Indexed universal life insurance (IUL) is a type of permanent life insurance that provides a cash value component and a death benefit. The cash value in a policyholder's account can earn interest by tracking a stock market index chosen by the insurer, such as the S&P 500 or Nasdaq-100. IUL policies offer a guaranteed minimum interest rate, protecting the principal from losses in the market, but they also often cap the maximum amount that can be earned. The interest rate derived from the equity index account can fluctuate, and policies are generally more volatile than fixed universal life policies.

| Characteristics | Values |

|---|---|

| Interest rate | Based on the performance of a chosen stock market index, with a minimum guaranteed rate |

| Caps | Yes, there is a limit to the rate of cash value growth |

| Floors | Yes, there is a minimum guaranteed rate |

| Premium | Flexible |

| Death benefit | Flexible |

| Risk | Less risky than variable universal life insurance but riskier than fixed universal life insurance |

| Fees | Yes, including premium expense charges, administrative expenses, and fees and commissions |

Explore related products

What You'll Learn

![]()

Indexed universal life insurance offers tax-free capital gains

Indexed universal life insurance (IUL) offers tax-free capital gains, meaning that policyholders do not pay capital gains tax on the increase in cash value over time. This is unless they abandon the policy before it matures, which is not the case with other types of financial accounts, where capital gains tax may be applied upon withdrawal.

IUL policies are often pitched as a cash-value policy that benefits from tax-free market gains without the risk of loss during a market downturn. The cash value portion of the policy earns interest based on the performance of an underlying stock market index. For example, returns may be linked to the Standard & Poor's (S&P) 500 composite price index, which tracks the movements of the 500 largest US companies by market capitalization. As the index moves up or down, so does the rate of return on the cash value component of the policy.

The death benefit, which is paid out to the named beneficiary or beneficiaries when the policyholder dies, can also be passed on tax-free.

IUL policies are best for those with large upfront investments who are seeking options for a tax-free retirement.

How to Adjust Your Life Insurance Payout

You may want to see also

Explore related products

$14.99 $14.95

![]()

It provides higher return potential

Indexed universal life insurance (IUL) offers higher return potential than other types of life insurance. This is because the cash value of an IUL policy is linked to the performance of a stock index, such as the S&P 500, which means that the cash value grows when the market grows. This growth is often accumulated tax-deferred.

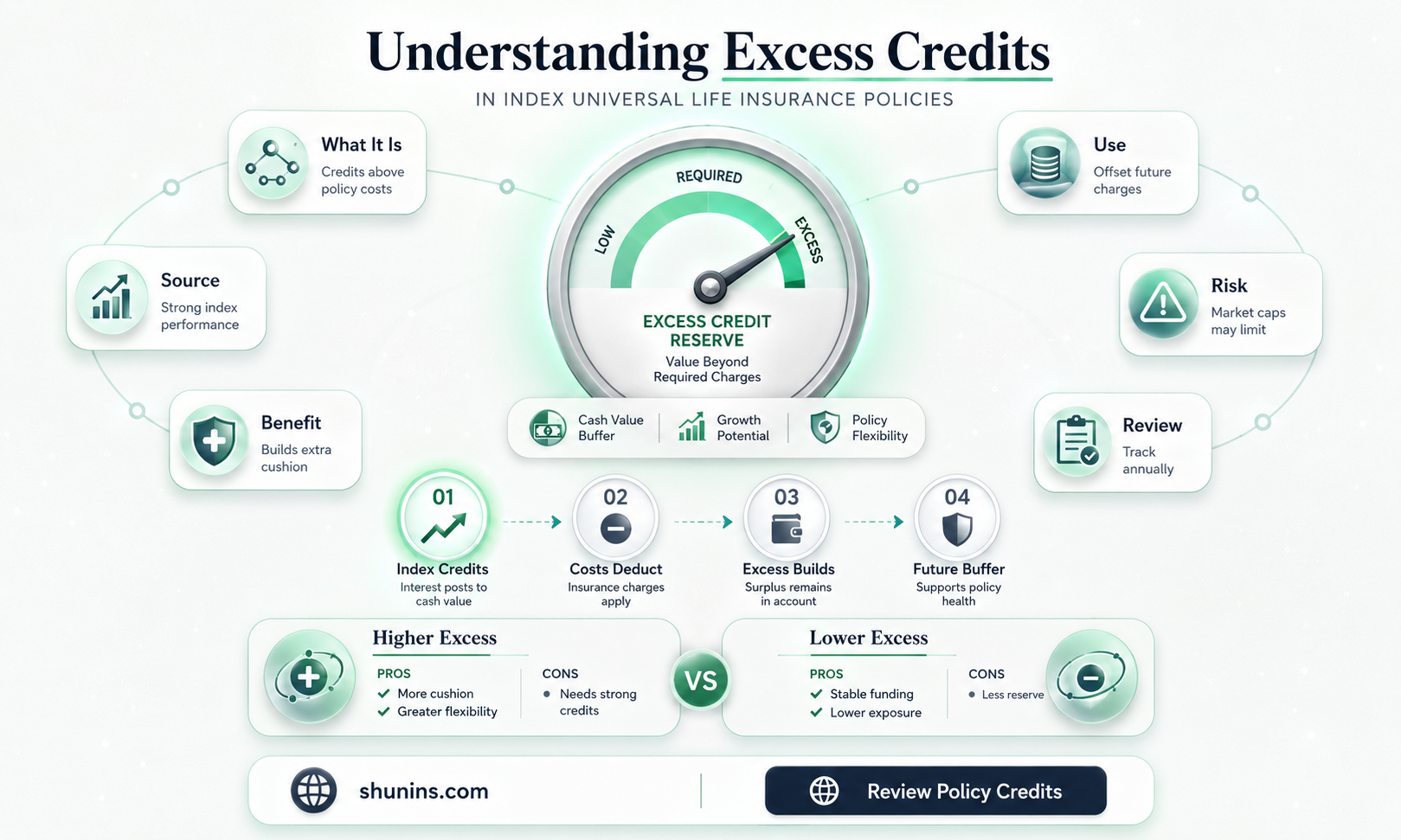

The annual return on an IUL policy depends on the performance of its underlying index. However, insurance companies can offer a guaranteed minimum return on investment. This is because IUL policies have a "floor", which is the lowest the interest rate can go, often set at 0%. This means that even if the market crashes, the account won't suffer losses.

