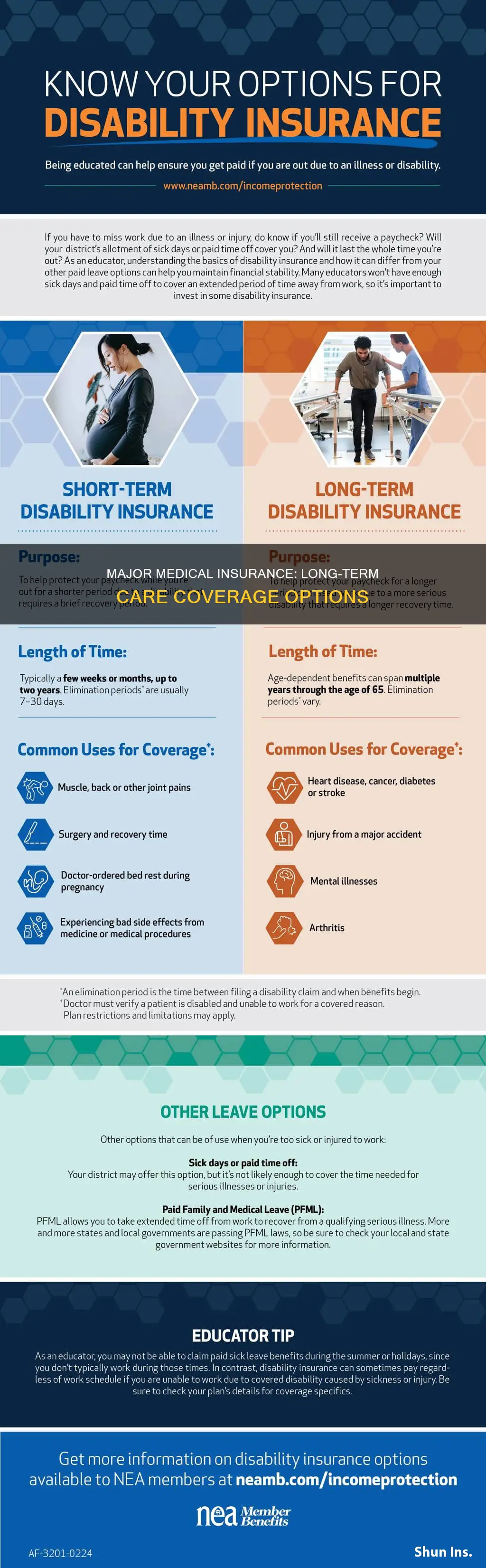

Long-term care insurance is a type of insurance that covers medical and non-medical costs for people with chronic illnesses or disabilities. This includes supervision and help with day-to-day tasks, as well as medical equipment, transportation, and other costs. Most major medical insurance companies, including Medicare, do not cover long-term care. However, some companies offer long-term care policies, and individuals can also purchase private long-term care insurance. The cost of long-term care insurance varies depending on age, gender, and other factors, and there are different types of policies available, such as stand-alone and hybrid policies. Additionally, some employers offer group long-term care policies to their employees. When considering long-term care insurance, it is important to plan ahead, understand the coverage options, and be aware of any pre-existing conditions that may affect eligibility.

| Characteristics | Values |

|---|---|

| Definition | There is no official definition of the term "major medical health insurance". |

| Description | Major medical insurance is a specific type of health insurance plan that covers medical expenses associated with serious illness or hospitalization. |

| Coverage | Major medical insurance covers preventive care services, urgent care visits, emergency room visits, prescription medications, and other routine medical expenses. It does not cover cosmetic procedures or pre-existing medical conditions. |

| Duration | Major medical insurance plans have longer terms than short-term insurance plans. |

| Enrollment | Major medical plans often have set enrollment periods, limiting the flexibility to change plans except during specific times like Open Enrollment or qualifying life events. |

| Cost | The cost of major medical insurance varies depending on the insurance company and the type of plan chosen. ACA major medical plans are classified into tiers (Bronze, Silver, Gold, Platinum, and Catastrophic) with different premiums based on the percentage of healthcare costs covered. |

| Compliance | Major medical plans are required to comply with the Affordable Care Act (ACA) and provide minimum essential benefits. Off-exchange plans purchased directly from an insurer must also be ACA-compliant. |

| Availability | Major medical insurance can be obtained through an employer, the government, or by purchasing it on one's own. It can be enrolled in online via Healthcare.gov, state marketplaces, private exchanges, or directly from insurance companies or brokers. |

