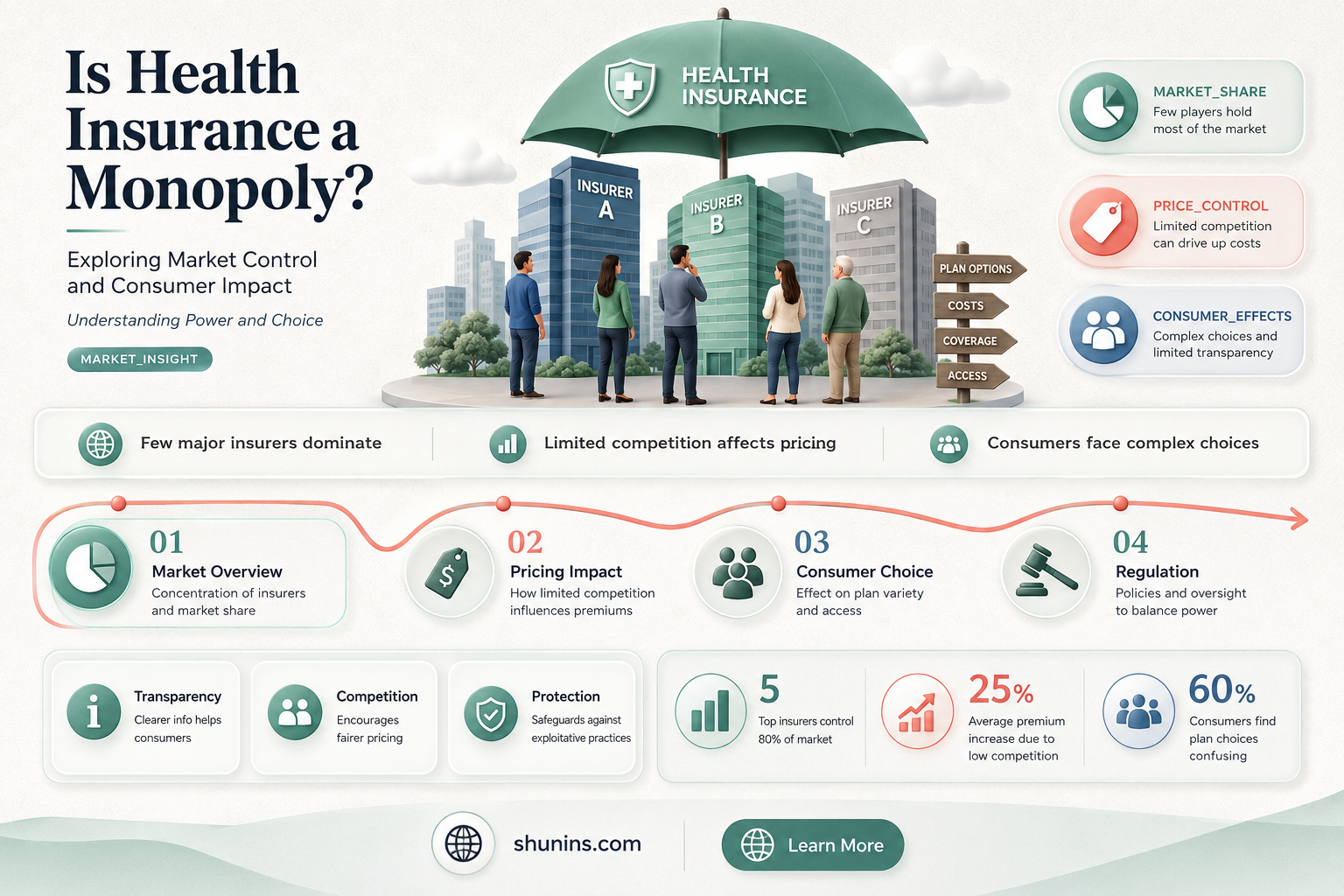

The question of whether health insurance constitutes a monopoly is a critical issue in the healthcare industry, as it directly impacts access, affordability, and quality of care for millions of individuals. In many regions, a handful of large insurance companies dominate the market, raising concerns about reduced competition, higher premiums, and limited consumer choice. This concentration of power can lead to inefficiencies, as insurers may prioritize profits over patient well-being, negotiate unfavorable terms with healthcare providers, or restrict coverage options. Critics argue that such monopolistic tendencies exacerbate existing disparities in healthcare access, particularly for low-income or marginalized communities. Conversely, proponents contend that larger insurers can leverage their scale to negotiate better rates with providers and offer more comprehensive plans. Understanding the dynamics of health insurance monopolies is essential for policymakers, consumers, and advocates seeking to reform the system and ensure equitable, affordable healthcare for all.

