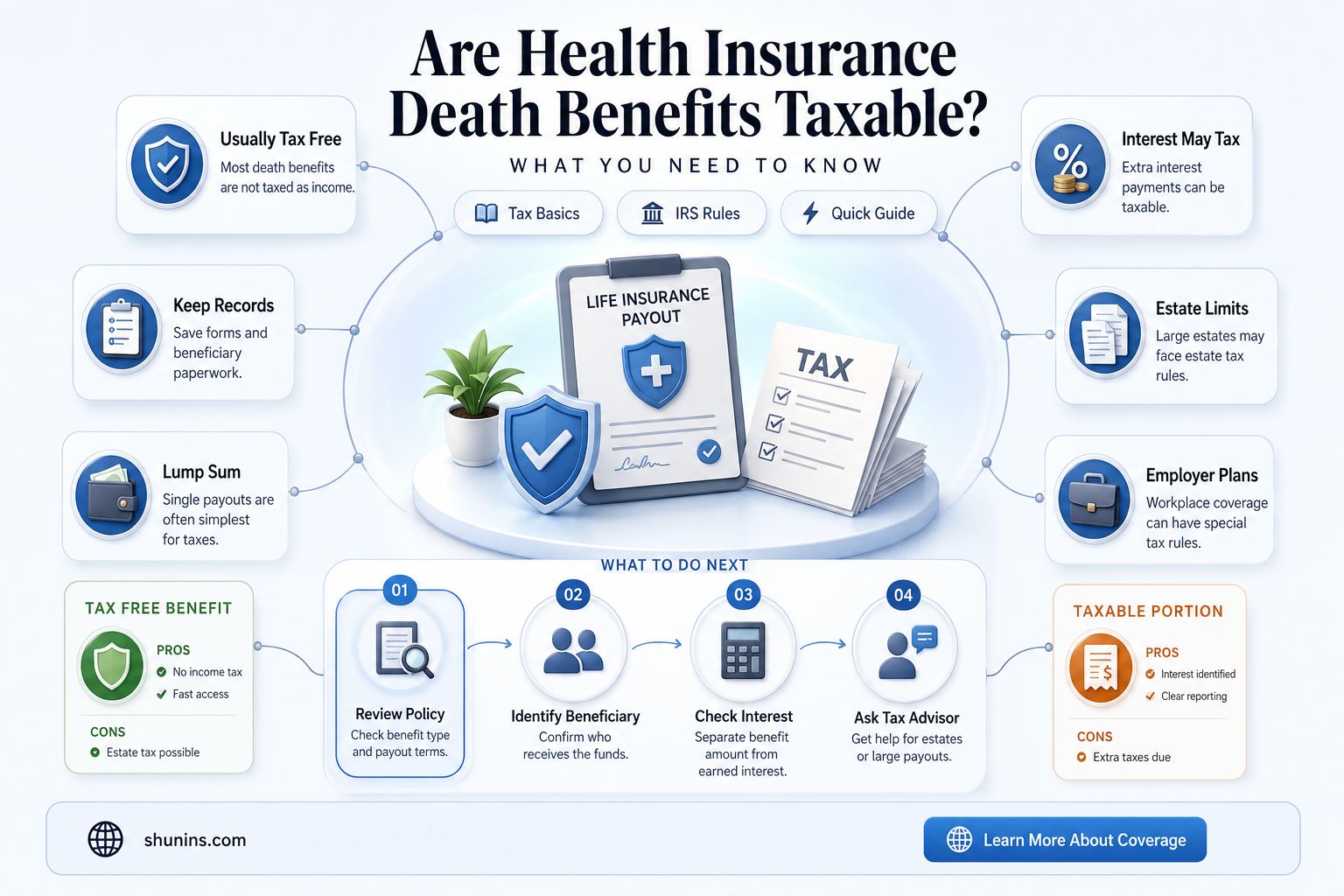

Health insurance death benefits, which are typically paid out to beneficiaries upon the policyholder's death, often raise questions about their tax implications. Generally, life insurance proceeds are not considered taxable income for the recipient under federal law, as they are viewed as a return of premiums rather than earnings. However, there are exceptions, such as if the benefits are paid in installments with interest or if the policy was transferred for valuable consideration. Additionally, while federal taxes may not apply, state-level taxes could vary, and beneficiaries should consult tax professionals to understand their specific obligations. Understanding these nuances is crucial for proper financial planning and compliance.

