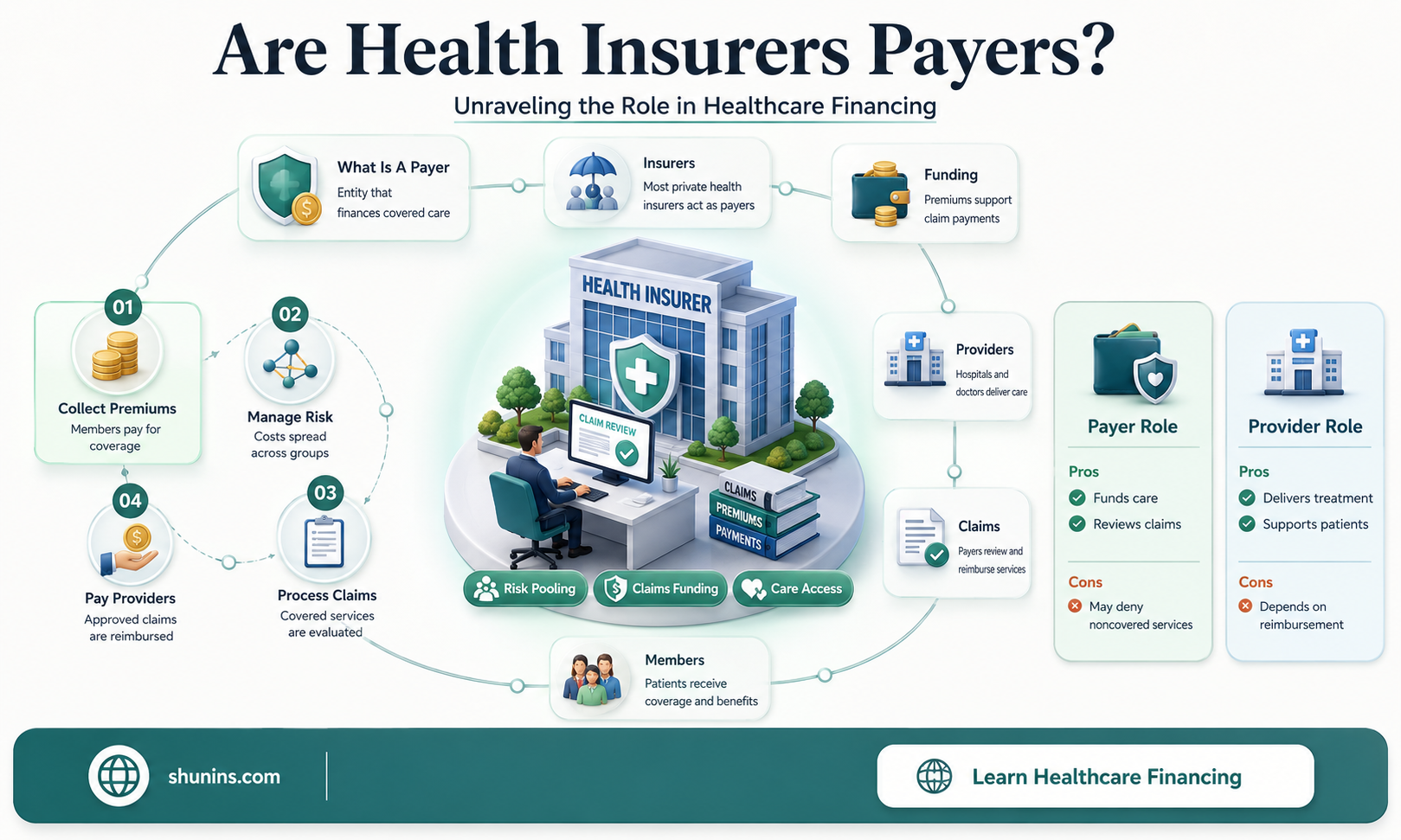

Health insurers play a critical role in the healthcare ecosystem as primary payers, acting as intermediaries between healthcare providers and patients. They manage financial risk by collecting premiums from policyholders and using those funds to cover medical expenses, ensuring that individuals and employers are not burdened with the full cost of care. By negotiating rates with providers, processing claims, and determining coverage, insurers influence both the accessibility and affordability of healthcare services. However, their dual role as both facilitators of care and cost managers often sparks debates about their impact on patient outcomes, provider reimbursements, and overall healthcare spending. Understanding whether health insurers are payers—and the implications of this role—is essential for evaluating their influence on the healthcare system and shaping policies that balance financial sustainability with equitable access to care.