Explore related products

What You'll Learn

- Market Concentration: Examines how few insurers dominate, limiting consumer choice and competition

- Premium Pricing Power: Explores insurers' ability to set high premiums due to lack of alternatives

- Consumer Impact: Analyzes how monopolies affect access, affordability, and quality of healthcare

- Regulatory Challenges: Discusses government efforts to curb monopolistic practices in health insurance

- Alternatives to Monopoly: Investigates solutions like public options or increased market competition

![]()

Market Concentration: Examines how few insurers dominate, limiting consumer choice and competition

In the United States, the health insurance market is characterized by a high degree of concentration, with a handful of insurers controlling a significant portion of the market. According to the American Medical Association (AMA), in 2020, the top 5 health insurers accounted for 57% of the national market, and in 22 states, one insurer held at least 50% of the market share. This level of market concentration raises concerns about limited consumer choice, reduced competition, and potential negative impacts on healthcare affordability and quality.

Consider the following scenario: a 45-year-old individual in a rural area with a pre-existing condition seeks health insurance. Due to the dominant presence of a single insurer in their region, they may face limited plan options, higher premiums, and restricted access to preferred healthcare providers. This lack of competition can result in reduced negotiating power for consumers, as insurers have little incentive to lower prices or improve services. To mitigate these effects, consumers should research available plans, compare costs and benefits, and consider alternatives such as health sharing ministries or short-term health plans, although these options may not provide comprehensive coverage.

A comparative analysis of market concentration in urban versus rural areas reveals stark disparities. In urban centers, where multiple insurers compete, consumers often benefit from lower premiums and more plan options. In contrast, rural areas frequently experience higher market concentration, with one or two insurers dominating the landscape. This disparity highlights the need for targeted policy interventions, such as incentivizing insurer entry into underserved markets or promoting public options like Medicaid expansion. By addressing these geographic imbalances, policymakers can foster greater competition and improve consumer choice.

To illustrate the impact of market concentration, examine the case of Anthem, one of the largest health insurers in the U.S. In states where Anthem holds a significant market share, such as Indiana and Kentucky, consumers often face higher premiums and limited provider networks. A 2019 study by the Commonwealth Fund found that in highly concentrated markets, premiums were 10-15% higher than in more competitive markets. This evidence underscores the importance of monitoring market concentration and implementing measures to promote competition, such as antitrust enforcement and increased transparency in pricing and provider networks.

Finally, a persuasive argument for addressing market concentration in health insurance is its potential to improve overall healthcare outcomes. When consumers have access to a variety of insurers and plans, they are more likely to find coverage that meets their specific needs, leading to better health-seeking behavior and outcomes. For instance, a study published in Health Affairs found that increased competition in the health insurance market was associated with higher rates of preventive care utilization and improved chronic disease management. By prioritizing policies that reduce market concentration, such as encouraging insurer entry and promoting public options, stakeholders can create a more competitive environment that benefits both consumers and the healthcare system as a whole.

Dr. Kenneth Prushik: Understanding Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Premium Pricing Power: Explores insurers' ability to set high premiums due to lack of alternatives

Health insurance premiums have surged by an average of 55% over the past decade, outpacing inflation and wage growth. This trend raises a critical question: Do insurers exploit their market dominance to set exorbitant prices, knowing policyholders have few alternatives? In regions where one or two insurers control over 70% of the market, premiums often climb unchecked, leaving consumers with little choice but to pay or go uninsured. This dynamic underscores the concept of premium pricing power, a phenomenon where insurers leverage their monopolistic or oligopolistic positions to dictate costs.

Consider the case of rural counties, where a single insurer often dominates due to the high cost of market entry for competitors. In such areas, premiums for a family plan can exceed $20,000 annually, compared to $15,000 in more competitive urban markets. This disparity isn’t merely a reflection of higher healthcare costs but a strategic pricing decision enabled by the lack of alternatives. Insurers in these regions frequently justify higher premiums by citing limited provider networks or higher administrative costs, yet their profit margins often outstrip those in competitive markets. This pattern suggests that pricing power, rather than operational necessity, drives these increases.

To mitigate the impact of premium pricing power, consumers must adopt proactive strategies. First, compare plans annually during open enrollment, even if switching seems inconvenient. Tools like Healthcare.gov or state-based exchanges provide side-by-side comparisons of premiums, deductibles, and out-of-pocket maximums. Second, consider high-deductible health plans paired with health savings accounts (HSAs), which can reduce premiums by 20-30% while offering tax advantages. For those aged 50 and older, explore Medicare Advantage plans, which often include prescription drug coverage and additional benefits like dental care at lower costs than private insurance.