| Characteristics | Values |

|---|---|

| Taxability of Death Benefits | Generally not taxable as income to the beneficiary. |

| Type of Policy | Health insurance policies typically do not include death benefits. |

| Life Insurance Death Benefits | Tax-free to the beneficiary under most circumstances (U.S. federal law). |

| Exceptions | If the beneficiary is an estate or corporation, taxes may apply. |

| Interest on Death Benefits | Any interest accrued on delayed payouts may be taxable. |

| Estate Tax Considerations | Death benefits may be included in the deceased's estate for estate tax purposes. |

| State-Specific Rules | Some states may have additional tax regulations on death benefits. |

| Employer-Provided Coverage | Group life insurance benefits through employers are usually tax-free. |

| IRS Guidelines | IRS Code Section 101(a)(1) exempts most life insurance death benefits from income tax. |

| Health Insurance vs. Life Insurance | Health insurance does not typically provide death benefits; life insurance does. |

| Tax Reporting Requirements | Beneficiaries generally do not need to report death benefits on tax returns. |

Explore related products

What You'll Learn

![]()

Taxability of Lump-Sum Death Benefits

Lump-sum death benefits from health insurance policies often leave beneficiaries uncertain about their tax implications. Generally, these benefits are not taxable as income to the recipient. The Internal Revenue Service (IRS) classifies them as a return of premiums paid, not as income. For instance, if a policyholder paid $10,000 in premiums over their lifetime and the beneficiary receives a $50,000 lump sum, the $10,000 portion representing premiums is tax-free, while the remaining $40,000 may be subject to taxation depending on the policy’s structure. However, most health insurance death benefits are fully tax-exempt because they are considered a reimbursement of expenses rather than a gain.

Understanding the exceptions is crucial. If the lump-sum benefit exceeds the total premiums paid and is structured as an investment or annuity component, the excess may be taxable. For example, some policies offer accrued interest or investment gains, which could trigger tax liability. Beneficiaries should review the policy’s terms or consult a tax professional to determine if any portion of the benefit falls into this category. Additionally, if the benefit is paid to an estate rather than an individual, estate taxes may apply, though this is separate from income tax considerations.

Practical steps for beneficiaries include obtaining a detailed breakdown of the benefit from the insurer, identifying the portion tied to premiums versus any additional payouts, and filing IRS Form 1099-R if applicable. For example, if a beneficiary receives a $75,000 lump sum where $15,000 represents accrued interest, the insurer will report the $15,000 on Form 1099-R, and the beneficiary must declare it as taxable income. Keeping thorough records and understanding the policy’s structure can prevent unexpected tax liabilities.

A comparative analysis reveals that lump-sum death benefits from health insurance differ from those of life insurance. While health insurance benefits are typically tax-free, life insurance payouts are almost always exempt from income tax unless the policy has a cash value component. This distinction highlights the importance of knowing the type of policy involved. For instance, a $100,000 life insurance payout is tax-free, but if a health insurance policy includes a $20,000 cash value, that portion might be taxable. Beneficiaries should differentiate between these policies to avoid confusion.

Finally, a descriptive overview of real-world scenarios underscores the need for clarity. Imagine a 65-year-old retiree whose spouse receives a $30,000 lump-sum benefit from a health insurance policy. Without understanding the tax rules, the spouse might mistakenly assume the entire amount is taxable. However, if the policy was purely for health coverage with no investment component, the full $30,000 is tax-free. This example illustrates how knowledge of tax laws can alleviate financial stress during an already difficult time. Always verify the policy’s nature and consult a professional when in doubt.

Understanding Third-Party Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Exclusion Rules for Beneficiaries

Health insurance death benefits, often paid as a lump sum to beneficiaries, are generally tax-free under U.S. federal law. However, exclusion rules for beneficiaries can complicate this straightforward principle. These rules hinge on the type of policy, the beneficiary’s relationship to the insured, and how the benefit is structured. For instance, employer-sponsored group life insurance policies typically exclude the first $50,000 of death benefits from taxation, but amounts exceeding this threshold may be taxable if the beneficiary paid the premiums. Understanding these nuances is critical to avoiding unexpected tax liabilities.

One key exclusion rule revolves around the "transfer-for-value" exception. If a policy is transferred to another party for valuable consideration (e.g., sold or gifted), the death benefit may become taxable to the beneficiary. For example, if a parent sells their life insurance policy to an investor, the proceeds paid to the investor upon the parent’s death could be subject to income tax. This rule underscores the importance of documenting policy ownership and transfers carefully. Beneficiaries should verify whether the policy falls under this exception to ensure proper tax treatment.

