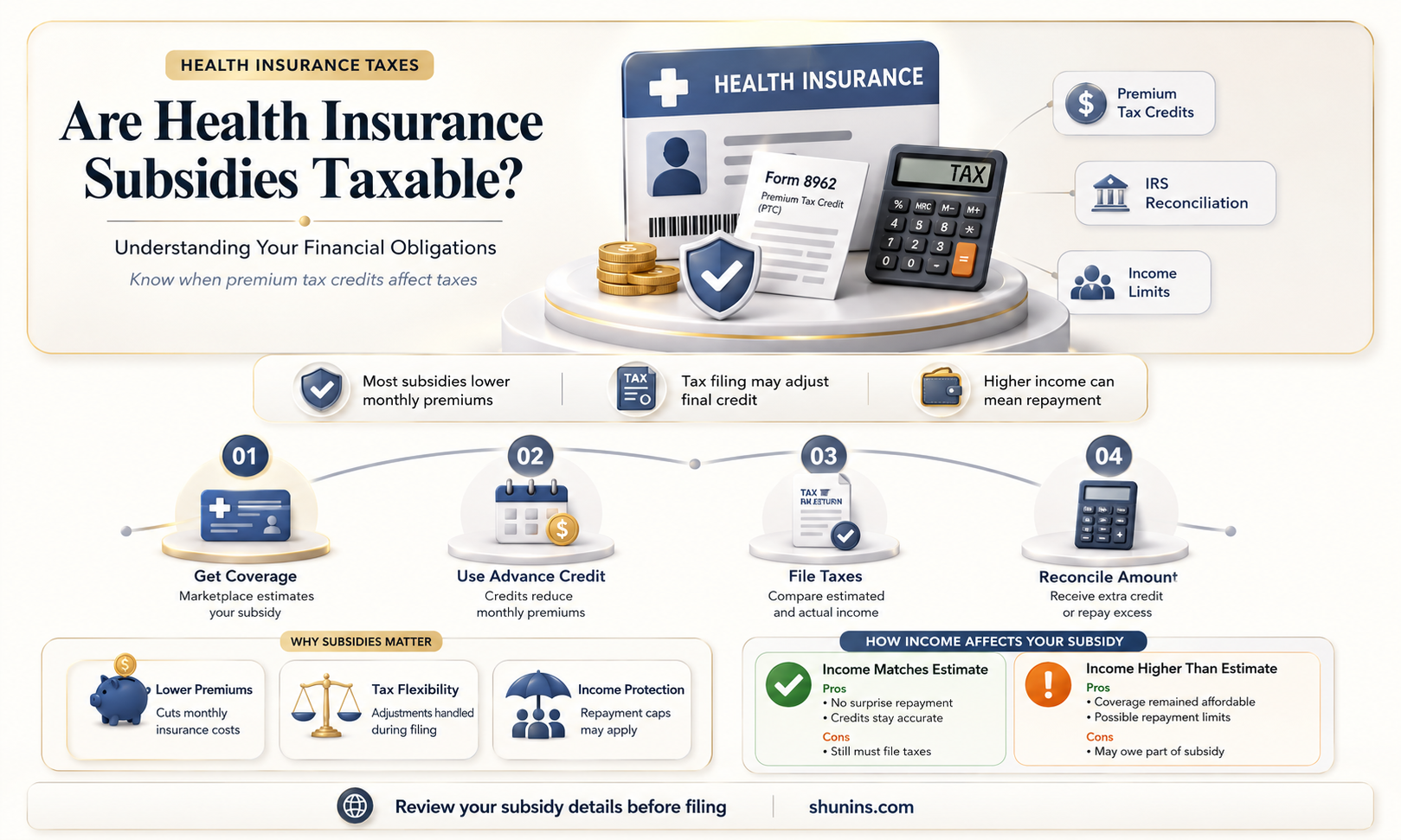

Health insurance subsidies, often provided through programs like the Affordable Care Act (ACA), are designed to make health coverage more affordable for eligible individuals and families. However, a common question arises regarding the tax implications of these subsidies: are they taxable? Generally, health insurance subsidies, such as the Advanced Premium Tax Credit (APTC), are not considered taxable income when properly reconciled on your tax return. Instead, they function as a tax credit that reduces the cost of your health insurance premiums. It’s crucial to accurately report and reconcile these subsidies during tax filing to avoid potential penalties or unexpected tax liabilities. Understanding the tax treatment of health insurance subsidies ensures compliance with IRS regulations and maximizes the financial benefits of these assistance programs.