Explore related products

What You'll Learn

![]()

Role of health insurers in healthcare payment systems

Health insurers are pivotal in healthcare payment systems, acting as intermediaries between patients and healthcare providers. They manage financial risk by pooling premiums from policyholders to cover medical expenses, ensuring that individuals are not burdened with catastrophic costs. For instance, in the United States, private insurers like UnitedHealth Group and Anthem process billions of claims annually, facilitating access to care for millions. Without insurers, many patients would face prohibitive out-of-pocket costs, limiting their ability to seek necessary treatments. This role extends beyond mere payment processing; insurers also negotiate rates with providers, influencing the overall cost structure of healthcare.

Analyzing the mechanics of insurer payments reveals a complex system designed to balance affordability and quality. Insurers use claims data to assess the necessity and cost-effectiveness of treatments, often employing utilization management techniques to prevent overuse or misuse of services. For example, prior authorization ensures that expensive procedures like MRI scans are medically justified before approval. While this can delay care, it also curbs unnecessary spending, keeping premiums lower for policyholders. However, this gatekeeping function has sparked debates about insurers prioritizing profits over patient care, highlighting the need for transparency and accountability in their decision-making processes.

From a comparative perspective, the role of health insurers varies significantly across countries. In single-payer systems like Canada’s, the government acts as the primary payer, eliminating the need for private insurers in basic healthcare coverage. In contrast, Germany’s multi-payer system includes both public and private insurers, offering citizens choice but also creating disparities in access and benefits. The U.S. model, heavily reliant on private insurers, often results in higher administrative costs and fragmented coverage. These differences underscore the influence of insurers on healthcare accessibility and equity, suggesting that their role is not just financial but also socio-political.

To navigate the complexities of insurer-driven payment systems, patients and providers must adopt practical strategies. Patients should scrutinize their insurance policies, understanding coverage limits, copays, and deductibles to avoid unexpected bills. Providers, on the other hand, can streamline revenue cycles by verifying patient eligibility and coding claims accurately to minimize denials. For instance, using ICD-10 codes correctly ensures that diagnoses are properly documented, reducing the likelihood of insurer rejections. Additionally, leveraging technology like electronic health records (EHRs) can improve efficiency in billing and claims processing, benefiting both parties.

In conclusion, health insurers are indispensable payers in healthcare systems, shaping how and when care is delivered and paid for. Their role demands a delicate balance between cost control and patient welfare, with implications for accessibility, quality, and equity. As healthcare evolves, insurers must adapt to emerging challenges, such as rising drug costs and the shift toward value-based care, to remain effective. By understanding their mechanisms and limitations, stakeholders can better navigate this complex landscape, ensuring that the system serves its ultimate purpose: providing affordable, high-quality care to all.

Why Insurance Companies Drop Policyholders After Filing a Claim

You may want to see also

Explore related products

![]()

How insurers negotiate provider reimbursement rates

Health insurers, as primary payers in the healthcare ecosystem, wield significant influence in negotiating provider reimbursement rates. These negotiations are pivotal in determining the financial viability of healthcare providers and the affordability of care for patients. Insurers leverage their market power, often derived from large member bases, to secure favorable rates. For instance, a major insurer might negotiate a discounted rate for a common procedure like an MRI, ensuring that their members pay less out-of-pocket while also controlling their own costs. This dynamic underscores the insurer’s role as both a payer and a cost regulator in the healthcare system.

Negotiations between insurers and providers often follow a structured process, beginning with data analysis. Insurers examine claims data, cost benchmarks, and provider performance metrics to identify areas where rates can be adjusted. For example, if a hospital’s reimbursement for a knee replacement is significantly higher than the regional average, the insurer may propose a lower rate. Providers, in turn, present their own data on operational costs, quality outcomes, and patient satisfaction to justify their rates. This back-and-forth is a delicate balance of financial sustainability for providers and cost containment for insurers.

One critical strategy insurers employ is the use of tiered provider networks. By categorizing providers into tiers based on cost and quality, insurers incentivize patients to choose lower-cost, high-quality options. For instance, a provider in the top tier might receive higher reimbursement rates due to superior patient outcomes and efficiency. Conversely, a provider in a lower tier may face reduced rates, prompting them to improve performance or risk losing patients. This tiered approach not only influences reimbursement rates but also drives competition among providers to enhance care quality.

Despite insurers’ negotiating power, providers have strategies to counterbalance these discussions. Group purchasing organizations (GPOs) and provider coalitions allow smaller practices and hospitals to negotiate collectively, increasing their leverage. Additionally, providers may highlight their unique services or specialized care to justify higher rates. For example, a cancer center with cutting-edge treatments might argue for premium reimbursement based on its ability to attract patients and improve outcomes. These countermeasures ensure that negotiations are not one-sided, fostering a more equitable dialogue.

