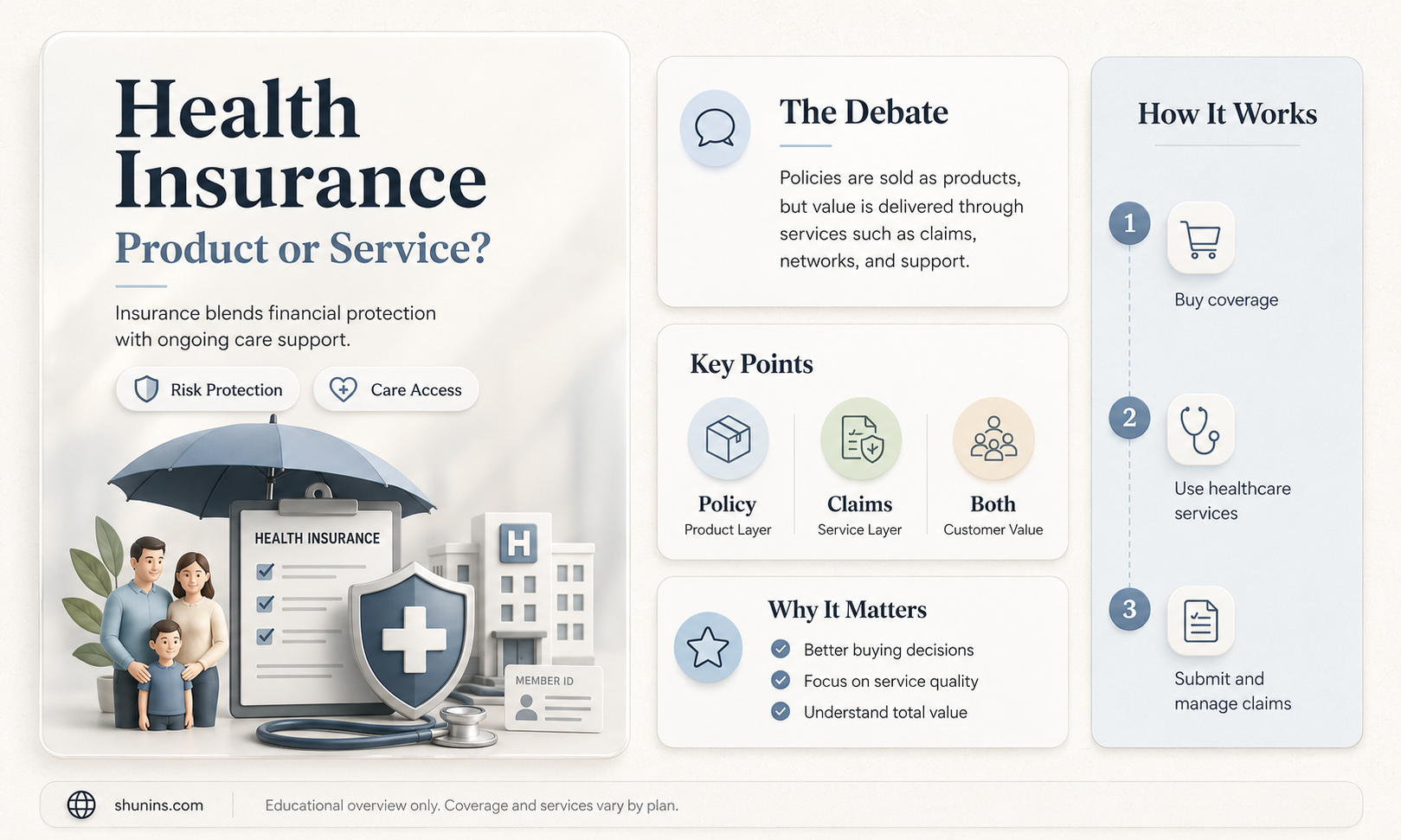

Health insurance is a critical component of modern healthcare systems, but its classification as either a product or a service often sparks debate. At its core, health insurance provides financial protection against medical expenses, which aligns with the characteristics of a service, as it involves a contractual agreement to deliver specific benefits in exchange for premiums. However, insurance policies are also tangible offerings structured with defined terms, coverage limits, and pricing, resembling a product. This duality arises because health insurance combines elements of both—it is a service in its delivery of risk management and financial support, yet it is marketed and sold as a structured product. Understanding this distinction is essential for consumers, policymakers, and industry stakeholders, as it influences regulation, consumer expectations, and the overall accessibility of healthcare coverage.