| Characteristics | Values |

|---|---|

| Taxability of Premium Tax Credits | Advanced Premium Tax Credits (APTC) are not taxable if reconciled properly. |

| Reconciliation Requirement | Must reconcile APTC on tax returns using Form 8962. |

| Excess Subsidy Treatment | Excess subsidies received may need to be repaid, depending on income. |

| Income Threshold for Repayment | Repayment limits vary based on household income and filing status. |

| Cost-Sharing Reductions (CSRs) | CSRs are not taxable as they reduce out-of-pocket costs, not premiums. |

| ACA Compliance | Subsidies are tied to ACA-compliant plans purchased through exchanges. |

| Impact on Taxable Income | Subsidies do not increase taxable income. |

| Eligibility Criteria | Based on household income (100%-400% of Federal Poverty Level). |

| State-Specific Rules | Some states may have additional regulations; federal rules apply broadly. |

| 2023 Updates | Enhanced subsidies under the Inflation Reduction Act extended through 2025. |

Explore related products

What You'll Learn

![]()

Eligibility Criteria for Subsidies

Health insurance subsidies, particularly those offered through the Affordable Care Act (ACA), are designed to make health coverage more affordable for individuals and families with moderate incomes. However, not everyone qualifies for these subsidies, and understanding the eligibility criteria is crucial for those seeking financial assistance. The primary factor determining eligibility is income, specifically how it compares to the federal poverty level (FPL). For the 2023 plan year, individuals earning between 100% and 400% of the FPL are generally eligible for premium tax credits, though recent expansions in some states have extended this range. For example, a family of four earning between $27,750 and $111,000 annually would fall within this bracket.

Beyond income, eligibility also hinges on immigration status and access to other coverage options. Applicants must be lawfully present in the U.S. and not have access to affordable employer-sponsored insurance or government programs like Medicaid. For instance, if an employer offers a plan where the employee’s contribution is less than 9.12% of their household income, they are typically ineligible for subsidies. Additionally, individuals must enroll in a plan through the Health Insurance Marketplace to qualify. This requirement ensures that subsidies are directed toward standardized, ACA-compliant plans, which include essential health benefits like preventive care and prescription drugs.

Another critical aspect of eligibility is household size and composition. The ACA uses the Modified Adjusted Gross Income (MAGI) method to assess income, which accounts for taxable income, certain deductions, and household members. For example, a single parent with two children would have a higher income threshold for subsidy eligibility compared to an individual applicant. It’s also important to note that pregnancy and recent changes in household size can impact eligibility, so applicants should update their information promptly to avoid gaps in coverage or financial assistance.

Practical tips for navigating eligibility include using the Marketplace’s subsidy calculator to estimate potential savings and gathering necessary documentation, such as tax returns and pay stubs, before applying. Applicants should also be aware of special enrollment periods, which allow individuals to sign up outside the annual open enrollment period if they experience qualifying life events, such as job loss or marriage. By understanding these criteria and staying informed about updates to subsidy rules, individuals can maximize their chances of receiving financial assistance for health insurance.

Finland's Medical Insurance: Failing System or Future Model?

You may want to see also

Explore related products

![]()

Tax Implications of Premium Tax Credits

Premium tax credits, a form of health insurance subsidy, are designed to make health coverage more affordable for individuals and families with moderate incomes. However, their tax implications can be complex, particularly when it comes to reconciliation during tax filing. Understanding these implications is crucial to avoid unexpected tax liabilities or penalties.

The Mechanics of Premium Tax Credits

Premium tax credits are advance payments made directly to insurers to reduce monthly health insurance premiums for eligible individuals purchasing plans through the Health Insurance Marketplace. The amount of the credit is based on income, family size, and the cost of benchmark plans in the applicant’s area. For example, a family of four earning up to 400% of the federal poverty level (approximately $111,000 in 2023) may qualify. The credit is paid in advance, but its final eligibility and amount are determined when filing taxes.

Reconciliation: Where Taxes Come Into Play

At tax time, recipients must reconcile the advance payments they received with the actual credit they qualify for based on their final income. If the advance payments exceed the eligible credit, the difference may need to be repaid to the IRS. Conversely, if the advance payments were less than the eligible credit, the taxpayer receives the difference as a refund. For instance, if a taxpayer received $3,000 in advance credits but qualifies for only $2,500 based on their income, they must repay $500. However, repayment limits apply based on income, capping the amount owed for lower-income households.

Practical Tips for Managing Tax Implications

To minimize surprises, taxpayers should report income changes to the Marketplace throughout the year, as adjustments to advance credits can be made mid-year. For example, a salary increase or bonus could reduce eligibility for the credit, while a job loss might increase it. Keeping detailed records of income and premium payments is essential. Additionally, using tax software or consulting a tax professional can help navigate the reconciliation process accurately.