Ultimately, the negotiation of reimbursement rates is a complex interplay of financial, operational, and quality considerations. Insurers must balance their role as payers with their responsibility to ensure access to affordable care, while providers strive to maintain financial stability without compromising patient care. As healthcare costs continue to rise, these negotiations will remain a critical mechanism for aligning the interests of insurers, providers, and patients. Practical tips for providers include investing in data analytics to demonstrate value, exploring collaborative negotiation models, and focusing on cost-effective, high-quality care to strengthen their position at the bargaining table.

Who is MSD Insurance Company? A Comprehensive Guide to Their Services

You may want to see also

Explore related products

![]()

Insurers as intermediaries between patients and providers

Health insurers often act as gatekeepers in the healthcare ecosystem, determining the flow of funds and services between patients and providers. This intermediary role is critical because it shapes access to care, influences treatment decisions, and impacts the financial sustainability of both patients and healthcare systems. For instance, insurers decide which treatments are covered, how much providers are reimbursed, and what out-of-pocket costs patients bear. This dynamic creates a complex interplay of interests, where insurers balance cost containment with patient care quality. Without this intermediary, patients might face prohibitive costs, and providers could struggle with inconsistent payment structures.

Consider the process of prior authorization, a common tool insurers use to control costs and ensure medical necessity. A 65-year-old patient with diabetes, for example, may need a specific insulin brand (e.g., Lantus, dosed at 10 units daily) that costs $300 per vial. The insurer requires the provider to submit documentation proving the patient’s need for this brand over a cheaper alternative. This step delays treatment by 3–5 days on average, potentially worsening the patient’s condition. While insurers argue this prevents overuse, providers view it as administrative burden, and patients experience frustration. This example illustrates how insurers’ intermediary role directly affects care delivery and patient outcomes.

From a provider’s perspective, insurers dictate revenue streams through reimbursement rates and claims processing. A primary care physician might spend 15–20 minutes per patient visit but receive only $80–$120 in reimbursement, depending on the insurer’s fee schedule. This disparity forces providers to see more patients daily to maintain profitability, often compromising the quality of care. Insurers also negotiate contracts with provider networks, limiting where patients can seek care. For instance, a patient with a PPO plan may pay 30% less for services within the network but face higher costs or denials outside it. This control over provider networks underscores insurers’ power as intermediaries.

Patients, meanwhile, navigate insurers’ rules through copays, deductibles, and coverage limitations. A 40-year-old with asthma requiring a monthly prescription for Symbicort (inhaler, $250 per unit) might face a $50 copay if the insurer deems it a preferred medication. If not, the cost could double. Insurers also influence preventive care by waiving copays for annual checkups or vaccinations, encouraging early intervention. However, this dual role as facilitator and barrier creates confusion and dissatisfaction. A 2022 survey found that 60% of patients felt insurers prioritized profits over their health, highlighting the tension in this intermediary relationship.

To navigate this system effectively, patients and providers must understand insurers’ incentives and processes. Patients should review their plan’s formulary and coverage details annually, especially for chronic conditions requiring specific medications or treatments. Providers can streamline prior authorization by using electronic systems and employing staff dedicated to insurance coordination. Policymakers could mandate transparency in reimbursement rates and claims denials to reduce friction. Ultimately, insurers’ role as intermediaries is indispensable but requires balance to ensure it serves, rather than hinders, the healthcare ecosystem.

Medicare Part D: Walgreens' Insurance Partners

You may want to see also

Explore related products

![]()

Impact of insurers on healthcare cost management

Health insurers, as primary payers in the healthcare ecosystem, wield significant influence over cost management through their reimbursement policies and utilization controls. By dictating which services are covered and at what rates, insurers directly shape provider behavior and patient access. For instance, the adoption of value-based care models, where insurers pay providers based on patient outcomes rather than the volume of services, incentivizes efficiency and quality. However, this approach also raises concerns about underutilization of necessary care if providers prioritize cost-cutting over comprehensive treatment. The balance between cost containment and patient welfare remains a critical challenge in insurer-driven cost management strategies.

Consider the role of prior authorization, a tool insurers use to control costs by requiring approval for certain treatments before they are administered. While this mechanism can prevent unnecessary procedures, it often delays care and burdens providers with administrative tasks. A 2021 study found that 92% of physicians reported care delays due to prior authorization, highlighting its unintended consequences. Insurers must refine such processes to minimize disruptions while maintaining fiscal responsibility. Practical tips for providers include investing in staff training for prior authorization protocols and leveraging technology to streamline submissions, reducing the administrative burden.

From a comparative perspective, the impact of insurers on cost management varies across healthcare systems. In the U.S., where private insurers dominate, cost containment efforts often focus on negotiating provider rates and limiting coverage for high-cost treatments. In contrast, single-payer systems like Canada’s prioritize global budgeting and standardized reimbursement rates, leading to more predictable costs but potential limitations in service availability. For example, while U.S. insurers may exclude certain high-cost drugs from formularies, Canadian patients face longer wait times for specialized care. Understanding these differences underscores the need for context-specific insurer strategies that align with system goals.