Explore related products

What You'll Learn

![]()

Short-term health insurance plans

Some of the best short-term health insurance plans for 2025 include UnitedHealthcare's Copay Select Max, which offers a wide provider network and prescription drug coverage, and Everest's Flex Term Health Insurance, which is widely available in most states and offers comprehensive coverage for basic and major medical needs. Pivot Health's Epic Base and Deluxe plans are also highly rated, with low deductibles and copays, although their maximum coverage benefit may be lower in some areas.

It is important to carefully consider your upcoming health needs and read all the details before enrolling in a short-term health insurance plan, as these plans can vary greatly in cost and coverage. They may not be suitable for long-term use or as a replacement for traditional major medical coverage.

Insurance Deductibles: Are They Tax-Deductible Medical Expenses?

You may want to see also

Explore related products

![]()

Comprehensive coverage

Prior to the Affordable Care Act (ACA), the term "Major Medical Insurance" referred to the most comprehensive health insurance plans available. The ACA changed this by requiring all policies to include more comprehensive benefits, known as the Ten Essential Health Benefits. These benefits include:

- Ambulatory Patient Services

- Emergency Services

- Hospitalizations

- Maternity and Newborn Care

- Prescription Drugs

- Laboratory Services

- Preventive Care

- Mental Health and Substance Abuse Treatment

- Pediatric Care

- Rehabilitation Treatment

Today, all health insurance plans are considered "Major Medical" and provide a minimum level of coverage. Comprehensive coverage can be more expensive than limited-coverage plans, but it offers broader protection and peace of mind. It is important to note that comprehensive coverage may vary depending on the insurance provider and the specific plan chosen.

In terms of long-term care, comprehensive coverage can include services such as in-home caregiving, medical equipment, and home modifications. However, standalone long-term care policies are becoming less common, with most providers now offering hybrid options tied to life insurance or annuity plans. Comprehensive coverage can provide financial protection and help individuals manage chronic conditions or disabilities, preventing the need to avoid necessary medical care due to high costs.

Understanding Pennsylvania's Essential Medical Insurance Coverage

You may want to see also

Explore related products

$63.99 $280

![]()

Preventative care services

Under the Affordable Care Act (ACA), private health plans must provide coverage for a range of preventive services without imposing cost-sharing, such as copayments, deductibles, or coinsurance. This applies to all private plans, including fully insured and self-insured plans in the individual, small group, and large group markets, except those with "`grandfathered`" status. The ACA requires plans to cover four broad categories of services for adults and children, as recommended by expert medical and scientific bodies such as the U.S. Preventive Services Task Force (USPSTF) and the Advisory Committee on Immunization Practices (ACIP).

Preventive services for children and adolescents are also covered by most health plans at no cost when delivered by an in-network provider. This includes a range of preventive health screening and counseling services. However, it is important to note that specific coverage may vary depending on the type of insurance, such as private or public, and the state in which the insurance is provided.

In terms of specific services, preventive care can be categorized into three main areas. The first category includes screenings such as colon cancer screening for adults ages 45-75, hepatitis C screening for adults at increased risk, HIV screening for ages 15-65, and lung cancer screening for heavy smokers or former smokers aged 55-80. The second category involves immunizations, with recommended populations and dosages varying. The third category includes annual check-ups, where a primary care provider assesses an individual's physical and emotional health, and may recommend additional screenings based on factors like family history, age, and current health status.

It is important to consult with your insurance provider to understand the specific preventive services covered by your plan, as well as any network restrictions or fee schedules that may apply.

Understanding Self-Funded Medical Insurance Plans

You may want to see also

Explore related products

![]()

ACA-compliant plans

Long-term care insurance can be purchased to cover services and support for those diagnosed with a disability or chronic medical condition who need help with basic activities. This is also referred to as "custodial care". This type of insurance can be purchased directly from insurance companies or through an agent. Some employers also offer the opportunity to purchase coverage from their brokers at group rates.