Explore related products

What You'll Learn

- Types of Health Insurance Plans (e.g., HMO, PPO, EPO, HDHP)

- Coverage and Benefits (doctor visits, hospitalization, prescription drugs, preventive care)

- Premiums, Deductibles, and Copays (cost-sharing mechanisms in health insurance policies)

- Network Providers and Restrictions (in-network vs. out-of-network healthcare services)

- Regulatory and Compliance Issues (state and federal laws governing health insurance)

![]()

Types of Health Insurance Plans (e.g., HMO, PPO, EPO, HDHP)

Health insurance plans are not one-size-fits-all; they come in various types, each with distinct features tailored to different needs and preferences. Understanding these options—HMO, PPO, EPO, and HDHP—is crucial for making an informed decision. Let’s break them down.

HMOs (Health Maintenance Organizations) prioritize cost control and coordination. With an HMO, you’re required to choose a primary care physician (PCP) who acts as your healthcare gatekeeper. All specialist visits and tests must be pre-approved by your PCP, and out-of-network care is typically not covered unless it’s an emergency. This structure keeps costs low but limits flexibility. For example, a 35-year-old professional seeking routine care might find an HMO ideal due to its affordability and emphasis on preventive services. However, someone with complex medical needs may feel restricted by the lack of direct access to specialists.

PPOs (Preferred Provider Organizations) offer greater flexibility at a higher cost. Unlike HMOs, PPOs allow you to visit any in-network provider without a referral, and you can see out-of-network providers, though at a higher out-of-pocket cost. This plan suits individuals who value choice and are willing to pay more for it. For instance, a family with children who frequently see multiple specialists might prefer a PPO for its convenience. However, premiums and deductibles tend to be higher, so it’s essential to weigh the benefits against the expenses.

EPOs (Exclusive Provider Organizations) combine HMO and PPO features but with a catch. Like PPOs, EPOs don’t require referrals to see specialists, but they limit coverage exclusively to in-network providers. There’s no out-of-network coverage, even in emergencies, except in rare cases. This plan is ideal for those who live in areas with robust in-network options and want lower premiums than a PPO. A 28-year-old urban dweller with a stable health history might find an EPO cost-effective and straightforward.

HDHPs (High Deductible Health Plans) pair with Health Savings Accounts (HSAs) for long-term savings. These plans have lower premiums but higher deductibles, often exceeding $1,400 for individuals or $2,800 for families. HDHPs are best for healthy individuals who rarely need medical care, as they pay less upfront for coverage. For example, a 40-year-old with no chronic conditions could save money by pairing an HDHP with an HSA, which allows tax-free contributions for future medical expenses. However, those with frequent healthcare needs may find the high deductible financially burdensome.

In summary, choosing the right health insurance plan depends on your healthcare needs, budget, and preference for flexibility. HMOs offer affordability with restrictions, PPOs provide freedom at a cost, EPOs balance the two but limit networks, and HDHPs cater to those prioritizing savings over immediate coverage. Assess your priorities carefully to select the plan that aligns best with your lifestyle.

Get on the Medicaid Insurance Panel: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Coverage and Benefits (doctor visits, hospitalization, prescription drugs, preventive care)

Health insurance is fundamentally a service, but its value lies in the products—coverage and benefits—it delivers to policyholders. These benefits are the tangible protections against the financial risks of medical expenses, and they vary widely across plans. Understanding the specifics of what is covered—doctor visits, hospitalization, prescription drugs, and preventive care—is crucial for maximizing the utility of any health insurance policy.

Consider doctor visits, a cornerstone of routine healthcare. Most plans cover primary care visits with a copay, typically ranging from $20 to $50, depending on the plan. For instance, a Silver-level plan under the Affordable Care Act (ACA) might require a $30 copay, while a high-deductible plan could necessitate full payment until the deductible is met. Specialist visits often incur higher copays or coinsurance, usually 20-30% of the cost. Pro tip: Always verify if your preferred doctors are in-network to avoid out-of-pocket expenses that can double or triple the cost.

Hospitalization coverage is where health insurance proves its worth, as inpatient care can cost tens of thousands of dollars. Most plans cover hospitalization after a deductible is met, with coinsurance rates typically ranging from 10-30%. For example, a three-day hospital stay averaging $30,000 could leave a policyholder responsible for $3,000 (10% coinsurance) plus the deductible. Critical care, surgeries, and emergency room visits are usually included, but pre-authorization may be required for non-emergency admissions. Caution: Some plans exclude certain high-risk procedures or experimental treatments, so read the fine print.

Prescription drug coverage is another critical benefit, often structured in tiers. Generic drugs might have a $10 copay, brand-name drugs $40, and specialty medications (e.g., biologics for chronic conditions) could require coinsurance of 25-50%. For example, a month’s supply of a specialty drug costing $5,000 could leave the patient paying $1,250. Practical advice: Use mail-order pharmacies for maintenance medications, as they often offer 90-day supplies at lower costs. Additionally, check if your plan includes a prescription drug discount program or patient assistance programs for high-cost medications.

