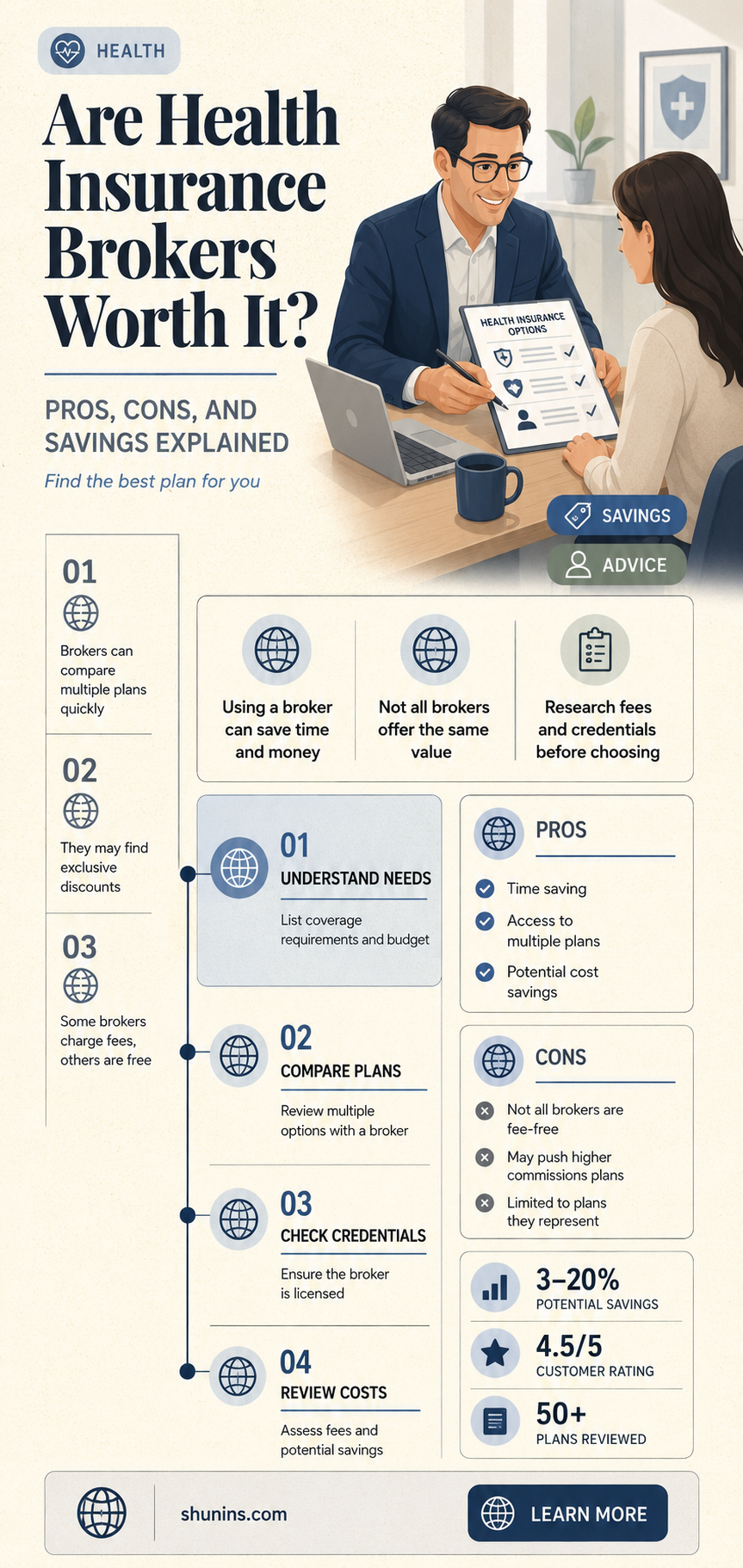

Health insurance brokers act as intermediaries between individuals or businesses and insurance providers, offering expertise to navigate the complex world of health insurance plans. While some may question their value, brokers can be worth considering for those overwhelmed by the myriad of options, policy jargon, and fine print. They provide personalized guidance, assess individual needs, and help find plans that align with specific health requirements and budgets. Additionally, brokers often have access to a wide range of policies, including those not available directly to consumers, potentially securing better rates or coverage. However, their services typically come with fees or commissions, which may offset some savings. Ultimately, whether a health insurance broker is worth it depends on one’s comfort level with researching and selecting a plan independently versus the convenience and expertise a broker provides.

