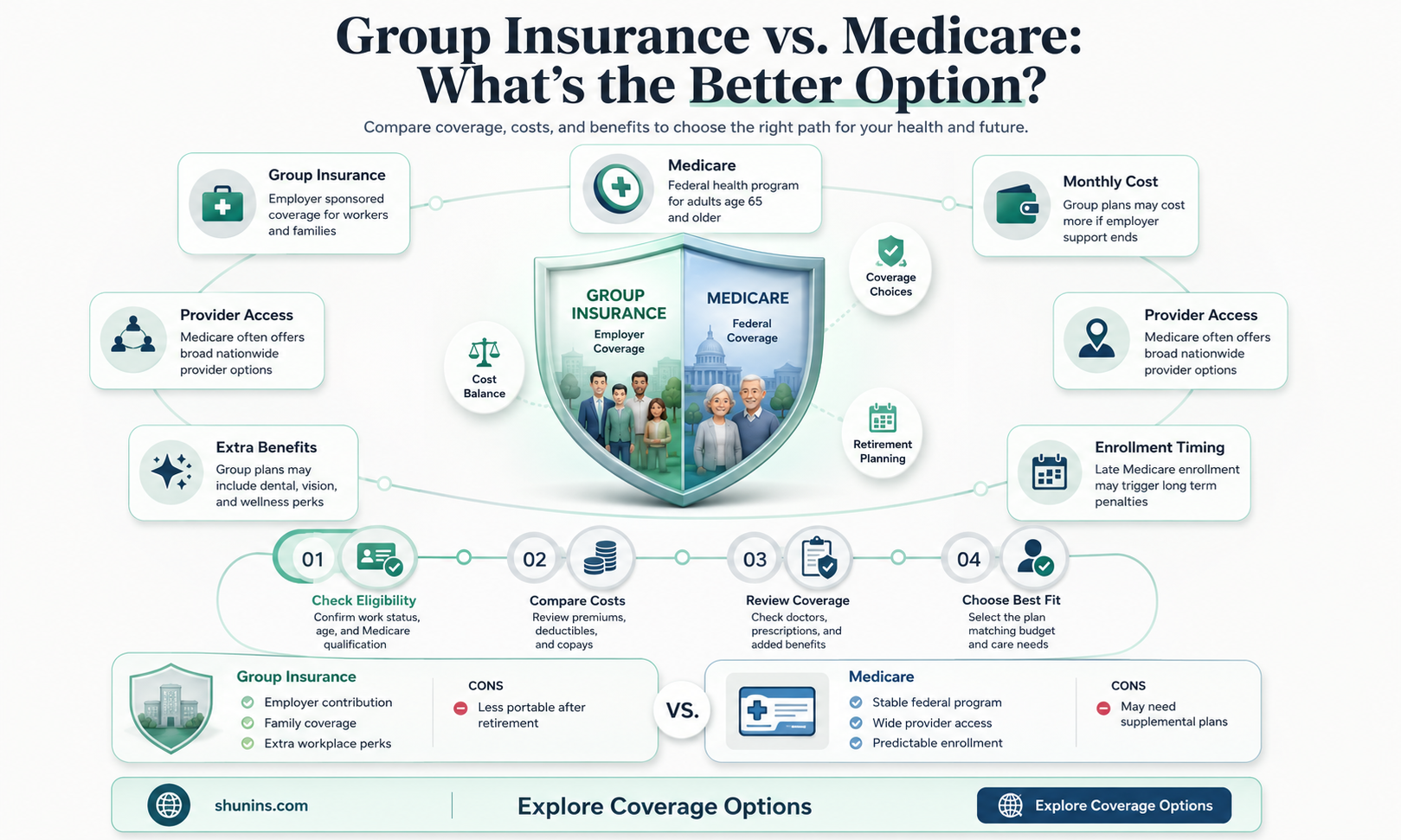

If you have group health insurance through your employer and are eligible for Medicare, you may be wondering which option is better for you. It's important to understand that you can have both Medicare and employer insurance at the same time, and they can work together. The primary payer pays up to the limits of its coverage, and the secondary payer covers some or all of the remaining costs. Whether Medicare or your group insurance is the primary payer depends on the size of your company and the specifics of your insurance plans. Reviewing deductibles, coinsurance, and coverage options will help you decide which option is best for your needs.

