The question of whether health insurance rates are increasing due to the Affordable Care Act (ACA), commonly known as Obamacare, remains a contentious issue. Proponents argue that the ACA has expanded coverage to millions of previously uninsured Americans, implemented consumer protections like prohibiting denial of coverage for pre-existing conditions, and introduced subsidies to make insurance more affordable for low- and middle-income individuals. However, critics contend that these provisions have led to higher premiums for some, particularly those who do not qualify for subsidies or have plans outside the ACA marketplaces. Factors such as mandated essential health benefits, the elimination of skimpy plans, and the individual mandate’s penalties (before its repeal in 2019) have been cited as contributors to rising costs. While the ACA has undoubtedly reshaped the health insurance landscape, the extent to which it is directly responsible for rate increases is complex, influenced by broader trends like medical inflation, provider consolidation, and pharmaceutical costs.

Explore related products

$19.99 $14.95

What You'll Learn

![]()

Impact of ACA on premiums

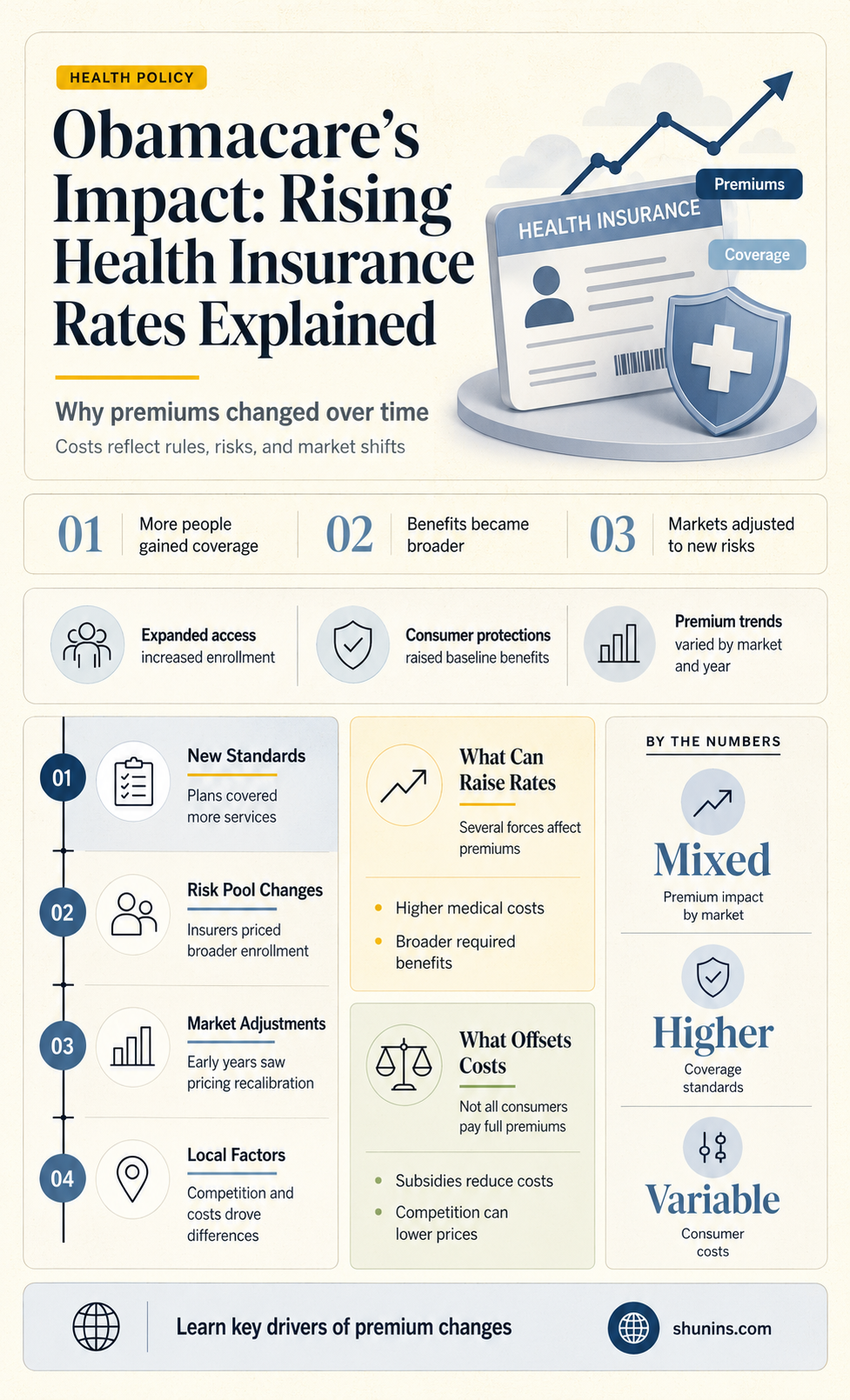

The Affordable Care Act (ACA), often referred to as Obamacare, has significantly reshaped the health insurance landscape in the United States. One of the most debated aspects of its impact is how it has influenced health insurance premiums. To understand this, it’s essential to examine both the immediate and long-term effects of the ACA on premium rates, considering factors such as expanded coverage, mandated benefits, and market dynamics.