Preventive care is the unsung hero of health insurance, designed to keep you healthy and avoid costly treatments later. Most plans cover 100% of preventive services, including annual check-ups, vaccinations (e.g., flu shots, HPV vaccines), and screenings (e.g., mammograms for women over 40, colonoscopies for adults over 50). For example, a Pap smear, which costs around $100, would be fully covered. Takeaway: Schedule preventive services early in the year to take full advantage of this benefit. Ignoring preventive care not only risks your health but also forfeits a key value proposition of your insurance.

In summary, the coverage and benefits of health insurance are its core deliverables, each tailored to address specific healthcare needs. Doctor visits and preventive care focus on accessibility and early intervention, while hospitalization and prescription drug coverage protect against catastrophic expenses. By understanding these specifics, policyholders can navigate their plans effectively, ensuring they receive the maximum benefit for their premiums.

Directors Guild of America: Medical Insurance Explained

You may want to see also

Explore related products

![]()

Premiums, Deductibles, and Copays (cost-sharing mechanisms in health insurance policies)

Health insurance policies are structured around cost-sharing mechanisms that distribute financial responsibility between the insurer and the policyholder. Premiums, deductibles, and copays are the cornerstone of this system, each serving a distinct purpose in managing healthcare expenses. Premiums are the recurring payments policyholders make to maintain coverage, while deductibles and copays are out-of-pocket costs incurred when services are used. Understanding these components is essential for maximizing the value of a health insurance plan.

Consider premiums as the price of admission to the healthcare system. They are typically paid monthly, quarterly, or annually and vary based on factors like age, location, plan type, and coverage level. For example, a 30-year-old in a low-cost-of-living area might pay $300/month for a mid-tier plan, while a 55-year-old in an urban area could pay $800/month for similar coverage. Higher premiums often correlate with lower out-of-pocket costs when services are used, making them ideal for individuals anticipating frequent medical needs. Conversely, lower premiums usually mean higher deductibles and copays, suitable for those with minimal healthcare usage.

Deductibles represent the amount policyholders must pay out of pocket before insurance coverage kicks in. For instance, a plan with a $2,000 deductible requires the insured to cover the first $2,000 of eligible medical expenses annually. Once met, the insurer begins sharing costs. Deductibles reset each year, and not all services require meeting the deductible first—preventive care, like vaccinations or annual check-ups, is often exempt. High-deductible plans (HDHPs), paired with Health Savings Accounts (HSAs), offer tax advantages but require careful budgeting to manage upfront costs.

Copays are fixed amounts paid at the time of service, such as $25 for a doctor’s visit or $50 for a specialist consultation. They are straightforward and predictable, making them easier to budget for than coinsurance, which is a percentage of the service cost. For example, a 20% coinsurance on a $1,000 MRI means paying $200 out of pocket. Copays and coinsurance often apply after the deductible is met, though some plans waive the deductible for certain services. Understanding these nuances ensures policyholders aren’t caught off guard by unexpected bills.

To optimize cost-sharing mechanisms, evaluate your healthcare usage patterns. If you rarely visit the doctor, a low-premium, high-deductible plan might suffice. However, if chronic conditions require frequent care, a higher-premium plan with lower deductibles and copays could save money long-term. Additionally, leverage preventive services, which are typically free under the Affordable Care Act, to avoid costly treatments later. Finally, review your plan’s Summary of Benefits and Coverage (SBC) annually to ensure it aligns with your health needs and financial situation. By strategically navigating premiums, deductibles, and copays, you can make health insurance a tool for financial stability rather than a source of stress.

Military Medical Insurance: Tax-funded Healthcare for Service Members

You may want to see also

Explore related products

![]()

Network Providers and Restrictions (in-network vs. out-of-network healthcare services)

Health insurance plans often divide healthcare providers into two categories: in-network and out-of-network. This distinction significantly impacts the cost and accessibility of medical services for policyholders. In-network providers have agreements with the insurance company to offer services at pre-negotiated rates, typically resulting in lower out-of-pocket costs for the insured. Out-of-network providers, on the other hand, have no such agreements, leading to higher costs and often requiring the patient to pay the difference between the provider’s charge and what the insurance covers. Understanding this difference is crucial for maximizing the value of your health insurance plan.

Consider a scenario where a policyholder needs a specialized medical procedure. If they choose an in-network provider, the insurance company will cover a larger portion of the cost, often after a copayment or coinsurance. For instance, a $5,000 procedure might require a $500 copayment, with the insurance covering the remaining $4,500. However, if the same procedure is performed by an out-of-network provider, the patient might be responsible for 50% or more of the total cost, which could exceed $2,500. This example highlights the financial advantage of staying within the network, especially for high-cost treatments.

