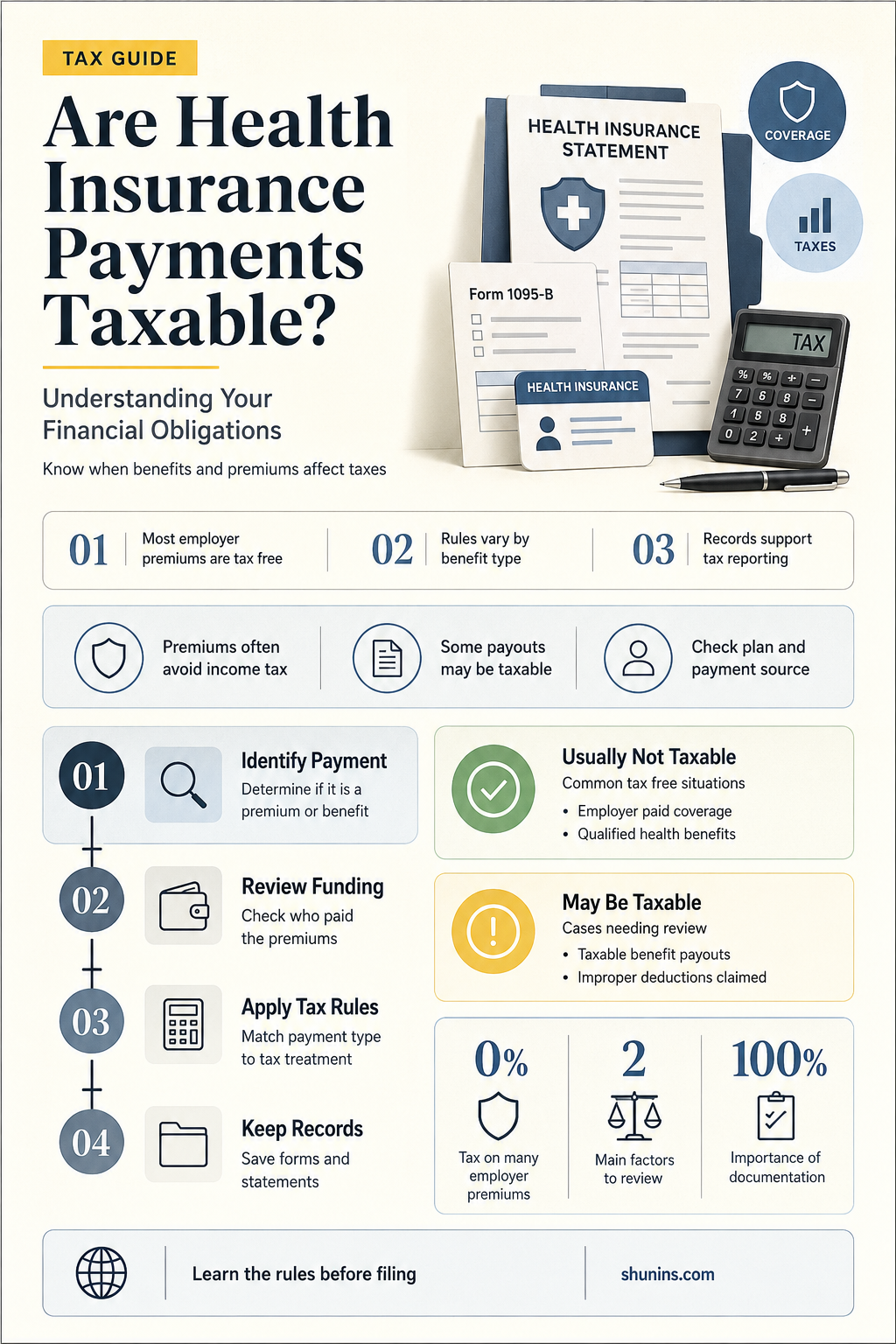

Health insurance payments are a critical aspect of financial planning, but understanding their tax implications can be complex. Many individuals wonder whether the premiums they pay for health insurance are taxable to them. Generally, health insurance premiums paid by individuals with their own after-tax dollars are not considered taxable income. However, if an employer pays for part or all of an employee’s health insurance, the value of this benefit may be tax-free to the employee under certain conditions, such as being part of a qualified employer-sponsored plan. Additionally, reimbursements from health insurance policies for medical expenses are typically not taxable, as they are considered a return of premiums rather than income. It’s essential to consult tax laws or a professional to navigate specific scenarios, as exceptions and nuances may apply depending on the type of insurance and payment structure.