Another exclusion rule pertains to policies owned by businesses. If a corporation owns a life insurance policy on an employee and names itself as the beneficiary, the death benefit may be taxable as ordinary income. However, if the policy is part of a qualified employer-owned life insurance plan and meets specific IRS requirements, such as employee consent, the benefit remains tax-free. Small business owners and beneficiaries should scrutinize policy ownership and beneficiary designations to avoid unintended tax consequences.

Practical tips for beneficiaries include requesting a copy of the insurance policy to confirm ownership, beneficiary status, and premium payment history. If the benefit exceeds $50,000 and the beneficiary paid premiums, consult a tax professional to determine taxable portions. Additionally, beneficiaries should retain documentation of any policy transfers or assignments to prove compliance with exclusion rules. Proactive steps like these can safeguard the tax-free status of death benefits and prevent disputes with the IRS.

In summary, while health insurance death benefits are often tax-free, exclusion rules for beneficiaries demand careful attention. From the transfer-for-value exception to business-owned policies, these rules create potential pitfalls for the unwary. By understanding these specifics and taking proactive measures, beneficiaries can ensure they receive the full, intended value of the benefit without unexpected tax burdens.

Adding Medical Insurance Accounts to Quicken: A Guide

You may want to see also

Explore related products

![]()

Impact of Policy Ownership

The ownership of a health insurance policy plays a pivotal role in determining the taxability of death benefits. When the policyholder owns the policy, the death benefit is generally not taxable to the beneficiary. This is because the Internal Revenue Service (IRS) considers the payout a tax-free inheritance rather than taxable income. For instance, if a 45-year-old individual owns a $500,000 life insurance policy and designates their spouse as the beneficiary, the spouse would receive the full amount tax-free upon the policyholder’s death. However, this straightforward rule becomes complicated when the policy is owned by someone other than the insured.

If the policy is owned by a third party, such as a trust, business, or another individual, the tax implications shift significantly. In these cases, the death benefit may be subject to income tax for the beneficiary. For example, if a business owns a key person insurance policy on an employee and receives the death benefit, the payout could be taxable as business income. Similarly, if a parent owns a policy on their adult child, the beneficiary might face unexpected tax liabilities. This underscores the importance of aligning policy ownership with the intended financial strategy to avoid unintended tax consequences.

Another critical aspect is the transfer of policy ownership during the insured’s lifetime. If a policy is transferred for valuable consideration (e.g., sold), the death benefit may become taxable to the beneficiary under IRS Section 101(a). For instance, if a 60-year-old sells their $1 million life insurance policy to an investor for $200,000, the beneficiary could owe taxes on the portion of the death benefit exceeding the policy’s basis. Conversely, if the transfer is a gift (e.g., from a parent to a child), the death benefit typically remains tax-free. Proper documentation and adherence to IRS guidelines are essential to navigate these scenarios effectively.

Practical tips for policyholders include reviewing ownership structures regularly, especially during life events like marriage, divorce, or business changes. For example, a divorced individual should ensure their ex-spouse is no longer listed as the policy owner to prevent complications. Additionally, consulting a tax advisor or estate planner can help optimize ownership to align with long-term financial goals. By proactively managing policy ownership, individuals can safeguard the tax-free status of death benefits and ensure their beneficiaries receive the full intended value.

In summary, policy ownership is a critical determinant of the taxability of health insurance death benefits. Whether owned by the insured, a third party, or transferred during life, the structure directly impacts the beneficiary’s tax liability. Understanding these nuances and taking strategic actions can preserve the financial security intended by the policy, making it a cornerstone of effective estate and tax planning.

Herpes Medication: Accessing Treatment Without Insurance Coverage

You may want to see also

Explore related products

![]()

Estate Tax Considerations

Health insurance death benefits, often paid as a lump sum to beneficiaries, are generally not considered taxable income at the federal level. However, when these benefits become part of an estate, they can trigger estate tax considerations that require careful planning. Estate tax is levied on the total value of a deceased person’s assets, and while the federal estate tax exemption is substantial ($12.92 million per individual in 2023), state-level estate or inheritance taxes may apply at much lower thresholds. For instance, in Massachusetts, the estate tax exemption is only $1 million, meaning estates valued above this amount could face significant tax liabilities.