However, individual actions alone cannot fully address the systemic issue of premium pricing power. Policymakers must intervene by fostering competition through measures like expanding Medicaid, incentivizing insurers to enter underserved markets, and capping premium increases. For instance, states like California and New York have implemented rate review programs that require insurers to justify premium hikes, resulting in reductions of up to 10% in proposed increases. Such regulatory frameworks demonstrate that, with oversight, insurers’ pricing power can be curbed, ensuring affordability without compromising access to care.

Ultimately, the ability of insurers to set high premiums due to a lack of alternatives highlights a market failure that demands both individual vigilance and collective action. While consumers can navigate this landscape through informed decision-making, lasting change requires structural reforms that promote competition and transparency. Until then, premium pricing power will remain a stark reminder of the imbalance between insurers and those they insure.

Medicaid Insurance Eligibility: Understanding the Asset Test

You may want to see also

Explore related products

![Winning Moves Back To The Future Monopoly [GRA PLANSZOWA] - Board Game - 2 Players - Age 6+](https://m.media-amazon.com/images/I/71nG40nhQAL._AC_UL320_.jpg)

![]()

Consumer Impact: Analyzes how monopolies affect access, affordability, and quality of healthcare

Health insurance monopolies can significantly limit consumer choice, often leaving individuals with only one or two providers in their region. This lack of competition frequently results in higher premiums, as insurers face no market pressure to keep prices competitive. For instance, in areas dominated by a single insurer, premiums can be up to 30% higher than in markets with multiple competitors. Such price increases disproportionately affect low-income families, who may be forced to choose between insurance and other essential expenses like rent or groceries.

Consider the impact on access to care. Monopolistic insurers often dictate which providers are in-network, limiting patients’ ability to see specialists or preferred doctors. A study in *Health Affairs* found that in monopoly markets, 40% of consumers reported difficulty finding in-network providers for critical services like mental health or oncology. This barrier to access can delay treatment, worsen health outcomes, and increase long-term healthcare costs. For example, a 45-year-old with diabetes might struggle to find an endocrinologist in-network, leading to poorly managed blood sugar levels and potential complications like neuropathy or kidney disease.

Affordability suffers not just from high premiums but also from restrictive coverage policies. Monopolies often design plans with high deductibles and narrow drug formularies, shifting more costs onto consumers. A practical tip for those in such markets: review your plan’s drug list annually and discuss generic alternatives with your doctor. For instance, switching from a brand-name statin to a generic version can save $50–$100 monthly, a significant reduction for those on fixed incomes.

Quality of care is another casualty of monopolies. Without competition, insurers have less incentive to invest in preventive services or innovative treatments. Comparative analysis shows that regions with competitive insurance markets offer more comprehensive wellness programs, such as free annual check-ups or discounted gym memberships. In contrast, monopoly markets often prioritize profit over patient outcomes, leading to lower consumer satisfaction scores. A 2022 JAMA study revealed that patients in monopoly markets were 20% less likely to report positive healthcare experiences compared to those in competitive markets.

To mitigate these effects, consumers in monopoly markets should advocate for policy changes, such as antitrust legislation or public insurance options. Additionally, leveraging tools like Healthcare.gov’s plan comparison feature can help identify the best available coverage. For those over 65, exploring Medicare Advantage plans might offer more flexibility than private insurers. While monopolies pose significant challenges, informed decision-making and collective action can help consumers navigate this complex landscape.

Mortgage Insurance Without Medical Exams: Is It Possible?

You may want to see also

Explore related products

![]()

Regulatory Challenges: Discusses government efforts to curb monopolistic practices in health insurance

Government intervention in the health insurance market aims to dismantle monopolistic structures that stifle competition and inflate costs. One key strategy involves enforcing antitrust laws, such as the Sherman Act, to prevent mergers that would create dominant entities. For instance, the Department of Justice blocked the proposed merger between Aetna and Humana in 2017, citing concerns that it would reduce competition and harm consumers. This action underscores the government’s role in safeguarding market diversity, ensuring that no single insurer can dictate prices or limit consumer choice.

Another regulatory approach is the implementation of state-level insurance exchanges under the Affordable Care Act (ACA). These exchanges foster competition by providing a platform for multiple insurers to offer plans, enabling consumers to compare prices and coverage. However, challenges arise when insurers exit unprofitable markets, leaving some regions with limited options. For example, in 2023, several counties in Mississippi had only one insurer on their exchange, highlighting the delicate balance between regulation and market sustainability.