| Characteristics | Values |

|---|---|

| Expertise & Personalization | Brokers have in-depth knowledge of the health insurance market, plans, and provider networks. They can assess your needs (health, budget, preferred doctors) and recommend suitable plans, ensuring you don't overlook crucial details. |

| Time Savings | Navigating health insurance options is complex and time-consuming. Brokers streamline the process by presenting tailored options, handling paperwork, and explaining plan details, saving you hours of research. |

| Cost Comparison | Brokers have access to a wide range of plans, including those not available directly to consumers. They can compare premiums, deductibles, copays, and out-of-pocket maximums to find the best value for your needs. |

| Advocacy & Support | Brokers act as your advocate during enrollment, assisting with applications, resolving issues, and answering questions. They also provide ongoing support for claims, policy changes, and renewals. |

| No Additional Cost | Brokers are typically paid by insurance companies through commissions, so their services are free to you. The premium you pay is the same whether you use a broker or buy directly. |

| Market Access | Brokers often have access to plans and networks not available through public marketplaces, potentially offering more options and better coverage. |

| Unbiased Advice | Reputable brokers prioritize your needs over any specific insurer, providing objective recommendations based on your situation. |

| Potential Drawbacks | While rare, some brokers might prioritize commissions over your best interests. It's crucial to choose a licensed, reputable broker with good reviews. |

Explore related products

What You'll Learn

![]()

Cost savings through broker negotiations

Health insurance brokers often act as intermediaries between consumers and insurance providers, leveraging their industry knowledge and relationships to negotiate better terms. One of their most tangible contributions is securing cost savings through strategic negotiations. Unlike individual buyers, brokers handle high volumes of policies, giving them greater bargaining power with insurers. This dynamic allows them to negotiate lower premiums, reduced deductibles, or additional benefits that might not be available to direct purchasers. For instance, a broker might secure a 10-20% premium discount for a group plan by bundling multiple policies or demonstrating lower risk profiles.

Consider a small business owner with 25 employees seeking health coverage. Without a broker, they might receive a standard group plan quote with a $500 deductible per employee and limited out-of-network coverage. A broker, however, could negotiate a $300 deductible, add out-of-network benefits, and include a wellness program at no extra cost. These improvements stem from the broker’s ability to compare multiple insurers, highlight the group’s healthy claims history, and propose tailored solutions. The result? Annual savings of $10,000-$15,000 for the business, plus enhanced employee satisfaction.

Negotiating cost savings isn’t just about premiums; it’s also about optimizing plan structures. Brokers can identify inefficiencies in existing policies and propose adjustments that reduce long-term expenses. For example, they might recommend switching from a PPO to an HMO for a low-risk group, cutting costs by 15% without compromising essential coverage. Alternatively, they could negotiate higher employer contributions to HSAs (Health Savings Accounts), effectively lowering employees’ out-of-pocket expenses. These strategic moves require a deep understanding of plan mechanics and insurer flexibility, which brokers possess.

To maximize broker-driven savings, clients should provide detailed information about their health needs, budget constraints, and risk tolerance. Brokers need this data to craft persuasive negotiation arguments. For instance, a family with no chronic conditions might benefit from a high-deductible plan paired with a broker-negotiated HSA contribution. Conversely, a group with frequent medical needs could secure a lower deductible and broader prescription coverage. Transparency and collaboration are key to unlocking these savings.

While brokers charge fees or commissions, their negotiated savings often outweigh these costs. A study by the National Association of Health Underwriters found that broker-assisted plans saved businesses an average of 18% on premiums compared to direct purchases. For individuals, brokers can identify subsidies or tax credits that further reduce costs. Ultimately, their value lies in transforming opaque insurance markets into opportunities for tangible financial relief, making them a worthwhile investment for many.

JD Towing Insurance Company in Shreveport, LA: Who Are They?

You may want to see also

Explore related products

![]()

Access to exclusive insurance plans

One of the most compelling reasons to consider a health insurance broker is their ability to unlock access to exclusive insurance plans not available to the general public. These plans, often negotiated through broker-specific partnerships with insurers, can offer tailored benefits, lower premiums, or unique coverage options that cater to specific health needs or lifestyles. For instance, a broker might secure a plan with enhanced mental health coverage, waived deductibles for preventive care, or discounted rates for wellness programs. This level of customization is rarely achievable when purchasing insurance directly from a provider or through a public marketplace.