| Characteristics | Values |

|---|---|

| Taxability of Premiums Paid by Employer | Generally tax-free to the employee under employer-provided group health insurance plans (Internal Revenue Code Section 106). |

| Taxability of Individual Premiums | Premiums paid by individuals with after-tax dollars are not tax-deductible unless itemized and exceed 7.5% of adjusted gross income (AGI) for 2023. |

| Health Savings Account (HSA) Contributions | Contributions to HSAs are tax-deductible, and qualified medical expenses (including premiums in certain cases) are tax-free. |

| Affordable Care Act (ACA) Subsidies | Premium tax credits (subsidies) reduce taxable income for eligible individuals purchasing insurance through ACA marketplaces. |

| Self-Employed Individuals | Health insurance premiums are deductible above the line, reducing taxable income directly. |

| Reimbursements (e.g., FSA/HRA) | Reimbursements for qualified medical expenses through Flexible Spending Accounts (FSAs) or Health Reimbursement Arrangements (HRAs) are tax-free. |

| COBRA Premiums | Premiums paid under COBRA are treated the same as employer-provided insurance if the employer continues to contribute; otherwise, taxable if paid with pre-tax dollars. |

| Medicare Premiums | Premiums for Medicare Part B and Part D may be tax-deductible if itemized and meet AGI thresholds. |

| Long-Term Care Insurance | Premiums may be tax-deductible up to certain limits based on age, if itemized and meet AGI criteria. |

| Taxable Benefits | Health insurance benefits received (e.g., reimbursements for non-qualified expenses) may be taxable as income. |

| 2023 Tax Year Updates | No significant changes to health insurance taxability rules; thresholds and limits adjusted for inflation. |

Explore related products

What You'll Learn

- Employer-Paid Premiums: Are employer contributions to health insurance taxable as income

- Self-Employed Deductions: Can self-employed individuals deduct health insurance premiums from taxes

- Taxable Benefits: Are health insurance payouts or reimbursements considered taxable income

- ACA Subsidies: Are Affordable Care Act premium tax credits taxable

- HSAs & Taxes: Are contributions to Health Savings Accounts tax-deductible

![]()

Employer-Paid Premiums: Are employer contributions to health insurance taxable as income?

In the United States, employer-paid health insurance premiums are generally not taxable as income to the employee. This tax exclusion is a significant benefit for both employers and employees, as it reduces the overall cost of providing health insurance. According to the Internal Revenue Service (IRS), employer contributions to health insurance plans are excluded from an employee’s gross income under Section 106 of the Internal Revenue Code. This means that the value of the employer’s premium payments does not need to be reported as taxable wages on the employee’s Form W-2. For example, if an employer pays $500 per month toward an employee’s health insurance, that $500 is not considered part of the employee’s taxable income, effectively lowering their tax liability.

However, there are exceptions and nuances to this rule. One key exception is for highly compensated individuals, such as executives or business owners, whose employer-paid premiums might be subject to taxation if the plan is considered discriminatory. The IRS scrutinizes plans that disproportionately benefit higher-paid employees, and in such cases, the value of the premiums may be included in the employee’s taxable income. Additionally, if an employer reimburses an employee for individual health insurance premiums through a health reimbursement arrangement (HRA) that does not meet specific IRS criteria, those reimbursements could also be taxable. Understanding these exceptions is crucial for both employers and employees to avoid unexpected tax consequences.

