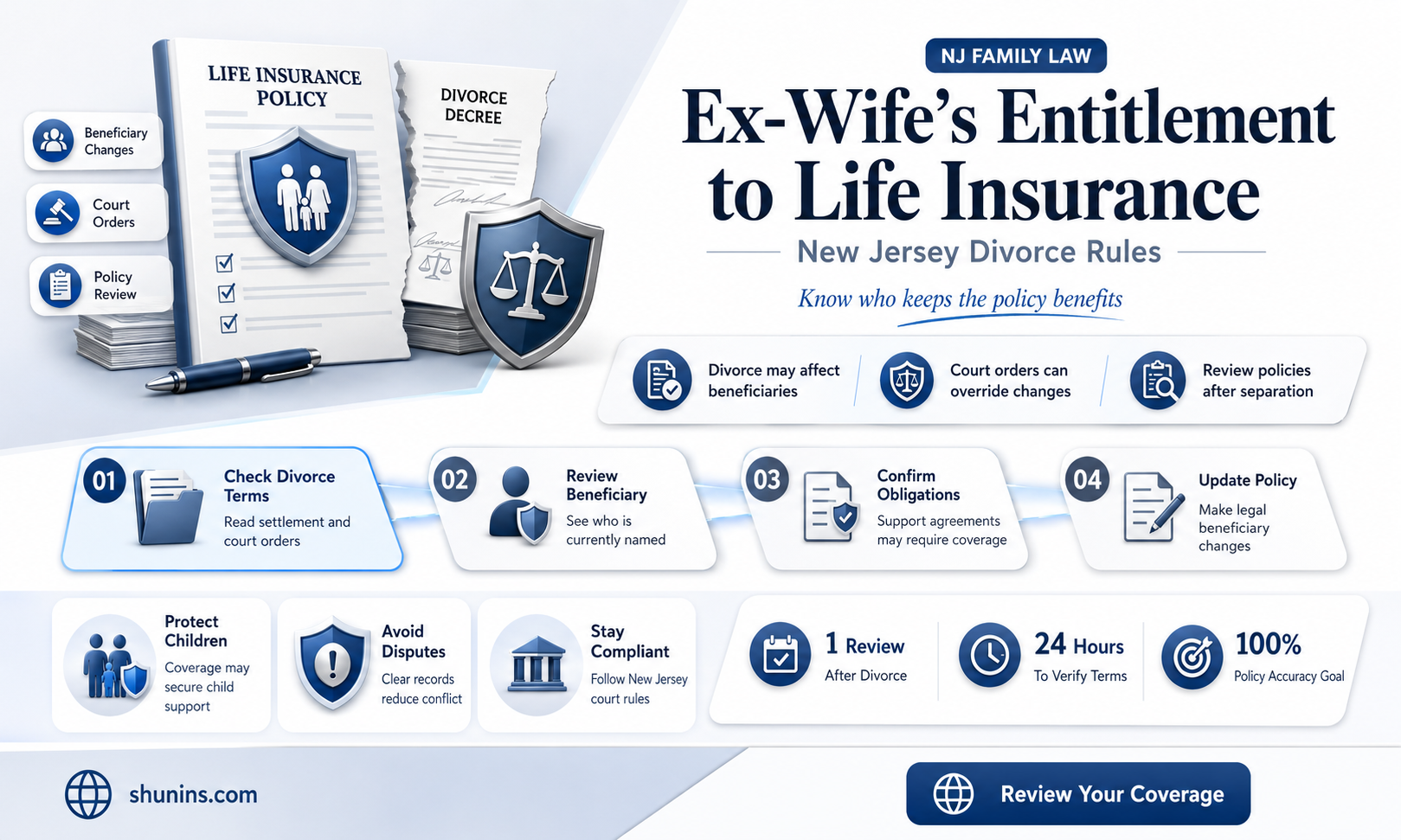

Life insurance is a crucial aspect to consider when going through a divorce. In New Jersey, if you are the beneficiary of your ex-spouse's life insurance policy, they cannot change that 90 days before officially filing for divorce. Once the divorce process begins, the state puts a freeze on changing beneficiaries until everything is settled. If your ex-spouse has alimony or child support obligations, the court may order them to continue paying the life insurance policy. In such cases, the court can also order that the insurance policy names the other parent or the supporting spouse as one of the beneficiaries.

| Characteristics | Values |

|---|---|

| Are ex-wives entitled to life insurance in New Jersey? | In New Jersey, if the ex-wife is listed as a beneficiary, the ex-husband cannot change that 90 days preceding the official date of filing for divorce. Once the divorce process is commenced, the state puts a freeze on changing beneficiaries until everything is settled. |

| Who is the life insurance beneficiary after divorce? | There is no universal rule on who receives life insurance after divorce. Factors such as the type of policy, the state where the policy was issued, and the language in the divorce decree will come into play when it is time to pay the life insurance benefit. |

| Can a divorce decree override a named beneficiary? | A divorce decree can override a beneficiary designation in a life insurance policy only in cases where the divorce decree (usually a state court order) is not preempted by laws controlling the life insurance policy itself. |

| Can an ex-spouse collect life insurance money if the deceased remarried? | Many states have enacted laws that automatically revoke the ex-spouse as the beneficiary on the life insurance policy following divorce. However, if the insured created a will or a trust after a divorce and included their life insurance policy in them, but failed to update a beneficiary on their policy, the existing beneficiary may have a valid claim for life insurance money after the insured's death. |

Explore related products

What You'll Learn

![]()

Ex-spouses can be removed from life insurance policies after divorce

While life insurance is an important consideration during a divorce, ex-spouses can be removed from life insurance policies after the marriage has been legally dissolved.