Example and Analysis:

Before the ACA, health insurance premiums were already rising, but the law’s implementation in 2014 introduced new variables. For instance, the ACA required insurers to cover pre-existing conditions and essential health benefits, such as maternity care and mental health services. While these mandates improved access to care, they also increased costs for insurers, which were partially passed on to consumers. According to the Kaiser Family Foundation, average premiums for employer-sponsored family coverage rose from $15,745 in 2010 to $22,221 in 2021. However, it’s crucial to note that this trend predates the ACA, with annual increases averaging around 4-5% in the decade before its implementation. The ACA’s role, therefore, is not one of initiating premium increases but rather of influencing their trajectory through expanded coverage requirements and market regulations.

Steps to Contextualize Premium Changes:

- Compare Pre- and Post-ACA Trends: Analyze premium data from the decade before 2010 and after 2014 to identify shifts in growth rates.

- Account for Subsidies: Recognize that the ACA introduced premium tax credits for individuals earning up to 400% of the federal poverty level. For eligible households, these subsidies offset premium increases, making coverage more affordable despite rising rates.

- Examine Market Stability: Consider how the ACA’s risk adjustment programs and reinsurance funds aimed to stabilize premiums by compensating insurers for high-cost enrollees.

Cautions in Interpretation:

While the ACA’s mandates and regulations have contributed to premium increases, isolating its impact from broader healthcare cost trends is challenging. For example, rising prescription drug prices, hospital consolidation, and administrative costs have also driven up premiums. Additionally, the ACA’s emphasis on preventive care and chronic disease management may yield long-term savings by reducing costly emergency room visits, though these effects are harder to quantify in the short term.

Practical Takeaway:

For consumers, understanding the ACA’s impact on premiums requires a nuanced view. While rates have risen, the law’s subsidies and protections have made coverage more accessible and comprehensive for millions. To navigate this landscape, individuals should:

- Assess Eligibility for Subsidies: Use the Healthcare.gov calculator to determine potential savings.

- Compare Plans Annually: Premiums and subsidies can change each year, so reviewing options during open enrollment is crucial.

- Leverage Preventive Services: Take advantage of ACA-mandated preventive care to manage health proactively and potentially reduce long-term costs.

In summary, the ACA’s influence on premiums is multifaceted, reflecting both immediate cost increases and long-term benefits. By contextualizing these changes and utilizing available tools, consumers can make informed decisions in a post-ACA insurance market.

Off-Road Insurance: Medical Expenses Covered?

You may want to see also

Explore related products

$36.33 $54.99

![]()

Pre-existing conditions coverage costs

One of the most significant changes brought about by the Affordable Care Act (ACA), often referred to as Obamacare, is the requirement that health insurance plans cover pre-existing conditions. Before the ACA, individuals with conditions like diabetes, asthma, or cancer often faced higher premiums, exclusions, or outright denials of coverage. Now, insurers must provide these individuals with the same coverage options as everyone else, but this mandate has implications for overall insurance costs.

Consider the financial mechanics: Insuring individuals with pre-existing conditions inherently carries higher risk for insurers, as these individuals are more likely to require costly medical care. To offset this risk, insurers must spread the cost across their entire pool of policyholders, which can lead to higher premiums for everyone. Critics argue that this effectively subsidizes high-risk individuals at the expense of healthier ones, while proponents counter that it ensures access to care for those who need it most.

For example, a 45-year-old with well-managed hypertension might see their annual premium increase by $500–$1,000 due to the inclusion of pre-existing conditions coverage. While this may seem unfair to someone in good health, it’s a trade-off for the security of knowing that a future diagnosis won’t leave them uninsured. Practical tip: To mitigate costs, individuals can explore subsidies through the ACA marketplace if their income qualifies, or consider high-deductible plans paired with health savings accounts (HSAs) to balance premiums and out-of-pocket expenses.

A comparative analysis reveals that countries with universal healthcare systems, such as Canada or the UK, handle pre-existing conditions differently, often funding them through taxation rather than insurance premiums. In the U.S., the ACA’s approach represents a middle ground, blending private insurance with regulatory mandates. This hybrid model has both strengths and weaknesses: it preserves choice but can lead to cost inefficiencies and market distortions.