Persuasively, insurers’ ability to manage costs hinges on their willingness to collaborate with stakeholders. Engaging providers in designing reimbursement models can foster buy-in and improve outcomes. For instance, bundled payments for episodes of care, such as joint replacements, align insurer and provider incentives by offering a fixed payment for all services related to the procedure. This approach reduces costs by eliminating redundant services while ensuring quality care. Patients benefit from coordinated treatment, while insurers achieve savings through efficient resource allocation. Such collaborative models demonstrate the potential for insurers to drive cost management without compromising care quality.

Finally, the descriptive lens reveals how insurers’ data-driven approaches are transforming cost management. By analyzing claims data, insurers identify high-cost patient populations and implement targeted interventions, such as chronic disease management programs. For example, a diabetes management program might focus on patients aged 45–65 with HbA1c levels above 8%, offering personalized care plans and medication adherence support. This proactive approach reduces costly complications like hospitalizations. However, the success of such programs relies on robust data infrastructure and patient engagement, highlighting the need for insurers to invest in both technology and community outreach to maximize their impact on healthcare cost management.

Understanding United Health Insurance Eligibility: Who Qualifies for Coverage?

You may want to see also

Explore related products

![]()

Insurers' influence on patient access to care

Health insurers wield significant control over patient access to care through their policies on coverage, prior authorization, and provider networks. For instance, a 2022 study found that 80% of physicians reported delays in patient care due to prior authorization requirements, a process where insurers review the necessity of a treatment before approving it. This bureaucratic hurdle can postpone critical interventions, such as chemotherapy or advanced imaging, by weeks or even months. For a 65-year-old patient with stage III breast cancer, a two-week delay in starting chemotherapy could reduce the 5-year survival rate by up to 10%, according to oncology research. Insurers’ decisions, therefore, directly impact not just convenience but also clinical outcomes.

Consider the case of narrow network plans, which limit patients to a smaller group of providers to reduce costs. While these plans are often cheaper, they can restrict access to specialists or top-tier hospitals. A patient with a rare autoimmune condition like systemic sclerosis might find that their insurer’s network excludes the rheumatologist with expertise in their disease. This forces the patient to either pay out-of-pocket for out-of-network care or settle for less specialized treatment, potentially worsening their long-term prognosis. Insurers’ network design, thus, shapes not only affordability but also the quality of care patients receive.

To mitigate these barriers, patients and providers can take proactive steps. First, scrutinize insurance policies during open enrollment, focusing on coverage for pre-existing conditions, specialist access, and prior authorization requirements. For example, a diabetic patient should verify that their plan covers continuous glucose monitors and insulin pumps without excessive copays. Second, appeal denied claims aggressively. A 2021 analysis revealed that 60% of appealed claims are overturned in favor of the patient, highlighting the flaws in insurers’ initial decisions. Finally, leverage state and federal protections, such as the Affordable Care Act’s ban on lifetime coverage limits, to ensure access to necessary treatments.

Comparatively, the influence of insurers on access to care differs across countries. In the U.S., where private insurers dominate, patients often face higher out-of-pocket costs and more administrative barriers than in single-payer systems like Canada or the U.K. For example, a patient in the U.S. might pay $500 for a colonoscopy, while a Canadian patient pays nothing. However, even in single-payer systems, insurers (or government bodies) can still restrict access through budget caps or wait times. A U.K. patient might wait 12 weeks for an MRI, compared to 4 weeks in a U.S. concierge medicine practice. This underscores that while the mechanism varies, insurers universally shape patient access, often in ways that prioritize cost containment over timely care.

In conclusion, insurers’ influence on patient access to care is profound and multifaceted, impacting everything from treatment timelines to provider choice. By understanding their policies, advocating for themselves, and leveraging available protections, patients can navigate these barriers more effectively. However, systemic reforms—such as streamlining prior authorization or expanding network transparency—are ultimately needed to ensure that insurers facilitate, rather than obstruct, access to essential care.

Understanding Penalties for Being Uninsured: Health Insurance Fine Explained

You may want to see also

Frequently asked questions

Yes, health insurers are considered payers because they are responsible for reimbursing healthcare providers for services rendered to their insured members.

As payers, health insurers process claims, determine coverage eligibility, and manage payments to healthcare providers, ensuring financial transactions are completed according to policy terms.

No, while health insurers are primary payers, other entities like government programs (e.g., Medicare, Medicaid) and self-insured employers also function as payers in the healthcare system.

Health insurers influence costs by negotiating rates with providers, setting coverage policies, and implementing cost-control measures like utilization management and prior authorization.