Long-Term Considerations

While premium tax credits are not taxable income, their reconciliation process underscores the importance of accurate income reporting and tax planning. Misestimating income can lead to financial strain if repayments are required. For those nearing the income threshold for eligibility, it may be strategic to defer income or contribute to tax-advantaged accounts to remain within qualifying limits. Understanding these nuances ensures that the subsidy serves its intended purpose—making health insurance accessible without creating undue tax burdens.

Trulicity Insurance Coverage: Which Companies Offer This Diabetes Medication?

You may want to see also

Explore related products

![]()

Reporting Subsidies on Tax Returns

Health insurance subsidies, often received through the Affordable Care Act (ACA) marketplace, can significantly reduce monthly premiums, but they come with a critical tax implication: reconciliation. When filing your tax return, you must report and reconcile these subsidies to ensure you received the correct amount based on your actual income.

Failure to do so can result in owing money to the IRS or missing out on a potential refund.

Understanding Reconciliation:

Think of subsidies as an advance payment on a tax credit. The government estimates your eligibility based on projected income. At tax time, you compare this estimate to your actual income. If your income was higher than expected, you may have received too much subsidy and need to repay some or all of it. Conversely, if your income was lower, you might qualify for a larger credit, resulting in a refund.

This process, known as reconciliation, is handled through Form 8962, Premium Tax Credit (PTC).

Gathering Necessary Information:

Before tackling Form 8962, gather these essential documents:

- Form 1095-A: This form, received from the marketplace, details the subsidies you received throughout the year.

- Income Documentation: W-2s, 1099s, and other income statements are crucial for accurately calculating your modified adjusted gross income (MAGI), which determines subsidy eligibility.

Completing Form 8962:

Form 8962 is a multi-part form that guides you through the reconciliation process. It involves calculating your MAGI, determining your eligible premium tax credit based on that income, and comparing it to the subsidies you received. The form provides clear instructions and worksheets to help you navigate the calculations.

Seeking Assistance:

While Form 8962 is designed to be user-friendly, reconciling subsidies can be complex, especially if your income situation changed significantly during the year. Consider consulting a tax professional if you have any doubts or complexities in your financial situation. They can ensure accurate reporting and potentially identify additional deductions or credits you may be eligible for.

Life and Health: Unified Life Insurance Explained

You may want to see also

Explore related products

![HUD mortgage interest subsidies tax yield (HUD-MISTY). 1988 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

Reconciliation of Advance Payments

Health insurance subsidies, often provided as advance premium tax credits (APTC), are a lifeline for millions of Americans seeking affordable coverage. However, the reconciliation of these advance payments during tax season can be a complex process, leaving many taxpayers unsure of their obligations. This process is not just a formality; it directly impacts your tax liability and potential refunds or payments due.

Understanding the Reconciliation Process

Imagine you received advance payments to subsidize your health insurance premiums throughout the year. These payments are essentially loans from the government, based on your estimated income. At tax time, you must reconcile these advances with your actual income to determine if you received the correct amount. This reconciliation is done through Form 8962, Premium Tax Credit (PTC), which is filed with your federal tax return. The form calculates the difference between the advance payments you received and the premium tax credit you're eligible for based on your final income.

Key Steps for Reconciliation:

- Gather Your Documents: Collect Form 1095-A, Health Insurance Marketplace Statement, which details your advance payments and coverage information. You'll also need your tax return information, including income and filing status.

- Complete Form 8962: This form requires you to report your household income, family size, and the premiums you paid for health insurance. It then calculates your actual premium tax credit and compares it to the advance payments received.

- Determine Your Liability: If your actual credit is less than the advance payments, you may owe the difference to the IRS. Conversely, if your actual credit is more, you may receive a refund or apply the excess to future tax liabilities.

Important Considerations:

- Income Fluctuations: Changes in income during the year can significantly impact your reconciliation. If your income increases, you may owe a portion of the advance payments back. Conversely, a decrease in income could result in a larger credit.

- Life Events: Marriage, divorce, birth of a child, or changes in employment status can affect your eligibility and the amount of your premium tax credit. Be sure to report these changes accurately on your tax return.

- Repayment Limits: The IRS has implemented repayment limits to protect taxpayers from excessive liability. These limits vary based on income level and filing status, ensuring that repayment amounts remain manageable.

Practical Tips for a Smooth Reconciliation:

- Keep Detailed Records: Maintain thorough documentation of your income, insurance premiums, and any life changes throughout the year. This will simplify the reconciliation process and ensure accuracy.