Life Insurance in the Context of Divorce

Divorce is a significant life event that can have far-reaching implications for insurance policies, including life insurance. During a divorce, it is essential to review and make necessary changes to your insurance coverage. This includes updating beneficiaries, adjusting coverage amounts, and ensuring compliance with any legal requirements or court orders related to the divorce settlement.

Removing an Ex-Spouse as a Beneficiary

One of the critical aspects of life insurance and divorce is determining the beneficiary of the policy. In most cases, individuals choose their spouse as the primary beneficiary of their life insurance policy. However, after a divorce, it is common for individuals to want to remove their ex-spouse as the beneficiary and designate someone else, such as a new partner or their children.

The ability to remove an ex-spouse as a beneficiary depends on several factors, including the terms of the divorce and any financial obligations towards the ex-spouse, such as alimony or child support. If there are no ongoing financial obligations towards the ex-spouse, removing them as a beneficiary is typically straightforward.

Legal and Financial Considerations

It is important to consult with a legal professional, such as a divorce attorney or a life insurance lawyer, to understand your rights and obligations regarding life insurance during and after a divorce. The laws governing life insurance and divorce can vary by state, and there may be specific statutes or court orders that come into play. For example, some states have revocation-upon-divorce statutes, which automatically revoke an ex-spouse's designation as a beneficiary on life insurance policies.

Additionally, if there are financial obligations, such as alimony or child support, a judge may require the policyholder to maintain the ex-spouse as a beneficiary to ensure continued support in the event of their death. In such cases, removing the ex-spouse as a beneficiary may require court approval or be prohibited altogether.

Practical Steps to Remove an Ex-Spouse

To remove an ex-spouse from a life insurance policy, it is advisable to follow these steps:

- Consult with a legal professional: Seek guidance from a divorce attorney or a life insurance lawyer to understand your specific situation and the applicable laws.

- Review the divorce terms: Examine the legal terms of your divorce, especially if there are provisions related to life insurance beneficiaries and financial support obligations.

- Contact the insurance company: Get in touch with the life insurance provider and inquire about their specific procedures for removing a beneficiary. Each insurance company may have its own processes, and it is essential to follow their guidelines.

- Provide necessary documentation: In some cases, you may need to provide documentation to the insurance company, such as a divorce decree or other legal documents, to support the removal of the ex-spouse as a beneficiary.

- Update the policy: Once the necessary steps have been taken, update the life insurance policy to reflect the removal of the ex-spouse as a beneficiary and the designation of a new beneficiary, if applicable.

While it is possible to remove an ex-spouse from a life insurance policy after divorce, it is important to approach this matter with careful consideration and legal guidance. The presence of financial obligations, court orders, and state-specific laws can impact the process. By seeking professional advice and following the necessary steps, individuals can effectively manage their life insurance policies during and after divorce, ensuring that their wishes are honoured and their loved ones are protected.

Life Insurance Suicides: A Morbid Truth or Urban Myth?

You may want to see also

Explore related products

![]()

Divorce decrees can override beneficiary designations

In some states, divorce does not affect a beneficiary designation in a life insurance policy. However, in other states, revocation-upon-divorce laws mean that an ex-spouse is automatically removed as a beneficiary. In these cases, the policyholder must designate a new beneficiary, otherwise, the death benefit will be paid to the estate.

If the policyholder was married in a community property state and is now divorced, the ex-spouse may be entitled to some of the death benefit, regardless of who is named as the beneficiary. This is because income earned during the marriage is considered community property, and if the policyholder paid the life insurance premiums with this income, the ex-spouse may receive a prorated portion of the payout.

If the policyholder is a child or spousal support obligor and fails to name their obligees as beneficiaries, those obligees may be entitled to the death benefit, regardless of the named beneficiary.

In the case of group life insurance policies provided by an employer, ERISA (the federal law that governs most employer-provided life insurance plans) supersedes state law. Under ERISA, a named beneficiary cannot be changed by divorce, so if the policyholder lives in a revocation-upon-divorce state and gets divorced, their ex-spouse remains the beneficiary.

It is important to note that if there are underage children involved in the divorce, the policyholder may need to keep their ex-spouse as the beneficiary to ensure the children are financially protected. Additionally, if spousal or child support is being paid, the judge may require the policyholder to maintain life insurance with the ex-spouse as the beneficiary to protect these payments.

Life Insurance: Can You Access Benefits Before Death?

