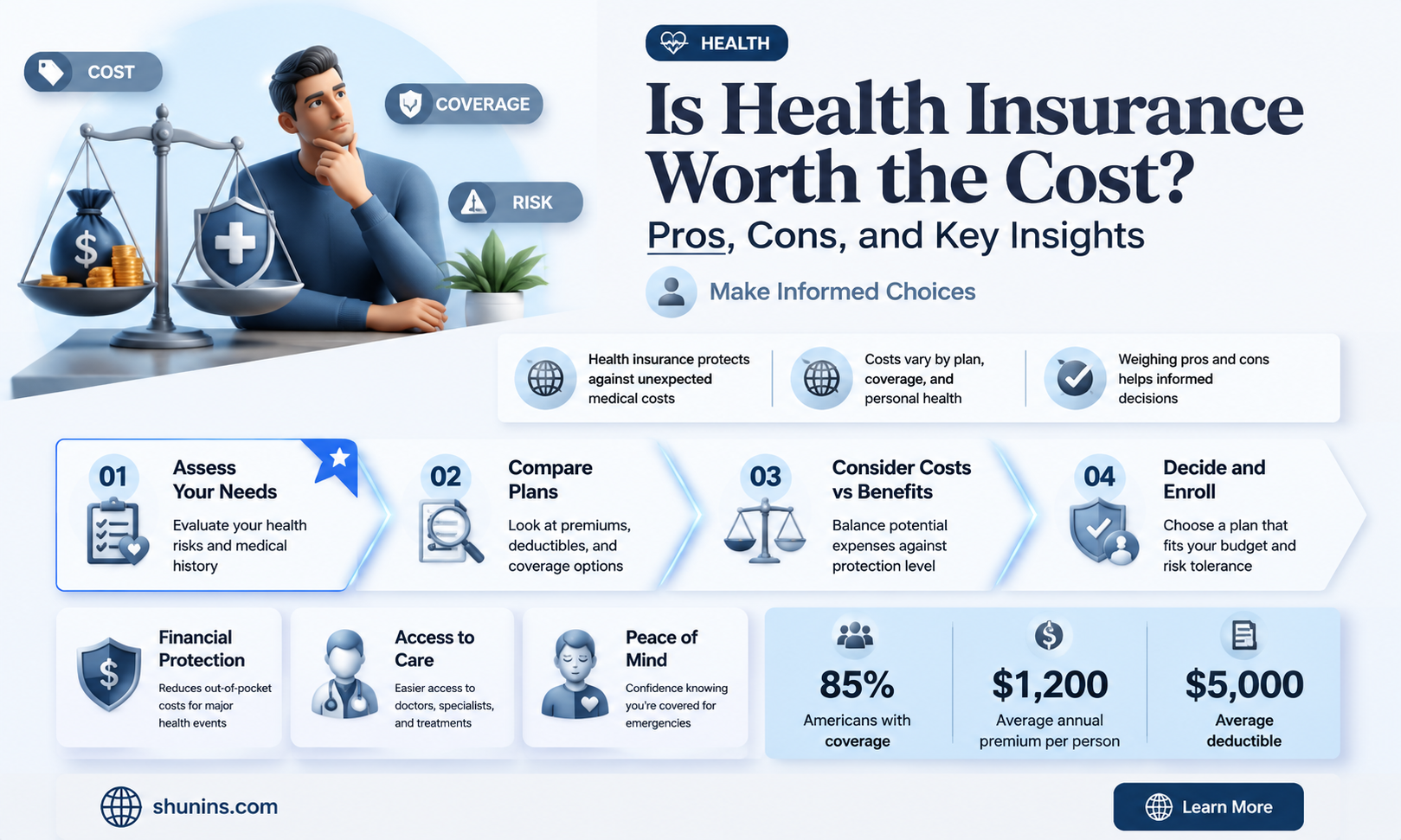

Health insurance is a critical aspect of financial planning, yet many individuals debate whether it’s truly worth the cost. On one hand, it provides a safety net against unexpected medical expenses, which can be financially devastating without coverage. On the other hand, premiums, deductibles, and copays can add up, leaving some to question the value, especially if they rarely visit the doctor. The worth of health insurance often depends on factors like age, health status, lifestyle, and the availability of employer-sponsored plans. For those with chronic conditions or families, it can be indispensable, while healthier individuals might weigh the benefits against the expense. Ultimately, the decision hinges on balancing potential risks with personal and financial circumstances.