Ultimately, the cost of covering pre-existing conditions under the ACA is a reflection of broader societal values. It prioritizes equity and access over cost minimization, ensuring that no one is left behind due to their health status. While this may contribute to rising insurance rates, it also fosters a more inclusive healthcare system. For policymakers and consumers alike, the challenge lies in balancing affordability with the moral imperative to protect the most vulnerable.

Eye Exams: Insurance Coverage and Your Vision

You may want to see also

Explore related products

![]()

Individual mandate repeal effects

The repeal of the individual mandate, a cornerstone of the Affordable Care Act (Obamacare), has had a ripple effect on health insurance rates and market dynamics. By eliminating the penalty for not having insurance, the mandate’s repeal shifted the risk pool, as healthier individuals opted out of coverage. This behavioral change directly contributed to rising premiums for those remaining in the marketplace. Insurers, facing higher claims from a sicker population, had no choice but to increase rates to maintain profitability. For example, a 2019 Urban Institute study projected that repealing the mandate could lead to a 10% increase in premiums by 2020, a prediction that aligned with actual market trends in subsequent years.

Consider the practical implications for individuals aged 26 to 34, a demographic often deemed "young invincibles." Before the repeal, many in this age group enrolled in health plans to avoid penalties, even if they perceived themselves as low-risk. Post-repeal, enrollment among this group dropped significantly, leaving behind a risk pool with higher medical needs. If you fall into this category and are debating whether to forgo insurance, calculate the potential out-of-pocket costs for a single emergency room visit ($1,000–$2,000 on average) versus the annual premium for a bronze-level plan ($3,000–$4,000). The latter, despite seeming costly, often provides better financial protection.

From a comparative standpoint, states that expanded Medicaid under Obamacare experienced a buffer against the mandate repeal’s effects. In these states, low-income individuals had an alternative to private insurance, reducing the adverse selection in the marketplace. Conversely, non-expansion states saw sharper premium increases, as their marketplaces absorbed a higher proportion of individuals with pre-existing conditions. For instance, in Texas, a non-expansion state, premiums rose by 14.8% in 2019, compared to 5.9% in California, a state with robust Medicaid expansion. This disparity underscores the interplay between state policies and federal changes.

To mitigate the impact of rising rates, consider these actionable steps: first, explore subsidies on the Health Insurance Marketplace, as 87% of enrollees qualify for premium tax credits. Second, if you’re self-employed or work for a small business, investigate group plans, which often offer lower rates than individual plans. Third, maintain a health savings account (HSA) to offset out-of-pocket costs, especially if you opt for a high-deductible plan. Finally, stay informed about state-specific initiatives, such as reinsurance programs in states like Alaska and Minnesota, which have successfully stabilized premiums by offsetting high-cost claims.

In conclusion, the repeal of the individual mandate accelerated premium increases by altering the risk pool and insurer costs. While the effects vary by state and demographic, proactive measures—such as leveraging subsidies, exploring group plans, and utilizing HSAs—can help individuals navigate this evolving landscape. Understanding these dynamics is crucial for making informed decisions in a post-mandate insurance market.

Company Insurance vs. Alternatives: Which Option Saves You More?

You may want to see also

Explore related products

![]()

Expanded Medicaid influence on rates

The expansion of Medicaid under the Affordable Care Act (ACA), often referred to as Obamacare, has significantly reshaped the health insurance landscape. By extending eligibility to millions of low-income adults, this policy aimed to reduce the uninsured rate and improve access to care. However, its influence on health insurance rates is a complex interplay of increased demand, cost-shifting, and market dynamics. While Medicaid expansion directly impacts public insurance costs, its indirect effects on private insurance rates warrant closer examination.

Consider the mechanism of cost-shifting, a phenomenon where providers offset lower reimbursements from Medicaid by charging more to private insurers. Medicaid typically pays providers less than private insurers, creating a financial gap. To maintain revenue, hospitals and clinics may raise prices for privately insured patients, indirectly contributing to higher premiums. For instance, a 2018 study in *Health Affairs* found that private insurance premiums in expansion states increased by an estimated 1.1% due to this cost-shifting effect. While this percentage may seem modest, it translates to tangible increases for individuals and families, particularly in regions with high Medicaid enrollment.

Yet, the relationship between Medicaid expansion and insurance rates isn’t uniformly negative. By reducing the number of uninsured individuals, Medicaid expansion alleviates the burden of uncompensated care on hospitals, which historically shifted these costs to private insurers. A 2020 analysis by the Kaiser Family Foundation noted that hospitals in expansion states experienced a 39% decline in uncompensated care costs between 2013 and 2017. This reduction can mitigate upward pressure on private insurance premiums, creating a counterbalance to cost-shifting. For example, in states like Kentucky and Arkansas, hospital savings from reduced uncompensated care were linked to slower premium growth in the individual market.

