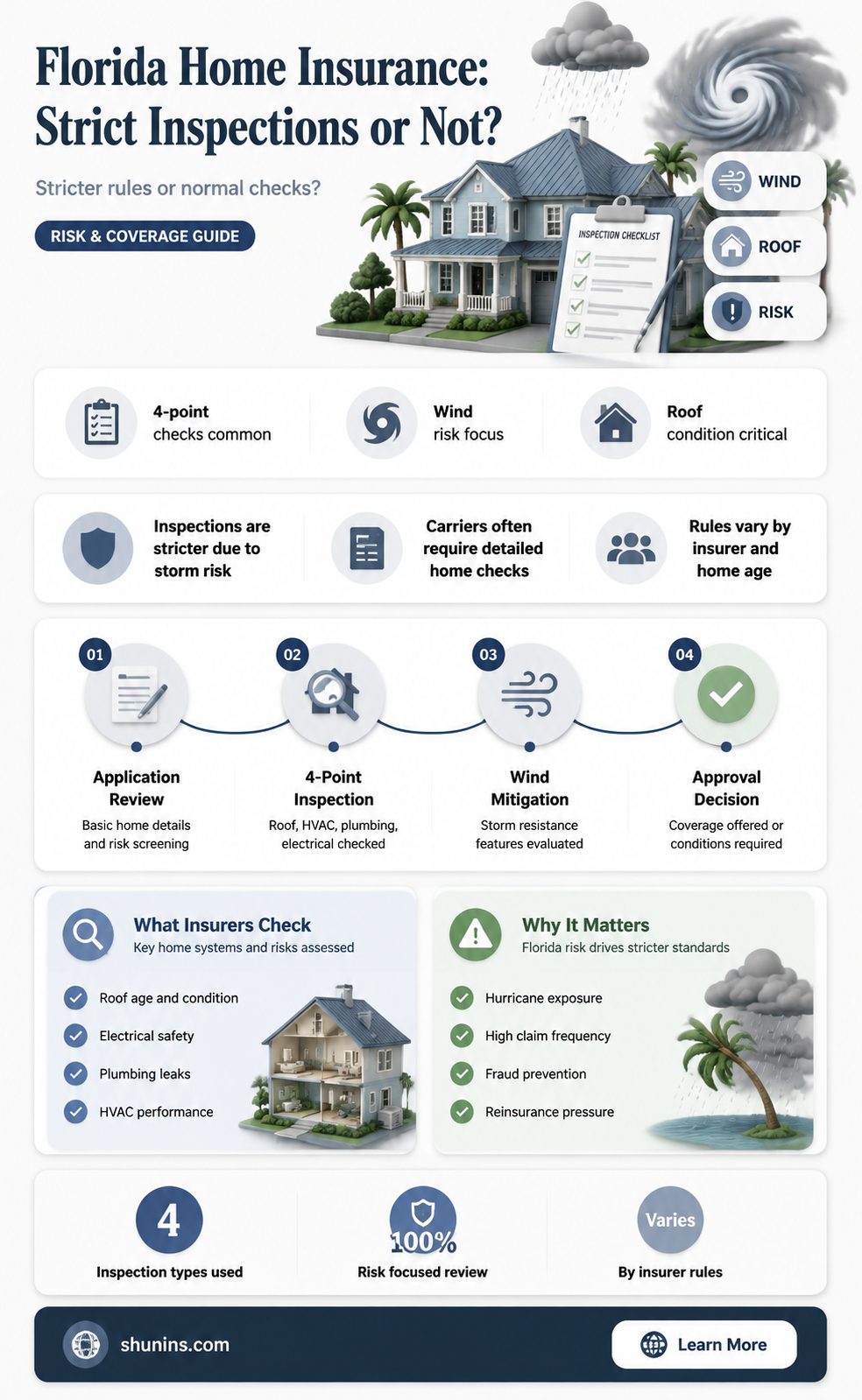

Home insurance inspections are not always necessary for procuring a home insurance policy, but they are becoming more common as part of a stricter underwriting process. In Florida, insurance inspections are required for homes over 25 years old, with some sources stating this is for homes over 30 years old. These inspections are designed to evaluate the condition of the property and the risk involved in insuring it. The four main areas of focus for inspectors are the roof, HVAC, electrical, and plumbing systems. The interior and exterior of the home are inspected, and the results can affect your rate or policy standing.