From a practical standpoint, employees should verify how their employer’s health insurance contributions are structured. Most group health plans offered by employers fall under the tax-free exclusion, but it’s always wise to confirm with the HR department or a tax professional. For self-employed individuals or those whose employers do not offer group health insurance, the rules differ. Self-employed individuals can deduct health insurance premiums above the line on their tax returns, but this is not the same as an employer-paid exclusion. Employees should also be aware that while the premiums themselves are tax-free, other benefits, such as flexible spending account (FSA) contributions or certain wellness program incentives, may have different tax treatments.

Comparatively, other countries handle employer-paid health insurance premiums differently. In Canada, for instance, employer contributions to private health insurance plans are generally considered a taxable benefit unless the plan meets specific provincial or territorial criteria. In contrast, the U.K.’s National Health Service (NHS) provides universal coverage, making employer-paid private health insurance a taxable perk. These international variations highlight the importance of understanding local tax laws when evaluating the value of employer-provided health benefits.

In conclusion, employer-paid health insurance premiums are typically tax-free for employees in the U.S., offering a valuable financial advantage. However, employees must remain vigilant about potential exceptions, especially if they are highly compensated or part of a non-compliant plan. By staying informed and seeking professional advice when necessary, individuals can maximize the benefits of their employer-sponsored health insurance while avoiding tax pitfalls. This knowledge not only ensures compliance but also empowers employees to make informed decisions about their healthcare coverage.

Affording Medication: Strategies Without Insurance

You may want to see also

Explore related products

![]()

Self-Employed Deductions: Can self-employed individuals deduct health insurance premiums from taxes?

Self-employed individuals often face unique financial challenges, particularly when it comes to managing healthcare costs. One critical question arises: Can they deduct health insurance premiums from their taxes? The answer is yes, but with specific conditions. According to the IRS, self-employed taxpayers can deduct premiums paid for medical, dental, and qualifying long-term care insurance for themselves, their spouses, and dependents. This deduction is an above-the-line adjustment, meaning it reduces adjusted gross income (AGI) and can be claimed even if the taxpayer doesn’t itemize deductions. However, the self-employed individual must report a net profit on Schedule C, Schedule F, or Schedule K-1 to qualify.

To claim this deduction, self-employed individuals must meet certain criteria. First, the insurance plan must be established under the taxpayer’s business or industry. Second, the premiums cannot be reimbursed by another source, such as a spouse’s employer-sponsored plan. For example, if a self-employed graphic designer pays $600 monthly for a family health insurance plan and has no other coverage, they can deduct the full $7,200 annually. This deduction can significantly reduce taxable income, providing substantial savings.

A common misconception is that health savings account (HSA) contributions and health insurance premiums are treated the same for tax purposes. While both offer tax advantages, they differ in structure. HSA contributions are tax-deductible and grow tax-free, but they require enrollment in a high-deductible health plan. In contrast, the health insurance premium deduction is straightforward and does not depend on the type of plan. Self-employed individuals should carefully evaluate their healthcare needs and financial situation to determine the best approach.

Practical tips can maximize this deduction’s benefit. First, maintain detailed records of all premium payments, including receipts and policy documents. Second, consult a tax professional to ensure compliance with IRS rules, especially if business profits fluctuate. Third, consider timing premium payments strategically—for instance, paying the full year’s premium in December to maximize the deduction for the current tax year. By leveraging this deduction effectively, self-employed individuals can offset a portion of their healthcare expenses and improve their overall financial health.

In conclusion, self-employed individuals have a valuable tool in the health insurance premium deduction to manage their tax liabilities. While the rules are clear, careful planning and documentation are essential to avoid pitfalls. By understanding and applying this deduction, self-employed taxpayers can achieve significant savings, making healthcare more affordable and their businesses more sustainable.

Disputing Medical Bills: Navigating Insurance Claims and Disputes

You may want to see also

Explore related products

![]()

Taxable Benefits: Are health insurance payouts or reimbursements considered taxable income?