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Failure to update beneficiary designations can lead to disputes

Life insurance disputes involving ex-spouses can be complex and emotionally charged, and failure to update beneficiary designations is a common trigger for these disputes. When a policyholder neglects to change the beneficiary after a divorce, it can result in the ex-spouse remaining as the primary beneficiary, which may entitle them to the insurance proceeds. This scenario can lead to conflicts between the ex-spouse and other potential recipients, such as the policyholder's new spouse, children, or siblings.

To avoid such disputes, it is crucial for divorcing parties to carefully review and update their life insurance policies during the divorce process. This includes changing beneficiary designations and considering the financial implications of any changes. Seeking legal counsel to understand their rights and obligations is essential.

In some cases, a court order or divorce settlement agreement may explicitly require the policyholder to maintain the ex-spouse as the named beneficiary, especially when alimony or child support payments are involved. If the policyholder fails to comply with these orders, disputes may arise between the ex-spouse and other beneficiaries or the policyholder's estate.

Additionally, community property considerations come into play in certain states. In these states, life insurance policies purchased during the marriage using marital funds may be considered marital assets, giving the ex-spouse a claim to a portion of the benefits even if they are not the named beneficiary.

To summarise, failure to update beneficiary designations on life insurance policies post-divorce can lead to disputes, especially when the ex-spouse is entitled to receive benefits. To prevent conflicts, divorcing individuals should proactively address life insurance policies during the divorce process, seek legal counsel, and make necessary changes to beneficiary designations.

Life Insurance Cash Value: Does It Keep Growing?

You may want to see also

Explore related products

![]()

Divorce settlements can address life insurance policies

If there are children involved, the divorce settlement may require one or both parties to maintain life insurance policies to protect the children's interests. This is especially relevant if there are child support or alimony obligations, as the dependent spouse and/or children need to be financially provided for in the event of the paying spouse's death. In such cases, the court may order the paying spouse to keep their ex-spouse as the beneficiary on their life insurance policy.

Additionally, the divorce settlement may outline specific requirements for the life insurance policy, such as the payout amount and the beneficiaries. For example, if the paying spouse is required to pay $10,000 a year in alimony for 10 years, they may be mandated to maintain a life insurance policy with a sum of $100,000 for the benefit of their ex-spouse. The settlement may also allow for adjustments to the policy over time, such as reducing the coverage amount annually to align with the decreasing alimony obligation.

It's important to note that the specific laws and regulations regarding life insurance policies in divorce settlements can vary by state. In some states, a former spouse automatically loses their designation as a beneficiary on life insurance policies after a divorce, while in other states, federal laws may supersede and allow the ex-spouse to remain as the beneficiary. Therefore, it's crucial to consult with a legal professional familiar with the relevant state and federal laws to navigate these complexities effectively.

Universal Life Insurance: Cash Surrender Policyowner's Guide

You may want to see also

Explore related products

![]()

Life insurance can replace child support and alimony

Life insurance can be used to replace child support and alimony during divorce or separation. The court may require the supporting spouse to keep paying the life insurance policy to back up these obligations. The judge can also order that the insurance policy names the other parent or the supporting spouse as one of the beneficiaries.

In the case of New Jersey, the state puts a freeze on changing beneficiaries until the divorce is settled. If the supporting spouse refuses to make payments, the court can issue financial sanctions on their assets until they comply. However, if they don't have alimony obligations, the designation of the beneficiary can be revoked once the final divorce decree is reached.

The amount of life insurance required will depend on several factors, including age, gender, health status, and financial resources available to support children or other beneficiaries. Some insurers offer different levels of coverage, such as "term" policies with fixed premiums for a specific number of years, while others offer whole life insurance, which provides lifetime protection at higher monthly costs.

Divorce settlements often address life insurance policies, including beneficiaries and death benefit amounts. If you are required to pay alimony or child support, the divorce decree might mandate keeping your ex-spouse as the beneficiary. Alternatively, you may need to purchase a new policy that would pay out a certain amount to your ex-spouse in the event of your death.

It is important to consult a divorce lawyer to understand how life insurance should be incorporated into your specific divorce settlement. They can advise you on removing your ex-spouse from your life insurance policy, as it depends on the terms of your divorce. If you are not financially supporting your ex-spouse post-divorce and own the policy, you can likely remove them as the beneficiary. However, if you are responsible for alimony or child support, a judge may require you to keep your ex-spouse as the beneficiary to ensure continued support in the event of your death.

Life Insurance for Incarcerated: Is It Possible?

You may want to see also

Frequently asked questions

Life insurance can help protect the assets you’ve worked to build, and that becomes even more important after a divorce. It can also be used to replace child support and alimony.

In New Jersey, if your ex-spouse had you as their beneficiary, they cannot change that 90 days preceding the official date of filing for divorce. Once the divorce process is commenced, the state puts a freeze on changing beneficiaries until everything is settled.

Yes, if you own the policy and are not financially supporting your ex-spouse, you can likely remove them. However, if you are paying alimony or child support, a judge may require you to keep your ex-spouse as a beneficiary.

The amount of life insurance needed will depend on age, gender, health status, and financial resources available to support children or other beneficiaries.

Yes, if the beneficiary is not updated after the divorce, the ex-wife can still be entitled to the insurance proceeds.