| Characteristics | Values |

|---|---|

| Inspection requirement | An insurance inspection is necessary for homes over 25 years old. Some sources state that this requirement is for homes over 30 years old. |

| Inspection type | A four-point inspection is a visual inspection of a property required for purchasing a homeowners insurance policy. |

| Inspection components | The four main components that are examined during a four-point inspection are the roof, HVAC, electrical, and plumbing systems. |

| Inspection frequency | Home insurance inspections are typically completed on a case-by-case basis and may not be required for newer homes. |

| Inspection process | The inspector will examine the property for any repairs, damages, and deficiencies, recording the information on an official inspection form. |

| Inspection notice | The insurance inspector may or may not provide notice before arriving. If the home is in a gated community or is considered high-value, the inspector will give notice. |

| Inspection results | The results of the inspection can be used to determine the insurance premium and may affect the rate or policy standing. |

| Inspection failure | If the inspection fails, it is possible to apply for another home insurance policy with a different insurer. |

Explore related products

What You'll Learn

![]()

Florida homes over 25-30 years old require an inspection

In Florida, homes over 25-30 years old are required to undergo a four-point insurance inspection to obtain a homeowners insurance policy. This inspection is necessary for the insurer to assess the risks associated with providing coverage for older homes. While it is not a strict rule, most insurance companies prefer to conduct these inspections to determine the appropriate coverage and premium rates.

The four-point inspection focuses on the roof, HVAC, electrical, and plumbing systems of the property. These areas are critical in evaluating the condition of the home and identifying potential risks. For instance, outdated electrical wiring or defective roofs can increase the likelihood of insurance claims. By conducting this inspection, insurers can gauge the necessary level of coverage to offer.

The inspection process can vary in scope. In some cases, a qualified inspector may simply drive by the property and perform a visual assessment of the exterior. In other instances, a more comprehensive in-person inspection may be required, particularly for high-value homes. During this inspection, the inspector will examine the interior and exterior of the home, including the basement, attic, roof, gutters, doors, and windows.

Homeowners should be aware that failing to cooperate with the inspection process could result in their insurance policy being cancelled or not renewed. Therefore, it is advisable to prepare for the inspection by checking for any issues in the areas mentioned above and making necessary repairs or replacements. By addressing these concerns promptly, homeowners can increase the likelihood of obtaining favourable insurance coverage and rates.

It is worth noting that Florida's inspection requirements extend beyond insurance purposes. Following the collapse of the Champlain Towers in Surfside, Florida, in 2021, the state introduced legislative changes to enhance safety standards for older buildings. As a result, Florida implemented milestone inspection requirements for buildings over 25 and 30 years old to ensure structural stability and foster a culture of safety and responsibility. These inspections are separate from insurance inspections and are mandatory for certain building types, with specific exemptions for single-family homes, small structures, and government-owned buildings.

Sixt Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Four-point inspections are common

Home insurance inspections are not always necessary for procuring a home insurance policy, but they are becoming more common as part of a stricter underwriting process. Four-point inspections are common and are often considered a universal language between insurance companies, the agent, and the homeowner. This type of inspection is a visual inspection of a property required for purchasing a homeowners insurance policy. It is typically required for homes over 25 or 30 years old and allows insurers to determine the level of risk they are taking on by offering an insurance policy. The four main components that are examined during a four-point inspection are the roof, HVAC, electrical, and plumbing.

The roof is an extremely important part of the inspection and the property itself. The inspector will check the condition of roofing shingles, warping, wear and tear, missing shingles, and potential water pooling or leaks. The interior portion of the inspection can help insurers identify significant risks within the home, such as pest infestations, that would not be covered by standard homeowners insurance. The inspector will also concentrate on the electrical, plumbing, and HVAC systems if an interior inspection is necessary. They may also check safety features such as smoke alarms, fire extinguishers, and anti-theft devices.

The inspection is straightforward, with a pass or fail result, and is minimally invasive as it only looks at these four main visible systems. Many insurance companies focus the four-point inspection's attention on older homes, as well as homes located in high-risk flood or evacuation zones, which applies to many Florida properties. A four-point inspection may also uncover any safety issues related to the property, but it is not categorized as a safety inspection.

The average cost of a four-point inspection from a certified professional inspector can range from $50 to $100. Inspectors can also provide a wind mitigation inspection with their four-point inspection and offer a bundled or discounted rate. It is beneficial to check the property for any potential hazards or damage prior to an inspection and fix any visible wear and tear or problem areas.

Amica Insurance: Worth the Money or Not?

You may want to see also

Explore related products

![]()

Inspections are not always necessary for insurance

Home insurance inspections are not always necessary and are done at the insurer's discretion. However, certain situations may make an insurance inspection necessary. For example, if you've made significant remodellings to your home and are having it appraised for a second time, you may need another home insurance inspection.

Insurance companies may request an inspection to help them determine the amount of coverage needed, especially for older homes or homes that haven't been inspected in a while. An insurance inspection allows the insurance company to gauge potential risks, such as outdated electrical wiring or defective roofs.