- Estimate Carefully: When estimating your income for advance payments, be as accurate as possible. Underestimating can lead to larger repayments, while overestimating may result in smaller subsidies than you're entitled to.

- Seek Professional Guidance: If you're unsure about the reconciliation process or have complex financial circumstances, consider consulting a tax professional. They can provide personalized advice and ensure your tax return is completed correctly.

In conclusion, the reconciliation of advance payments is a critical aspect of managing health insurance subsidies. By understanding the process, gathering the necessary documents, and staying informed about your financial situation, you can navigate tax season with confidence and ensure compliance with IRS regulations. Remember, accurate reconciliation not only fulfills your tax obligations but also helps you maximize your benefits and avoid potential penalties.

Medicaid Insurance Coverage: North Carolina's Form Requirements

You may want to see also

Explore related products

![]()

Impact of Income Changes on Taxability

Income fluctuations can significantly alter the taxability of health insurance subsidies, creating a complex interplay between earnings and tax obligations. For instance, individuals receiving Advanced Premium Tax Credits (APTC) through the Affordable Care Act (ACA) must reconcile these subsidies on their tax returns. If your income rises mid-year, pushing you above the eligibility threshold (400% of the federal poverty level), you may need to repay a portion of the subsidy. Conversely, a decrease in income could qualify you for additional subsidies, reducing your overall tax liability. This dynamic underscores the importance of accurate income estimation during enrollment and prompt reporting of income changes to the marketplace.

Consider a practical scenario: A single taxpayer earning $50,000 annually qualifies for a $2,000 APTC subsidy. If their income unexpectedly jumps to $60,000 mid-year, they may exceed the eligibility limit, triggering a repayment requirement. The IRS calculates the repayment based on income brackets and family size, capping the amount for lower-income households. For example, in 2023, a single filer earning between 300% and 400% of the poverty level faces a maximum repayment of $1,650. To mitigate this risk, taxpayers should use the IRS’s *Tax Credit Reduction Worksheet* to estimate potential liabilities and adjust withholding or make estimated tax payments accordingly.

From a strategic perspective, proactive income management is key to minimizing tax surprises. For self-employed individuals or those with variable income, quarterly income projections can help align subsidy usage with actual earnings. For example, if a freelancer anticipates a high-earning quarter, they might reduce their subsidy amount temporarily to avoid over-reliance on credits. Conversely, underestimating income could lead to insufficient subsidy usage, resulting in higher premiums. Tools like the ACA’s *Income and Subsidy Estimator* can aid in these calculations, ensuring a more accurate match between income and subsidy levels.

Comparatively, the tax treatment of health insurance subsidies differs from other tax credits, such as the Child Tax Credit, which phases out at higher income levels but does not require repayment. This distinction highlights the unique risk associated with health insurance subsidies: they are based on projected income, not actual earnings at the time of receipt. Unlike deductions or fixed credits, subsidies are reconciled retroactively, making them particularly sensitive to income volatility. This system incentivizes taxpayers to maintain stable income reporting but also places a greater burden on those with fluctuating earnings.

In conclusion, understanding the impact of income changes on subsidy taxability requires a blend of foresight and adaptability. Taxpayers should monitor income trends, utilize available tools for estimation, and report changes promptly to avoid penalties. For those nearing eligibility thresholds, consulting a tax professional can provide tailored strategies to navigate this complexity. By treating subsidies as dynamic rather than static benefits, individuals can optimize their tax outcomes while maintaining compliance with ACA regulations.

Medicare and Supplemental Insurance: What Providers Must Accept

You may want to see also

Frequently asked questions

Health insurance subsidies, such as those provided through the Affordable Care Act (ACA), are generally not taxable if they are properly applied to reduce your health insurance premiums. However, if you receive excess subsidies that you are not eligible for, you may need to repay some or all of that amount when you file your taxes.

Yes, you must report health insurance subsidies on your tax return. The marketplace will send you Form 1095-A, which details the subsidies you received. You’ll use this information to complete Form 8962, Premium Tax Credit, to reconcile the subsidies and determine if any adjustments are needed.

Excess health insurance subsidies are not considered taxable income, but you may be required to repay some or all of the excess amount when you file your taxes. The repayment limits depend on your income level, and there are caps on the repayment amount for individuals below certain income thresholds.

Yes, health insurance subsidies can affect your tax refund. If you received more subsidies than you were eligible for, you may owe money to the IRS, which could reduce your refund or result in a tax liability. Conversely, if you received less than you were eligible for, you may receive a larger refund.