Legislative efforts also focus on price transparency and rate review processes. States like California and New York require insurers to justify premium increases, with regulators having the authority to reject unjustified hikes. This mechanism acts as a check on monopolistic pricing behavior, though it often faces pushback from insurers who argue it stifles innovation. Practical tips for consumers include leveraging these regulatory tools by reporting excessive rate increases to state insurance departments and using exchange platforms to explore all available options.

Despite these measures, regulatory challenges persist due to the complexity of the healthcare ecosystem. Insurers often consolidate through vertical integration, acquiring healthcare providers to control costs, which can blur the lines between competition and efficiency. Policymakers must navigate this gray area, ensuring that integration benefits consumers without fostering monopolistic control. For instance, the Federal Trade Commission (FTC) scrutinizes such mergers to assess their impact on market competition, but the process is resource-intensive and often reactive rather than proactive.

In conclusion, government efforts to curb monopolistic practices in health insurance are multifaceted but face significant hurdles. While antitrust enforcement, state exchanges, and rate reviews provide critical tools, their effectiveness depends on consistent application and adaptability to evolving market dynamics. Consumers can empower themselves by staying informed about regulatory protections and actively engaging with available resources to make informed choices in an increasingly complex landscape.

Who Relies on American Life and Health Insurance Company?

You may want to see also

Explore related products

![]()

Alternatives to Monopoly: Investigates solutions like public options or increased market competition

The dominance of a few players in the health insurance market has sparked debates about the need for alternatives to break the monopoly. One proposed solution is the introduction of a public option, a government-run health insurance plan that competes alongside private insurers. This approach aims to increase choice and affordability for consumers, particularly those who struggle to find suitable coverage in the current market. For instance, a public option could offer standardized plans with comprehensive benefits, including mental health services and prescription drug coverage, at a lower cost by leveraging the government's negotiating power.

To implement a public option effectively, policymakers must consider several factors. First, the plan's design should address the specific needs of underserved populations, such as low-income individuals and those with pre-existing conditions. Second, funding mechanisms, such as payroll taxes or premiums, need to be carefully structured to ensure financial sustainability without burdening taxpayers. Lastly, the public option should be integrated into existing healthcare infrastructure to minimize disruption and maximize efficiency. For example, it could build on the framework of Medicare, utilizing its provider networks and payment systems.

Another strategy to counter health insurance monopolies is fostering increased market competition. This can be achieved by lowering barriers to entry for new insurers, such as streamlining regulatory processes and reducing administrative costs. Encouraging the growth of nonprofit health insurance cooperatives is one practical step. These cooperatives, owned and operated by their members, often prioritize affordability and community needs over profit margins. For instance, a cooperative in Minnesota successfully reduced premiums by 20% for its members by negotiating bulk rates with healthcare providers.

However, increasing competition alone may not suffice without addressing underlying market failures. Regulators must enforce antitrust laws to prevent anti-competitive practices, such as mergers that reduce consumer choice. Additionally, transparency initiatives, like public reporting of insurer performance metrics, can empower consumers to make informed decisions. For example, a state-run website comparing insurers based on cost, coverage, and customer satisfaction could drive market accountability.

In conclusion, breaking health insurance monopolies requires a multi-faceted approach. Public options offer a direct means to enhance affordability and accessibility, while increased market competition can drive innovation and consumer choice. By combining these strategies with targeted regulatory measures, policymakers can create a more equitable and efficient health insurance landscape. Practical steps, such as designing inclusive public plans and supporting nonprofit cooperatives, provide actionable pathways toward this goal. Ultimately, the key lies in balancing government intervention with market dynamics to ensure that healthcare remains a right, not a privilege.

Medicare Insurance: What Policies Are Permanent?

You may want to see also

Frequently asked questions

A health insurance monopoly occurs when a single company or entity dominates the market, leaving consumers with little to no alternative options for coverage. This can result in higher premiums, limited choices, and reduced competition.

While no single health insurance company has a complete monopoly nationwide, some regions may have dominant players with significant market share. However, the U.S. has multiple insurers competing in most areas, preventing a true monopoly.

A monopoly can lead to higher costs, reduced innovation, and limited plan options for consumers. Without competition, insurers may prioritize profits over customer needs, resulting in poorer service and coverage.

Yes, government regulations, such as antitrust laws and market oversight, can help prevent monopolies by promoting competition and ensuring fair practices. Policies like the Affordable Care Act (ACA) also aim to increase consumer choices and affordability.