When considering ACA-compliant plans in the context of long-term care, it is important to understand the limitations and waiting periods associated with these plans. While ACA-compliant plans can provide comprehensive coverage for essential health benefits, long-term care is often categorized as a separate type of insurance. This means that individuals specifically seeking coverage for long-term care services may need to explore dedicated long-term care insurance policies or other specialized options.

It is worth noting that some ACA-compliant plans may offer limited coverage for short-term nursing home stays or home health care services, but comprehensive long-term care coverage is typically not included. Individuals should carefully review the details of their specific ACA-compliant plan to understand the extent of their coverage for long-term care services. Additionally, it is important to be aware of potential delays in coverage for pre-existing conditions, which can vary depending on the policy.

To summarize, while ACA-compliant plans provide essential health benefits and improve access to healthcare, they typically do not include comprehensive coverage for long-term care services. Individuals seeking protection against the financial burden of long-term care expenses may need to supplement their ACA-compliant plans with dedicated long-term care insurance policies or explore alternative options like Medicaid, depending on their financial situation.

Insurance Companies and Medical Records: Who Has Access?

You may want to see also

Explore related products

![]()

Monthly premiums

Long-term care insurance is an important consideration for people as they age. It covers a range of essential services, including medical and non-medical care for those with a chronic illness or disability. However, it is important to note that private health insurance, including Medicare and Medicare Supplement Insurance (Medigap), does not typically pay for long-term care. Medicare only covers specific long-term care programs, such as a portion of care in a skilled nursing facility and care provided by a home healthcare agency if the patient is confined to their home.

The cost of long-term care insurance varies depending on several factors, including age, health, coverage, riders, the insurance company, and marital status. According to the 2024 American Association for Long-Term Care Insurance (AALTCI) annual Price Index survey, the average annual premium for a $165,000-benefit policy with no inflation protection is $950 for a single 55-year-old male and $1,500 for a single 55-year-old female. The same coverage for a 60-year-old couple with joint coverage would cost $213 per month, according to Forbes. Additionally, some insurers may require a physical exam or medical record review, while others conduct health interviews via telephone.

It is worth noting that long-term care insurance can have tax advantages. Federal and some state tax codes allow you to deduct part or all of the long-term care insurance premiums as medical expenses, provided they meet certain federal standards and are labelled as "Federally Tax Qualified" or "tax-qualified". These deductions can be made on your federal and state income tax returns, depending on your age and the amount of the annual premium.

When considering long-term care insurance, it is important to select a premium that you can comfortably afford. While it may be tempting to opt for a higher premium to increase coverage and benefits, it is crucial to ensure that the monthly payments are sustainable, especially considering that income often does not keep pace with inflation during retirement. Additionally, it is worth exploring alternative options, such as hybrid or linked-benefit policies, which combine long-term care coverage with another benefit, typically life insurance or an annuity. These policies may offer a lump-sum payment option or fixed annual payments, eliminating the risk of rising premiums.

Understanding Medical Insurance Carriers: Who They Are and What They Do

You may want to see also

Frequently asked questions

Major medical insurance is a type of health insurance that covers serious illnesses or hospitalizations, as well as preventive care services, urgent care visits, emergency room visits, prescription medications, and other routine medical expenses. It is more comprehensive than short-term insurance and provides coverage for a longer duration.

Major medical insurance covers a wide array of inpatient and outpatient healthcare services, including preventive care, urgent care, emergency room visits, prescription medications, and other routine medical expenses. It also covers the Ten Essential Health Benefits, which include areas such as maternity care, mental health services, and prescription drugs. However, it is important to note that cosmetic procedures are generally not covered by major medical insurance.

Major medical insurance is a term used to describe comprehensive and robust health coverage. All health insurance plans today are considered "Major Medical" as they cover the Ten Essential Health Benefits. Major medical insurance plans are also typically ACA-compliant, adhering to the minimum essential benefit standards set by the Affordable Care Act. These plans are usually obtained through an employer, the government, or purchased individually.

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)