Explore related products

What You'll Learn

![]()

Cost vs. Benefits Analysis

Health insurance premiums can consume a significant portion of your monthly budget, often leaving you wondering if the expense is justified. A cost-benefit analysis is essential to determine if the financial outlay aligns with the potential advantages. This evaluation should consider not only the immediate costs but also the long-term financial security and peace of mind that insurance provides. For instance, a 30-year-old individual might pay $300 monthly for a comprehensive plan, but this could save them from a $50,000 hospital bill in the event of an unexpected medical emergency.

To conduct a practical cost-benefit analysis, start by listing all potential medical expenses you might incur without insurance, such as doctor visits, prescriptions, and emergency care. Compare these costs to your annual insurance premium plus out-of-pocket expenses like deductibles and copays. For example, a family of four might spend $1,200 annually on routine check-ups and medications, but their insurance plan could cap their maximum out-of-pocket expense at $5,000, protecting them from catastrophic costs. Tools like healthcare calculators can help estimate these figures based on age, location, and health status.

From a persuasive standpoint, health insurance is not just about covering illnesses but also about preventive care, which can significantly reduce future costs. Many plans cover annual physicals, vaccinations, and screenings at no additional cost, enabling early detection of conditions like diabetes or hypertension. For a 45-year-old, regular screenings could identify a treatable condition early, avoiding costly treatments later. This preventive aspect shifts the focus from reactive spending to proactive investment in health, making insurance a valuable long-term asset.

Comparatively, the value of health insurance varies by age, lifestyle, and existing health conditions. A young, healthy individual might perceive insurance as less critical, opting for a high-deductible plan with lower premiums. Conversely, someone with chronic conditions like asthma or arthritis may find comprehensive coverage indispensable due to frequent medical needs. For instance, a high-deductible plan might cost $200 monthly with a $5,000 deductible, while a comprehensive plan at $400 monthly could offer lower copays and broader coverage, making it more cost-effective for those with ongoing health issues.

In conclusion, a cost-benefit analysis of health insurance requires a tailored approach, factoring in individual health needs, financial situation, and risk tolerance. Practical steps include reviewing plan details, estimating annual medical expenses, and considering the potential financial impact of unforeseen events. By weighing these elements, you can make an informed decision that balances immediate costs with long-term benefits, ensuring that your investment in health insurance is both prudent and protective.

DACA Recipients and Health Insurance: Eligibility and Coverage Explained

You may want to see also

Explore related products

![Health Insurance Benefits Advisory Council annual report on Medicare covering the period ... Volume 1966-1967 1967 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

Coverage for Unexpected Illnesses

Unexpected illnesses can strike anyone, regardless of age or lifestyle, and the financial burden they bring can be overwhelming. Health insurance steps in as a critical safeguard, offering coverage that can mean the difference between manageable expenses and crippling debt. For instance, a sudden diagnosis like appendicitis or pneumonia can lead to emergency room visits, surgeries, and hospitalizations, often costing thousands of dollars without insurance. With coverage, these expenses are significantly reduced, often limited to copays or coinsurance, making it easier to focus on recovery rather than bills.

Consider the case of a 32-year-old professional who, despite a healthy lifestyle, was diagnosed with a rare autoimmune disorder. The initial tests, specialist consultations, and ongoing medication costs totaled over $50,000 in the first year alone. Thanks to comprehensive health insurance, their out-of-pocket expenses were capped at $5,000, a fraction of the total cost. This example underscores how insurance provides a financial safety net, ensuring that unexpected illnesses don’t derail your financial stability.

When evaluating health insurance plans, pay close attention to coverage limits, exclusions, and network restrictions. Some policies may cap payouts for certain treatments or require pre-authorization for specialist visits. For instance, a plan with a $1 million lifetime maximum might seem generous but could fall short for chronic or severe conditions. Additionally, ensure the plan covers a broad range of services, including diagnostic tests, hospital stays, and prescription medications. For those with specific concerns, such as a family history of cancer, look for plans that include genetic testing or preventive screenings.

Practical tips for maximizing coverage include understanding your policy’s deductible and out-of-pocket maximum. For example, if your deductible is $2,000, plan for this expense early in the year to unlock full coverage benefits sooner. Keep detailed records of all medical expenses, as some plans allow you to apply unreimbursed costs toward your deductible. Finally, take advantage of preventive care services, often covered at 100%, to catch potential issues early and avoid more costly treatments later.