| Characteristics | Values |

|---|---|

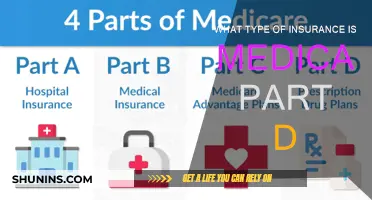

| Medicare Part A | Hospital Insurance |

| Medicare Part B | Medical Insurance |

| Medicare Part C | Medicare Advantage |

| Medicare Part D | Prescription Drug Plan |

| Group health plan | Coverage from employer or spouse's employer |

| Primary payer | Pays up to the limit of its coverage |

| Secondary payer | Pays the remaining balance |

| Coordination of benefits | Order of payment when having multiple insurance plans |

| Creditable coverage | Benefits that are at least as good as those offered by Medicare |

| Deductibles | Out-of-pocket expenses before insurance coverage kicks in |

| Coinsurance | Percentage of costs covered by insurance |

| Copayments | Fixed amount paid for a covered service |

| Health Savings Account (HSA) | Account for tax-advantaged savings for medical expenses |

Explore related products

What You'll Learn

![]()

Medicare and employer insurance can be held simultaneously

If an individual is eligible for Medicare and has employer insurance, they can delay enrolling in Medicare Part B without incurring penalties, as long as their employer insurance qualifies as "creditable coverage", meaning it provides benefits that are at least as good as Medicare's. Once an individual retires or loses their employer coverage, they can enroll in Medicare Part B during a Special Enrollment Period (SEP) without facing late enrollment penalties. This SEP typically lasts for eight months.

The primary and secondary payers are determined based on the size of the employer. If an individual's company has fewer than 20 employees, Medicare is the primary payer. If the company has 20 or more employees, the employer coverage is the primary payer, and Medicare is the secondary payer. In this case, Medicare pays only for covered services that the employer's group health coverage did not pay.

It is important to note that Medicare coverage applies only to the individual and does not extend to dependents or spouses, even if the employer's group health plan covers them. Individuals should carefully consider their health needs, medical expenses, and spousal coverage before deciding whether to skip Medicare enrollment or delay enrolling in Medicare Part B.

Major Medical Insurance: Long-Term Care Coverage Options

You may want to see also

Explore related products

![]()

Medicare Part B and employer insurance can be coordinated

The primary payer is determined by the size of the employer. If the employer has 20 or more employees, the employer's group health coverage pays first, and Medicare pays second. If the employer has fewer than 20 employees, Medicare pays first, and the employer's group health plan pays second.

If you are still working and have employer insurance when you become eligible for Medicare, you have the option to delay enrolling as long as your employer insurance qualifies as "creditable coverage", meaning it provides benefits that are at least as good as those offered by Medicare. Once you lose your employer coverage, you can enroll in Medicare Part B during a Special Enrollment Period (SEP) without facing late enrollment penalties. This SEP typically lasts for eight months after your employment or coverage ends.

It is essential to coordinate the timing of your Medicare Part B enrollment with the end of your employer coverage to ensure uninterrupted healthcare benefits.

Switching Medical Insurance: When and Why You Should Change

You may want to see also

Explore related products

![]()

Group health plan size determines Medicare enrolment requirements

If you have group health insurance through your employer or your spouse's employer, you may be wondering how it works with Medicare. The short answer is that it depends on the size of the group health plan. Medicare uses a primary payer and secondary payer system, where the primary payer pays up to the limits of its coverage, and the secondary payer covers the rest of the balance.

If you have a non-tribal group health plan through an employer with 20 or more employees, your group health plan is the primary payer, and Medicare pays second. On the other hand, if your employer has fewer than 20 employees, Medicare is the primary payer, and your group health plan is the secondary payer. This also applies to retiree or COBRA coverage, regardless of the employer's size.