One critical step in managing estate tax implications is understanding how health insurance death benefits are treated within the estate. If the policyholder designated a specific beneficiary, the proceeds typically pass directly to that person outside of probate, avoiding inclusion in the taxable estate. However, if the beneficiary is the estate itself or if the proceeds are payable to the estate by default, they become part of the taxable estate. This distinction is crucial, as it can push the estate’s total value over state or federal exemption limits, triggering taxes that could have been avoided with proper planning.

To mitigate potential estate tax liabilities, consider strategies such as irrevocable trusts or gifting. For example, transferring ownership of a life insurance policy to an irrevocable trust removes it from the estate, ensuring the death benefit remains tax-free. Similarly, gifting assets during lifetime can reduce the estate’s value, but be mindful of gift tax rules—individuals can gift up to $17,000 annually (as of 2023) per recipient without incurring gift tax. For married couples, portability of the estate tax exemption allows a surviving spouse to utilize the deceased spouse’s unused exemption, effectively doubling the threshold to $25.84 million in 2023.

A comparative analysis of state estate and inheritance taxes reveals significant variations. For instance, Pennsylvania imposes an inheritance tax with rates ranging from 4.5% to 15%, depending on the relationship of the beneficiary to the deceased. In contrast, Oregon has an estate tax with rates up to 16% and a low exemption of $1 million. Beneficiaries and estate planners must therefore consider both federal and state laws to optimize tax outcomes. For example, relocating to a state without estate or inheritance taxes, such as Florida or Texas, could be a strategic move for high-net-worth individuals.

In conclusion, while health insurance death benefits are typically tax-free at the federal income tax level, their treatment within an estate can have profound estate tax implications. Proactive planning, such as designating beneficiaries correctly, utilizing trusts, and understanding state-specific tax laws, is essential to minimize liabilities. For those with estates nearing or exceeding exemption thresholds, consulting an estate planning attorney or financial advisor can provide tailored strategies to protect assets and ensure beneficiaries receive the maximum intended benefit.

Medicare Hospital Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Treatment of Accelerated Death Benefits

Accelerated death benefits (ADBs) allow policyholders to access a portion of their life insurance payout while still alive, typically if diagnosed with a terminal or critical illness. The tax treatment of these benefits hinges on the policyholder’s health condition and the structure of the payout. Under the Internal Revenue Code (IRC) Section 101(g), ADBs are generally tax-free if the policyholder receives a certification from a licensed physician stating they have a life expectancy of 24 months or less. This provision ensures financial relief during dire medical circumstances without adding a tax burden.

However, the rules shift when ADBs are paid for chronic or critical illnesses not meeting the terminal illness criteria. In such cases, the benefits may be taxable as income unless they qualify under specific exceptions, such as those outlined in IRC Section 7702B. For instance, if the ADBs are used to cover long-term care expenses, they may be excluded from taxable income up to certain limits, typically tied to the cost of care. Policyholders must carefully document their expenses to ensure compliance with these regulations.

A critical distinction arises when comparing ADBs to traditional health insurance benefits. While health insurance payouts for medical treatments are generally tax-free, ADBs are treated differently because they are derived from life insurance policies. This distinction underscores the importance of understanding the source of the benefit. For example, if a policyholder receives $50,000 in ADBs for cancer treatment, the tax treatment depends on whether the diagnosis meets the terminal illness threshold or falls under a critical illness category.

Practical tips for navigating ADB taxation include consulting a tax professional to interpret the nuances of IRC provisions and maintaining detailed records of medical certifications and expenses. Policyholders should also review their insurance policies to understand the conditions under which ADBs are paid and how they align with tax laws. By proactively addressing these factors, individuals can maximize the financial support provided by ADBs while minimizing unexpected tax liabilities.

Wisdom Teeth Removal: Insurance Coverage and Costs

You may want to see also

Frequently asked questions

Health insurance death benefits are generally not taxable as income. They are typically considered tax-free because they are paid out to cover medical expenses or as a return of premiums, not as income.

Beneficiaries usually do not need to report health insurance death benefits on their tax returns, as these payments are not considered taxable income. However, it’s always a good idea to consult a tax professional for specific situations.

In rare cases, if the death benefit is paid as interest or if it exceeds the total premiums paid into the policy, the excess amount might be taxable. However, this is uncommon and typically applies to specific types of policies or situations.