In conclusion, coverage for unexpected illnesses is a cornerstone of health insurance’s value. It transforms unpredictable, high-cost medical events into manageable expenses, providing peace of mind and financial security. By carefully selecting a plan and understanding its nuances, you can ensure that you’re protected when you need it most. Health insurance isn’t just a financial product—it’s an investment in your well-being and future stability.

Retrospective Insurance: How to Get Covered After the Fact

You may want to see also

Explore related products

![]()

Preventive Care Savings

Health insurance often frames preventive care as a cornerstone of its value proposition, and for good reason. Regular check-ups, screenings, and vaccinations can detect health issues early, when they’re cheaper and easier to treat. For instance, a colonoscopy, covered under preventive care, can identify precancerous polyps before they become colorectal cancer, a disease with an average treatment cost of $15,000 in its early stages—compared to over $100,000 in advanced stages. This isn’t just about saving money; it’s about preserving quality of life.

Consider the economics of preventive care through the lens of chronic disease management. A 45-year-old with prediabetes, if left untreated, has a 70% chance of developing type 2 diabetes within a decade. Annual preventive screenings and lifestyle interventions—covered by most insurance plans—can delay or even reverse this progression. The cost of managing prediabetes? Roughly $200–$500 annually. The cost of treating diabetes? Over $9,000 per year, on average. The math is clear: investing in prevention is fiscally smarter than reacting to crises.

Now, let’s get practical. To maximize preventive care savings, understand your insurance plan’s specifics. Most plans cover 100% of services like flu shots, mammograms (starting at age 40), and blood pressure screenings. However, some plans require in-network providers to waive copays. For example, a high-deductible health plan (HDHP) paired with a health savings account (HSA) allows you to pre-tax dollars for preventive services, effectively lowering your out-of-pocket costs. Pro tip: Schedule preventive visits during the first quarter of the year to avoid end-of-year provider backlogs and ensure timely follow-ups.

Critics argue that not all preventive services yield savings, citing overdiagnosis or unnecessary procedures. For example, annual EKGs for low-risk individuals rarely provide actionable insights but add costs. The key is to focus on evidence-based preventive measures tailored to your age, gender, and risk factors. A 30-year-old woman benefits more from HPV testing every five years than from annual Pap smears, per updated guidelines. Always consult your healthcare provider to prioritize services with the highest impact for your profile.

Ultimately, preventive care savings hinge on proactive engagement. Insurance isn’t just a safety net for catastrophic events; it’s a tool to avoid those events altogether. By leveraging covered services, you’re not just saving money—you’re investing in a future where healthcare is about maintaining wellness, not treating illness. The question isn’t whether health insurance is worth it; it’s how effectively you use it to turn prevention into your most valuable financial strategy.

Enhancing Employee Wages: Adding Medical Insurance Benefits

You may want to see also

Explore related products

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

![]()

Financial Protection from High Bills

Medical debt is the leading cause of bankruptcy in the United States, accounting for roughly 66.5% of all bankruptcies, according to a study published in the American Journal of Public Health. This staggering statistic underscores the financial vulnerability individuals face without adequate health insurance. High medical bills, often stemming from unexpected emergencies, chronic conditions, or specialized treatments, can quickly spiral into unmanageable debt. For instance, a three-day hospital stay can cost upwards of $30,000, while a complex surgery like a heart bypass can exceed $100,000. Without insurance, these expenses are borne entirely by the individual, often leading to long-term financial hardship.

Consider the case of a 45-year-old individual diagnosed with appendicitis, requiring immediate surgery. The total cost, including emergency room fees, surgery, and post-operative care, averages $35,000. With comprehensive health insurance, the out-of-pocket cost might be limited to a deductible of $1,500 and a coinsurance payment of 20% after the deductible, totaling around $8,500. Without insurance, the full $35,000 falls on the individual. This example illustrates how health insurance acts as a financial safeguard, capping potential expenses and preventing catastrophic debt.