To navigate this landscape, stakeholders must consider both short-term challenges and long-term benefits. Policymakers could address cost-shifting by adjusting Medicaid reimbursement rates to align more closely with private insurance payments, though this requires balancing state budgets. Employers and individuals should monitor market trends, as the impact of Medicaid expansion varies by state and insurer. For instance, in states with robust provider networks, competition may offset cost-shifting effects, while rural areas with fewer providers may see more pronounced rate increases. Practical steps include comparing plans during open enrollment, leveraging subsidies if eligible, and advocating for policies that enhance Medicaid efficiency.

In conclusion, the expanded Medicaid program under Obamacare exerts a dual influence on health insurance rates. While cost-shifting can drive premiums upward, reductions in uncompensated care offer a mitigating effect. Understanding these dynamics empowers consumers and policymakers to make informed decisions, ensuring that the goal of expanded coverage doesn’t come at the expense of affordability.

Mary Lou Retton's Health Insurance Gap: Uncovering the Surprising Reason

You may want to see also

Explore related products

![]()

Insurance market competition changes

The Affordable Care Act (ACA), often referred to as Obamacare, introduced significant changes to the health insurance landscape, including the dynamics of market competition. One of the most notable shifts was the creation of health insurance marketplaces, which aimed to increase transparency and competition among insurers. These marketplaces allowed consumers to compare plans side by side, theoretically driving insurers to offer more competitive rates and better coverage options. However, the impact on competition has been mixed, with some regions experiencing increased insurer participation and others seeing a reduction in options due to market consolidation.

Consider the case of rural areas, where the ACA’s marketplaces initially attracted multiple insurers, fostering competition. For instance, in 2014, states like Kentucky and Arkansas saw a surge in insurer participation, leading to lower premiums for consumers. However, by 2017, many insurers exited these markets due to financial losses, leaving residents with fewer choices and higher rates. This highlights a critical challenge: while the ACA intended to boost competition, the financial viability of participating in these markets has been unpredictable, leading to insurer withdrawals and reduced competition in some areas.

To understand the competitive changes, it’s essential to examine the ACA’s risk adjustment program, which redistributes funds from insurers with healthier enrollees to those with sicker populations. This mechanism was designed to encourage insurers to compete on value rather than avoiding high-risk individuals. However, smaller insurers often struggled to navigate this system, giving larger, more established companies an advantage. For example, UnitedHealth Group and Anthem have consistently outperformed smaller competitors in ACA marketplaces, leveraging their scale and expertise to manage risk more effectively. This trend underscores how the ACA’s regulatory framework has inadvertently favored larger insurers, altering the competitive landscape.

A practical takeaway for consumers is to actively monitor insurer participation in their state’s marketplace annually. Open enrollment periods are the ideal time to reassess plan options, as insurer exits or entries can significantly impact premiums and coverage. For instance, in 2023, several states, including Florida and Texas, saw new insurers enter their marketplaces, offering lower-cost plans. Consumers who switched plans saved an average of $300 annually. Tools like Healthcare.gov’s plan comparison feature can help identify the most cost-effective options, ensuring that competition works in the consumer’s favor.

Finally, policymakers must address the structural issues limiting competition in ACA marketplaces. Proposals such as expanding reinsurance programs, which protect insurers from high-cost claims, have shown promise in stabilizing markets and attracting more insurers. For example, Colorado’s state-based reinsurance program reduced premiums by 20% in 2020, encouraging new insurers to enter the market. By implementing such measures, states can foster a more competitive environment, ultimately benefiting consumers through lower rates and improved access to care.

Small Accidents: How They Affect Your Mercury Insurance Rates

You may want to see also

Frequently asked questions

While Obamacare has influenced health insurance rates, it is not the sole reason for increases. Factors like rising healthcare costs, inflation, and changes in medical technology also contribute to rate hikes.

Some premiums increased after the ACA’s implementation due to new requirements like essential health benefits and coverage for pre-existing conditions, but the law also introduced subsidies to offset costs for many individuals.

Rates have generally risen since the ACA’s passage, but this trend predates the law. The ACA aimed to slow premium growth, and while it has had mixed results, other factors like healthcare inflation play a larger role.

Covering pre-existing conditions can increase costs for insurers, which may be passed on to consumers. However, the ACA’s risk adjustment programs and subsidies help mitigate these increases.

Future rate increases depend on multiple factors, including policy changes, healthcare costs, and market stability. While the ACA remains in place, its impact on premiums will be influenced by broader economic and healthcare trends.