While in-network providers offer cost savings, they may limit patient choice. Insurance companies often maintain smaller networks to control costs, which can restrict access to certain specialists or hospitals. For example, a patient with a rare condition might find that the only expert in their area is out-of-network. In such cases, patients must weigh the financial burden against the necessity of specialized care. Some plans offer out-of-network coverage but with significantly higher deductibles and coinsurance rates, making it essential to review policy details carefully.

To navigate these restrictions effectively, policyholders should take proactive steps. First, verify whether a provider is in-network before scheduling an appointment. Most insurance companies offer online directories or customer service hotlines for this purpose. Second, for out-of-network care, obtain a cost estimate and compare it with the insurance reimbursement rate to avoid unexpected bills. Finally, consider appealing to the insurance company if an in-network provider is unavailable for a specific service. Some plans allow exceptions, particularly for specialized or emergency care.

In conclusion, the in-network vs. out-of-network distinction is a critical aspect of health insurance that directly affects cost and access to care. By understanding these differences and taking proactive measures, policyholders can make informed decisions that balance financial responsibility with healthcare needs. Always review your plan’s network restrictions and coverage details to ensure you’re maximizing the benefits of your insurance while minimizing out-of-pocket expenses.

Switching Medical Insurance: Can You Change Policies Mid-Year?

You may want to see also

Explore related products

![]()

Regulatory and Compliance Issues (state and federal laws governing health insurance)

Health insurance operates within a complex web of state and federal regulations, creating a compliance landscape that demands meticulous attention from insurers, providers, and consumers alike. At the federal level, the Affordable Care Act (ACA) sets minimum standards for coverage, including essential health benefits like maternity care, mental health services, and prescription drugs. Insurers must also adhere to the ACA’s prohibitions on denying coverage based on pre-existing conditions and its requirement to allow young adults to remain on parental plans until age 26. These mandates ensure a baseline of accessibility and fairness but also impose operational constraints on insurers, such as the need to maintain detailed records for audits and reporting.

State regulations further complicate compliance by introducing variations in how federal laws are implemented. For instance, while the ACA mandates coverage for certain preventive services without cost-sharing, states may require additional services, such as fertility treatments or specific vaccinations, to be included in plans. In California, for example, insurers must cover Applied Behavior Analysis (ABA) therapy for autism spectrum disorder, a requirement not universally mandated. Conversely, some states impose stricter limits on premium increases or provider network adequacy, forcing insurers to navigate a patchwork of rules that differ significantly across jurisdictions. This state-by-state variability necessitates robust legal and compliance teams to ensure adherence to local statutes.

One of the most challenging aspects of regulatory compliance is the interplay between federal and state laws, particularly in areas like Medicaid expansion. Under the ACA, states have the option to expand Medicaid eligibility to cover individuals earning up to 138% of the federal poverty level. As of 2023, 40 states and the District of Columbia have adopted expansion, while 10 states have not, creating disparities in coverage for low-income populations. Insurers operating in non-expansion states must carefully structure their plans to avoid inadvertently enrolling ineligible individuals, while those in expansion states must coordinate with Medicaid programs to ensure seamless transitions for beneficiaries.

Practical compliance also extends to consumer protections, such as those outlined in the ACA’s Medical Loss Ratio (MLR) rule. Insurers must spend at least 80% of premiums on healthcare claims and quality improvement in the individual and small group markets, or 85% in the large group market. Failure to meet these thresholds triggers rebates to policyholders, incentivizing insurers to manage administrative costs efficiently. Additionally, states like New York require insurers to provide plain-language summaries of policies, reducing consumer confusion and minimizing disputes over coverage terms.

Despite these safeguards, regulatory compliance remains a dynamic challenge due to frequent legislative and judicial changes. For instance, the 2022 Inflation Reduction Act extended ACA premium subsidies through 2025, altering the financial landscape for insurers and consumers. Similarly, ongoing litigation over the ACA’s constitutionality introduces uncertainty, requiring insurers to remain agile in their compliance strategies. To navigate this complexity, insurers should invest in technology to monitor regulatory updates, conduct regular internal audits, and foster strong relationships with state insurance departments. By proactively addressing compliance, stakeholders can mitigate risks while ensuring access to affordable, quality healthcare.

Chipotle's Medical Insurance: What's Covered and What's Not

You may want to see also

Frequently asked questions

Health insurance is considered a service. It provides financial protection and access to healthcare services through a contractual agreement between the insurer and the policyholder.

Health insurance services focus specifically on covering medical expenses, treatments, and preventive care, whereas other insurance services (like auto or life insurance) address different risks and needs.

While health insurance is primarily a service, it can be marketed as a product in terms of policy features, coverage options, and pricing plans. However, its core function remains service-oriented.

Health insurance is categorized as a service because it involves intangible benefits, such as risk management, claims processing, and access to healthcare networks, rather than a physical or tangible item.