Consider the case of a self-employed individual in their 40s who requires comprehensive coverage for chronic condition management. A broker could identify an exclusive plan that includes access to specialist networks, prescription drug discounts, and telehealth services at no additional cost. Without a broker, this individual might settle for a standard plan that lacks these critical features, potentially leading to higher out-of-pocket expenses and inadequate care. The broker’s role here is not just transactional but consultative, ensuring the plan aligns with the client’s long-term health and financial goals.

However, accessing these exclusive plans isn’t without its caveats. Brokers typically earn commissions from insurers, which could influence the plans they recommend. To mitigate this, clients should ask brokers to disclose all available options, including non-exclusive plans, and compare them objectively. Additionally, some exclusive plans may require higher income thresholds or specific eligibility criteria, limiting accessibility for certain demographics. It’s essential to clarify these details upfront to avoid surprises during enrollment.

For those weighing the value of a broker, the takeaway is clear: exclusive plans can offer significant advantages, but they require careful evaluation. Start by defining your health priorities—whether it’s affordability, comprehensive coverage, or access to specific providers. Then, engage a broker with a proven track record in securing exclusive plans. Ask for case studies or testimonials from clients with similar needs to gauge their expertise. Finally, review the plan’s fine print, including exclusions and renewal terms, to ensure it remains a good fit over time. With the right approach, a broker’s access to exclusive plans can transform health insurance from a commodity into a personalized tool for well-being.

Understanding the Role of a Financial Advisor in Insurance Companies

You may want to see also

Explore related products

$15.89

![]()

Personalized policy recommendations

Health insurance brokers often shine in their ability to provide personalized policy recommendations, a service that can be invaluable in navigating the complex landscape of healthcare plans. Unlike generic online comparison tools, brokers leverage their expertise and access to multiple carriers to tailor options to your specific needs. For instance, a 35-year-old freelancer with no dependents might benefit from a high-deductible health plan (HDHP) paired with a health savings account (HSA), while a family of four with chronic conditions could save significantly with a comprehensive PPO plan that includes lower out-of-pocket costs for specialist visits.

The process begins with a detailed assessment of your health, financial situation, and lifestyle. Brokers ask pointed questions: Do you anticipate frequent doctor visits? Are you planning to start a family? What prescription medications do you take? By analyzing this data, they can identify plans that align with your current and future needs. For example, a broker might recommend a plan with robust maternity coverage for a couple planning to expand their family, or suggest a policy with lower premiums but higher copays for a healthy individual who rarely sees a doctor.

One of the most significant advantages of personalized recommendations is the potential for cost savings. Brokers can uncover hidden benefits or exclusions that might not be immediately apparent. For instance, a plan with a slightly higher monthly premium might offer better coverage for preventive care, saving you money in the long run if you prioritize regular check-ups. Conversely, they can flag plans that exclude specific treatments or medications, preventing costly surprises down the line.

However, it’s essential to approach personalized recommendations with a critical eye. While brokers are incentivized to find the best fit for you, they also earn commissions from carriers. To ensure transparency, ask your broker to disclose any potential conflicts of interest and request a breakdown of how they selected the recommended plans. Additionally, don’t hesitate to compare their suggestions with other options independently. Tools like Healthcare.gov or state-specific marketplaces can provide a broader perspective, though they lack the personalized touch of a broker.

Ultimately, personalized policy recommendations from a health insurance broker can be a game-changer, especially for those overwhelmed by the sheer volume of options. By combining their industry knowledge with your unique circumstances, brokers can simplify the decision-making process and help you secure a plan that offers both coverage and value. If you’re unsure where to start or feel daunted by the complexity of health insurance, consulting a broker could be a worthwhile investment in your health and financial well-being.

Employee Insurance and Medicaid: Can Spouses Mix Coverage?

You may want to see also

Explore related products

$26.99

![]()

Time-saving assistance with paperwork

Navigating the labyrinth of health insurance paperwork can consume hours, if not days, of your time. Applications, policy documents, and claims forms are riddled with jargon and fine print that demand meticulous attention. This is where health insurance brokers step in as time-saving allies. By handling the paperwork on your behalf, they free you to focus on what truly matters—your health and well-being. Their expertise ensures that forms are completed accurately and submitted on time, minimizing the risk of delays or rejections. For instance, a broker can streamline the process of comparing plans, filling out enrollment forms, and even assisting with claims, saving you an average of 10–15 hours per year.