It's important to note that if you have employer insurance that qualifies as "creditable coverage," meaning it provides benefits that are at least as good as Medicare, you can delay enrolling in Medicare Part B without penalty. However, once you retire or lose your employer coverage, you can enroll in Medicare Part B during a Special Enrollment Period (SEP) without late enrollment penalties.

In addition, Medicare Supplement (Medigap) plans, Prescription Drug (Part D) plans, and Medicare Advantage (Part C) plans are also available. These plans offer additional benefits, such as prescription drug coverage, that may not be included in your group health plan.

When deciding whether to enrol in Medicare or keep your group health insurance, it's essential to consider factors such as the cost of premiums, deductibles, and the specific benefits offered by each plan.

Health Insurance and Retroactive Coverage: What's the Deal?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medicare Part A and B are prerequisites for TFL benefits

Medicare is a federal health insurance program for individuals aged 65 and older, as well as certain younger individuals with disabilities. It consists of multiple parts, with Part A covering inpatient hospital care, skilled nursing facility care, hospice care, and some home health care, and Part B covering medical services and outpatient care, including doctor visits, preventive services, and durable medical equipment.

Group health insurance, on the other hand, is coverage provided by an employer. If you have group health insurance and Medicare, the two can work together, with one being the primary payer and the other the secondary payer. The primary payer pays up to the limits of its coverage, after which the secondary payer covers the remaining balance, if applicable. The size of the employer determines which insurance pays first, with Medicare usually being the primary payer for smaller companies and the secondary payer for larger ones.

TRICARE For Life (TFL) is a type of coverage that combines Medicare and TRICARE, a health program for military personnel, retirees, and their families. TFL provides expanded medical coverage to Medicare-eligible individuals who are also TRICARE-eligible, and having both Medicare Part A and Part B is a prerequisite for TFL benefits. This means that to receive TFL coverage, individuals must have both hospital insurance (Part A) and medical insurance (Part B) through Medicare.

In conclusion, Medicare Part A and Part B are essential for individuals seeking TFL benefits. By having both parts, individuals can access the expanded coverage provided by TFL, which combines the benefits of Medicare and TRICARE. It is important for those interested in TFL to ensure they have enrolled in both Medicare Part A and Part B to be eligible for this enhanced coverage option.

Buckeye Insurance: Weight Loss Medication Coverage Options

You may want to see also

Explore related products

![]()

Medicare Part B enrolment timing is crucial

Medicare Part B is a component of Original Medicare, a federal health insurance programme for individuals aged 65 and older, as well as certain younger individuals with disabilities. Part B primarily covers medical services and outpatient care, including doctor visits, preventive services, and durable medical equipment.

The IEP is a 7-month period that begins 3 months before the month a person turns 65, includes their birthday month, and ends 3 months after they turn 65. Coverage always starts on the first of the month.

The SEP is an 8-month period that starts when you stop working or lose your job-based health coverage, whichever comes first. If you want Medicare coverage to start immediately after your job-based health insurance ends, you need to sign up for Part B the month before you plan to retire. Your coverage will start the month after Social Security or the Railroad Retirement Board receives your completed forms.

If you miss the 8-month SEP, you will have to wait to sign up and may go months without coverage. You might also have to pay a monthly late enrolment penalty until you turn 65.

It is important to note that Medicare Part B can work together with employer insurance if you are still working and have employer insurance when you become eligible for Medicare. In this case, you can delay enrolling in Medicare Part B as long as your employer insurance qualifies as ""creditable coverage,"" meaning it provides benefits that are at least as good as those offered by Medicare.

Prescription Refills: Insurance-Free Options for Patients

You may want to see also

Frequently asked questions

Group insurance is provided by your employer, while Medicare is a federal health insurance program for individuals aged 65 and older, as well as certain younger individuals with disabilities.

Yes, you can have both group insurance and Medicare at the same time. However, you need to determine which insurance is the primary payer and which is the secondary payer.

If your company has fewer than 20 employees, Medicare is the primary payer. If your company has 20 or more employees, your group health insurance is the primary payer.

Having both group insurance and Medicare can provide additional coverage and help pay for any costs not covered by the primary insurance. It can also give you access to a wider range of healthcare services and providers.