IUL policies also have a "cap", which is the highest interest rate the account can earn. For example, if the cap is 10% and the index rises by 12%, you will only earn interest of 10%.

The participation rate is another way that an IUL policy can restrict interest. This is the percentage of the index return that you receive each year. For example, if the policy has a 70% participation rate and the index grows by 10%, your cash value return will only be 7%.

Despite these restrictions, IUL policies still offer higher return potential than other types of life insurance. This is because they are linked to the performance of the stock market, whereas whole life insurance policies and fixed universal life insurance policies offer only a small interest rate that may not even be guaranteed.

Progressive's Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Policyholders can decide how much risk they want to take

The advantage of this type of policy is that it offers the potential for higher returns than other types of life insurance. If the chosen index performs well, the cash value of the policy will increase. However, there is also the risk that the index could perform poorly, which would result in lower returns or even losses. To manage this risk, policyholders can choose to allocate a portion of their cash value to a fixed-rate account, which offers a guaranteed minimum return.

The level of risk in an indexed universal life insurance policy is also affected by the participation rate and the cap on returns. The participation rate determines how much of the index's return the policyholder will receive. For example, if the index grows by 10% and the participation rate is 70%, the cash value return would only be 7%. The cap on returns sets an upper limit on how much the cash value can grow, even if the index performs extremely well. These factors can limit the potential returns of the policy, but they also help to protect against large losses.

Overall, indexed universal life insurance offers policyholders the flexibility to choose their level of risk and potential return. By allocating their cash value between the equity-indexed account and the fixed-rate account, policyholders can balance their investment goals and risk tolerance. This makes indexed universal life insurance a good option for those who want more control over their investments and are comfortable with some level of risk.

Marriott's Employee Benefits: Life Insurance Coverage

You may want to see also

Explore related products

![]()

The death benefit is flexible and guaranteed

Index universal life insurance (IUL) offers a flexible death benefit that is guaranteed as long as premiums are paid. This means that the death benefit can be adjusted as needed, but the policy must remain in force for the benefit to be paid out.

The death benefit is permanent and not subject to income or death taxes. It also does not need to go through probate, which can be a lengthy process. The benefit can be used to cover funeral and burial expenses, pay off outstanding debts, fund college costs, or cover everyday living expenses for the deceased's loved ones.

The death benefit is also flexible in that it can be passed on to beneficiaries tax-free. This means that the full amount of the benefit will be available to the beneficiaries, without any deductions for taxes.

In addition to the death benefit, IUL policies also offer a cash value component. This means that the policy can increase in value during the lifetime of the insured through the accumulation of cash value. The cash value can be accessed in several ways, such as through loans or withdrawals, and can be used to pay premiums or supplement retirement income.

The flexibility of IUL policies makes them a good option for those who want the security of a death benefit while also building cash value. However, it is important to carefully consider the pros and cons of IUL policies before purchasing one, as there are potential drawbacks, including complex fee structures and unpredictable returns.

Globe Insurance: Term Life Insurance Options and Availability

You may want to see also

Explore related products

![]()

It is less risky than variable universal life insurance

Index universal life insurance (IUL) is considered less risky than variable universal life insurance (VUL) because it does not directly invest in the stock market. While IUL policies track the performance of a stock market index, the money in the policyholder's cash value account is not directly invested in the market. This means that the policyholder does not lose money if the market crashes.

IUL policies offer a guaranteed minimum interest rate, which limits losses. They also have a cap on gains, which is typically around 8-12%. This means that the policyholder will not benefit from the full gains of the stock market index if it performs extremely well.

In contrast, VUL policies allow the policyholder to invest directly in mutual funds or other securities. This means that the policyholder can potentially lose money if the investments perform poorly. There is no guaranteed minimum interest rate with VUL policies, so losses can be significant.

IUL policies are also less risky than VUL policies because they offer more flexibility. Policyholders can decide how much risk they want to take by adjusting the percentage of their cash value that is allocated to the equity-indexed account and the fixed-rate account. They can also adjust their premiums and death benefits as needed.

Overall, IUL policies are considered a less risky option than VUL policies because they offer a guaranteed minimum interest rate, a cap on gains, and more flexibility for the policyholder.

Life Insurance: Owner's Rights to Remaining Balance Explained

You may want to see also

Frequently asked questions

Indexed universal life insurance is a type of permanent life insurance that provides a cash value component along with a death benefit. The money in a policyholder's cash value account can earn interest by tracking a stock market index selected by the insurer, such as the Nasdaq-100 or the Standard & Poor's 500.

Some benefits of indexed universal life insurance include higher return potential, greater flexibility, tax-free capital gains, and no impact on Social Security benefits.

Some drawbacks of indexed universal life insurance include possible limits on returns, unpredictable returns, and higher fees compared to other policies.