Health insurance payouts and reimbursements are generally not considered taxable income for the insured individual, but exceptions exist. The Internal Revenue Service (IRS) treats these payments as tax-free when they are paid directly to the policyholder for qualified medical expenses. For instance, if your health insurance covers a $5,000 hospital bill, that amount is not reported as income on your tax return. However, this rule applies only if the premiums were paid with after-tax dollars. If your employer pays for your health insurance as part of a cafeteria plan or flexible spending arrangement (FSA), the tax treatment may differ, but the payouts themselves typically remain non-taxable.

One critical exception arises when health insurance payouts exceed actual medical expenses. For example, if you receive a $10,000 payout for a $7,000 medical expense, the $3,000 surplus may be taxable. This scenario is rare but highlights the importance of documenting expenses to avoid unexpected tax liabilities. Additionally, disability insurance payments tied to health conditions are often taxable if the premiums were paid by an employer or with pre-tax dollars. Understanding these nuances ensures compliance and prevents overpayment of taxes.

For self-employed individuals, health insurance premiums are deductible on their tax returns, but reimbursements are not taxable. This dual benefit allows them to lower their taxable income while keeping payouts tax-free. However, this only applies if the insurance plan meets IRS criteria for qualified medical expense coverage. For example, cosmetic procedures or non-prescription medications typically do not qualify, and reimbursements for such expenses could be taxable. Self-employed individuals should consult IRS Publication 502 for a detailed list of eligible expenses.

Employer-sponsored health reimbursement arrangements (HRAs) add another layer of complexity. Under an HRA, employers reimburse employees for medical expenses, and these payments are tax-free if used for qualified expenses. However, if an employee receives HRA funds but does not provide proof of eligible expenses, the funds may become taxable. For instance, if an employer reimburses $2,000 for medical expenses but the employee only submits $1,500 in receipts, the remaining $500 could be treated as taxable income. Proper documentation is key to maintaining the tax-free status of these reimbursements.

In summary, health insurance payouts and reimbursements are typically non-taxable for the insured, provided they cover qualified medical expenses and premiums were paid with after-tax dollars. Exceptions include excess payouts, disability insurance tied to pre-tax premiums, and improperly documented HRA reimbursements. By understanding these rules and maintaining thorough records, individuals can avoid unintended tax consequences and maximize the benefits of their health insurance coverage. Always consult a tax professional for personalized advice tailored to your specific situation.

Get Super Visa Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UY218_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UY218_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UY218_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UY218_.jpg)

![]()

ACA Subsidies: Are Affordable Care Act premium tax credits taxable?

Health insurance payments, particularly those involving Affordable Care Act (ACA) subsidies, often raise questions about tax implications. ACA premium tax credits, designed to make health insurance more affordable, are a lifeline for millions of Americans. However, understanding whether these subsidies are taxable requires clarity on how they function within the tax system. Unlike direct income, ACA premium tax credits are not considered taxable income to the insured. Instead, they operate as an advance payment that reduces the cost of health insurance premiums at the time of purchase. This distinction is crucial, as it ensures that individuals receiving these subsidies are not burdened with additional tax liabilities.

To grasp the tax treatment of ACA subsidies, consider how they are applied. When enrolling in a health insurance plan through the Marketplace, eligible individuals can choose to receive premium tax credits in advance, directly lowering their monthly premiums. At tax time, the actual credit amount is reconciled based on the individual’s final income for the year. If the advance payments exceed the eligible credit, the difference may need to be repaid, though repayment limits apply based on income level. Conversely, if the advance payments were less than the eligible credit, the difference is refunded or applied to the tax owed. This process ensures the subsidy remains tax-free, as it is treated as a reconciliation rather than taxable income.

A common misconception is that receiving ACA subsidies increases taxable income. This is not the case. The premium tax credits are structured to provide financial assistance without adding to the insured’s tax burden. For example, a family of four earning $60,000 annually may qualify for a subsidy that reduces their monthly premium from $1,200 to $400. The $800 difference is not reported as income; it is simply an advance payment of the tax credit. This design aligns with the ACA’s goal of making health insurance accessible without creating additional financial strain during tax season.