In Florida, a four-point insurance inspection is a visual inspection of a property required for purchasing a homeowners insurance policy for homes over 25 years old. It allows insurers to determine the risk involved in offering an insurance policy. While the four-point inspection is not comprehensive enough to evaluate all the risks of purchasing a home, it is a straightforward pass or fail inspection that focuses on four main areas: the roof, HVAC, electrical, and plumbing systems.

The interior and exterior of the home can be inspected, and the results can affect your rate or policy standing. An insurance inspection could be as simple as a qualified inspector driving by your home and checking your property's exterior, or it could be an in-person visit to your home.

Canceling Mortgage Payment Protection Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Inspections can affect insurance rates

In Florida, insurance companies may require a four-point inspection for homes over 25 or 30 years old. This inspection focuses on the roof, HVAC, electrical, and plumbing systems. The inspector will look for any repairs, damages, and deficiencies and record this information on an official inspection form. The results of the inspection can affect your insurance rates or policy standing. For example, if the inspector notes that your plumbing system is old but in perfect condition, the insurer will factor this into the rate they offer. On the other hand, if there is a leak in your basement, the insurer may not issue a policy until you make the necessary repairs.

Inspections can also affect insurance rates by helping insurers identify significant risks within the home that would not be covered by standard homeowners insurance. For example, pest infestations or outdated electrical wiring. If there are any signs of a threat to the property, such as a low-hanging branch above the roof or a crack in the driveway, insurers may require you to fix these issues before providing coverage.

The interior portion of the inspection can help insurers identify risks that may not be apparent from an exterior inspection or photos/videos. For example, water damage or indications of insects or rodents in the attic. Inspectors may also check safety features such as smoke alarms, fire extinguishers, and anti-theft devices.

In some cases, inspections may be required for homes in high-risk areas, such as those prone to hurricanes, tornadoes, or wildfires. Homes in these areas may have higher insurance rates due to the increased risk of damage. Additionally, homes with wind-damage mitigation features may qualify for policy premium discounts by documenting these features through a wind mitigation inspection.

It's important to note that not all insurance companies require a home inspection, and some may accept an appraisal in place of a formal inspection. However, an inspection can benefit the homeowner by proving their diligence and responsibility, reassuring the insurance company that their home is worth covering.

Septic Drain Field: Is Homeowners Insurance Enough?

You may want to see also

Explore related products

![]()

Inspectors may or may not provide notice before arriving

In Florida, insurance companies may or may not require a home inspection to obtain a homeowners insurance policy. However, more companies have started requiring one as part of their stricter underwriting process. The inspection helps insurance companies assess the replacement cost and risks associated with a new homeowners insurance policy or the renewal of an existing policy. It is a way for the insurance company to gauge potential risks, such as outdated electrical wiring or defective roofs.

Homeowners insurance inspections in Florida are not always necessary, but they can be beneficial to both the homeowner and the insurance company. For example, an inspection may prove how diligent and responsible the homeowner is, reassuring the insurance company that the home is worth covering. On the other hand, the results of the inspection can be used to determine the insurance premium, as they help the insurance company understand the level of risk they are taking on.

The interior and exterior of the home can be inspected, and the results can affect the policy rate or standing. An inspector may or may not provide notice before arriving. If the home is in a gated community or is considered high value, which often requires an interior inspection, the inspector will give notice so that the homeowner can let them in. If the homeowner does not cooperate with the process, the insurance company may cancel or choose not to renew the policy.

Home insurance inspections in Florida differ from a full home inspection that typically occurs when buying a home. A full inspection allows potential homebuyers to evaluate the property from top to bottom for safety and structural issues before deciding to purchase the home. Home insurance inspections may not be as extensive and are completed on a case-by-case basis. They are often required for homes over 25 or 30 years old and can be combined with wind mitigation inspections.

Farmers' Malpractice Insurance: Overcoming the Challenges of Agricultural Risks

You may want to see also

Frequently asked questions

Home insurance inspections are not always necessary for obtaining a home insurance policy. However, many insurance companies have started requiring them as part of their underwriting process. In Florida, a four-point insurance inspection is required for homes over 25 or 30 years old. This type of inspection is a visual evaluation of the property's roof, HVAC, electrical, and plumbing systems.

If your home fails the insurance inspection, your insurance company may cancel your policy or choose not to renew it. You can apply for another home insurance policy, but any new insurer will likely want to conduct their own inspection. It is recommended to address any issues from the previous inspection to avoid the same problems from arising again.

Before a homeowners insurance inspection, you should check for any potential hazards or damage and make necessary repairs. This includes looking for cracks in the foundation, signs of mould or water damage, and ensuring the roof is in good condition. It is also important to provide clear access to the electrical panel, water heater, and AC unit for the inspector.