To maximize financial protection, it’s essential to understand the components of your health insurance plan. Focus on policies with lower deductibles and out-of-pocket maximums, which limit your total liability. For instance, a plan with a $2,000 deductible and a $5,000 out-of-pocket maximum ensures you’ll never pay more than $5,000 annually for covered services. Additionally, prioritize plans with robust coverage for preventive care, as early detection of conditions like diabetes or hypertension can reduce long-term costs. For families, consider plans with pediatric dental and vision coverage, as these services are often excluded from basic policies but can add up quickly.

A common misconception is that health insurance is unnecessary for young, healthy individuals. However, accidents and sudden illnesses can occur at any age. For example, a 25-year-old involved in a car accident might require extensive rehabilitation, costing tens of thousands of dollars. Even routine procedures, like an MRI, can cost $1,000 or more without insurance. By investing in a health insurance plan with a higher deductible and lower monthly premiums, young adults can secure financial protection without breaking the bank. This approach balances affordability with coverage, ensuring peace of mind without straining monthly budgets.

Ultimately, health insurance is not just a health investment—it’s a financial one. By mitigating the risk of high medical bills, it provides a safety net that preserves savings, credit scores, and overall financial stability. For those weighing the cost of premiums against potential savings, consider this: the average monthly premium for an individual is roughly $456, or $5,472 annually, according to the Kaiser Family Foundation. Compared to the potential cost of a single medical emergency, this expense is a fraction of the financial risk it protects against. In the realm of financial planning, health insurance is a critical tool for safeguarding your economic future.

Understanding Gaps in Basic Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Long-Term Health Investment Value

Health insurance often feels like an immediate financial burden, but its true value lies in its role as a long-term health investment. Consider this: a single unexpected medical emergency can wipe out savings accumulated over years. For instance, the average cost of a three-day hospital stay in the U.S. exceeds $30,000, a sum that could derail even the most disciplined saver. Health insurance acts as a financial buffer, ensuring that such events don’t become catastrophic. By paying a predictable premium, individuals protect themselves from unpredictable, high-cost scenarios, effectively smoothing out the financial volatility of healthcare.

Analyzing the investment perspective, health insurance encourages preventive care, which is far cheaper than treating advanced conditions. Most plans cover annual check-ups, vaccinations, and screenings at no additional cost. For example, a mammogram, priced around $250 out-of-pocket, can detect breast cancer early, potentially saving tens of thousands in treatment costs later. Similarly, managing chronic conditions like diabetes through regular doctor visits and medication adherence can prevent complications like kidney failure, which requires dialysis costing upwards of $70,000 annually. Over decades, these preventive measures compound, reducing both healthcare costs and health risks.

A comparative look at insured vs. uninsured individuals highlights the long-term benefits. Studies show that uninsured adults are 25% more likely to forgo necessary care due to cost, leading to delayed treatments and poorer health outcomes. For instance, a 45-year-old without insurance might skip a colonoscopy, only to face a late-stage colon cancer diagnosis at 60, requiring extensive surgery and chemotherapy. In contrast, an insured individual would likely catch the issue early, possibly through a covered screening, resulting in less invasive treatment and better survival rates. This comparison underscores how health insurance isn’t just a safety net—it’s a tool for maintaining health and quality of life over time.

To maximize the long-term investment value of health insurance, individuals should adopt a strategic approach. First, choose a plan with comprehensive preventive care coverage, including mental health services, which are increasingly recognized as essential for overall well-being. Second, take advantage of wellness programs often offered by insurers, such as gym memberships or smoking cessation aids, which can reduce future health risks. Finally, maintain consistent coverage, even during periods of good health, to avoid gaps that could lead to higher premiums or denied coverage later. By treating health insurance as a proactive investment rather than a reactive expense, individuals can secure both financial stability and long-term health.

Understanding Coordination of Benefits: Primary Insurance First

You may want to see also

Frequently asked questions

Yes, health insurance is worth it even if you’re young and healthy. Unexpected accidents, illnesses, or preventive care needs can arise, and insurance protects you from high out-of-pocket costs.

While premiums can be costly, the financial protection against catastrophic medical expenses often outweighs the cost. Many plans also cover preventive care, saving you money in the long run.

Yes, health insurance is still valuable even if you rarely visit the doctor. It provides peace of mind and financial security in case of emergencies or sudden health issues.

High-deductible plans can still be worth it, especially if paired with a Health Savings Account (HSA). They offer lower premiums and protect you from major medical expenses.

Even if you can afford out-of-pocket costs, health insurance is worth it for protection against unforeseen, expensive medical events that could deplete your savings.