Consider the complexity of enrolling in a health insurance plan. You’re required to provide detailed personal and financial information, select coverage options, and understand terms like deductibles, copays, and out-of-pocket maximums. A broker acts as your personal guide, simplifying these steps and ensuring compliance with regulatory requirements. They also handle follow-ups with insurers, eliminating the back-and-forth that often frustrates individuals. For example, if you’re self-employed or transitioning between jobs, a broker can manage COBRA paperwork or help you navigate the Health Insurance Marketplace, saving you from hours of confusion and potential errors.

The value of this time-saving assistance becomes even clearer during claims processing. Filing a claim often involves gathering medical bills, receipts, and other documentation, which can be overwhelming, especially during a health crisis. Brokers take charge of this process, ensuring all necessary paperwork is submitted correctly and promptly. They also act as advocates, resolving disputes with insurers on your behalf. A study found that individuals who used brokers for claims processing saved an average of 8 hours per claim compared to those who handled it themselves. This efficiency not only saves time but also reduces stress during an already challenging period.

For families or individuals with specific healthcare needs, the paperwork burden can be exponentially higher. Brokers tailor their assistance to your unique situation, whether you’re enrolling a child in a new plan, adding a spouse, or managing chronic conditions. They ensure that all necessary forms, such as those for pre-existing conditions or specialized treatments, are completed accurately. For example, a broker can help a family of four navigate the paperwork for pediatric dental coverage, vision care, and annual check-ups, saving them from juggling multiple forms and deadlines.

In conclusion, the time-saving assistance with paperwork provided by health insurance brokers is a significant benefit that justifies their value. By handling enrollment, claims, and other administrative tasks, they allow you to reclaim hours of your life while ensuring accuracy and compliance. Whether you’re an individual, a family, or a business owner, the efficiency and expertise of a broker can transform a tedious, error-prone process into a seamless experience. If you value your time and peace of mind, partnering with a broker is a practical and worthwhile investment.

Top Life Insurance Providers Offering Starter Draw Benefits Explained

You may want to see also

Explore related products

![]()

Ongoing support for claims and changes

Health insurance policies are complex, and navigating claims or policy changes can be overwhelming. This is where ongoing support from a broker becomes invaluable. Unlike direct purchases, brokers act as your advocate throughout the policy lifecycle, not just during the initial sale. They understand the intricacies of different plans and can guide you through the claims process, ensuring you receive the maximum benefits you're entitled to.

Imagine a scenario: you're hospitalized and facing a mountain of medical bills. A broker can help decipher your policy's coverage, assist with claim submission, and even negotiate with the insurance company on your behalf. This support can significantly reduce stress and potentially save you money.

The value of ongoing support extends beyond claims. Life circumstances change – you might get married, have a child, or change jobs. A good broker will proactively review your policy annually, ensuring it still meets your evolving needs. They can help you understand how life events impact your coverage and recommend adjustments to maintain adequate protection. For instance, a broker can guide you through adding a newborn to your policy, ensuring they're covered from day one, or help you navigate the complexities of COBRA if you lose employer-sponsored insurance.

This proactive approach prevents coverage gaps and ensures you're not overpaying for unnecessary benefits.

While some may argue that online resources and customer service hotlines can provide similar support, brokers offer a personalized touch. They build a relationship with you, understand your specific situation, and advocate for your best interests. This personalized guidance can be particularly beneficial for those with complex medical histories or unique coverage needs.

Business School: Navigating Medical Insurance

You may want to see also

Frequently asked questions

Yes, health insurance brokers are often worth the cost because they provide personalized guidance, help you compare plans, and ensure you find coverage tailored to your needs, often at no additional expense since they are typically paid by insurance companies.

A: Yes, brokers can help you save money by identifying plans with lower premiums, better benefits, or available subsidies, leveraging their market knowledge to find the best value for your budget.

A: In most cases, health insurance brokers do not charge fees to consumers. They are compensated by insurance companies through commissions, making their services free for you to use.

A: Using a broker is often better because they offer unbiased advice, access to multiple insurers, and expertise in navigating complex policies, whereas buying directly limits you to one company’s offerings.