Practical tips for managing ACA subsidies include keeping accurate records of income and premium payments throughout the year. This helps in estimating eligibility for the correct subsidy amount and avoids potential repayment issues. Additionally, using the IRS’s tax tools or consulting a tax professional can provide clarity on how subsidies impact individual tax situations. For instance, individuals with fluctuating income should monitor their earnings and report changes to the Marketplace promptly to adjust their subsidy amounts accordingly. This proactive approach minimizes surprises during tax reconciliation.

In conclusion, ACA premium tax credits are not taxable to the insured. They function as a tax-free mechanism to reduce health insurance costs, with reconciliation occurring at tax time to ensure accuracy. Understanding this structure alleviates concerns about tax implications and allows individuals to fully utilize the benefits of ACA subsidies. By focusing on eligibility, record-keeping, and timely reporting, insured individuals can navigate the system effectively and maintain financial stability.

Granger Medical: Understanding Insurance Coverage and Your Options

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UY218_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UY218_.jpg)

![]()

HSAs & Taxes: Are contributions to Health Savings Accounts tax-deductible?

Health Savings Accounts (HSAs) offer a unique trifecta of tax advantages: contributions are tax-deductible, funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free. This makes HSAs a powerful tool for managing healthcare costs while maximizing tax savings. However, understanding the rules around HSA contributions and their tax implications is crucial to fully leverage these benefits.

To contribute to an HSA, you must be enrolled in a high-deductible health plan (HDHP) and not covered by any other health insurance, with exceptions for dental, vision, and certain preventive care policies. For 2023, the IRS defines an HDHP as a plan with a minimum deductible of $1,500 for individuals and $3,000 for families. Contribution limits are set annually; in 2023, individuals can contribute up to $3,850, while families can contribute up to $7,750. Those aged 55 or older can make an additional $1,000 catch-up contribution. These contributions are tax-deductible, reducing your taxable income for the year, regardless of whether you itemize deductions.

One of the most compelling aspects of HSAs is their flexibility. Unlike Flexible Spending Accounts (FSAs), HSAs are not "use-it-or-lose-it." Funds roll over indefinitely, allowing you to build a substantial savings pool for future medical expenses. This feature, combined with the triple tax advantage, positions HSAs as a strategic long-term investment vehicle for healthcare. For instance, if you contribute the maximum amount annually and invest the funds wisely, you could accumulate a significant nest egg for retirement healthcare costs.

However, it’s essential to navigate HSA rules carefully to avoid penalties. Withdrawals for non-qualified expenses are subject to income tax and a 20% penalty if you’re under 65. After age 65, the penalty disappears, but non-qualified withdrawals are still taxed as income. To maximize HSA benefits, focus on using the account for qualified medical expenses, such as deductibles, copays, prescriptions, and even certain over-the-counter medications. Keeping detailed records of these expenses is critical, as you can reimburse yourself from the HSA at any time, even years later.

In summary, HSA contributions are tax-deductible, offering a valuable opportunity to lower your taxable income while saving for healthcare expenses. By adhering to eligibility requirements, staying within contribution limits, and using funds for qualified expenses, you can fully capitalize on the unique tax advantages of HSAs. Whether you’re planning for immediate medical costs or building a long-term healthcare fund, HSAs provide a versatile and tax-efficient solution.

Visa Medical Insurance: What TD Visa Holders Need to Know

You may want to see also

Frequently asked questions

No, health insurance premiums paid by the insured are generally not taxable as income. They are considered a personal expense and are not included in taxable income.

No, employer-paid health insurance premiums are typically excluded from the employee’s taxable income under Section 106 of the Internal Revenue Code (in the U.S.).

It depends. If the payments are for medical expenses and the insured has not claimed a tax deduction for those expenses, the reimbursements are usually tax-free. However, if the insured claimed a deduction, the reimbursement may be taxable.

Generally, health insurance payouts for medical expenses are not taxable. However, if the payout is for non-medical reasons (e.g., a return of premiums), it may be taxable as income.

![TurboTax Desktop Business 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71UL+5xLOeL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)