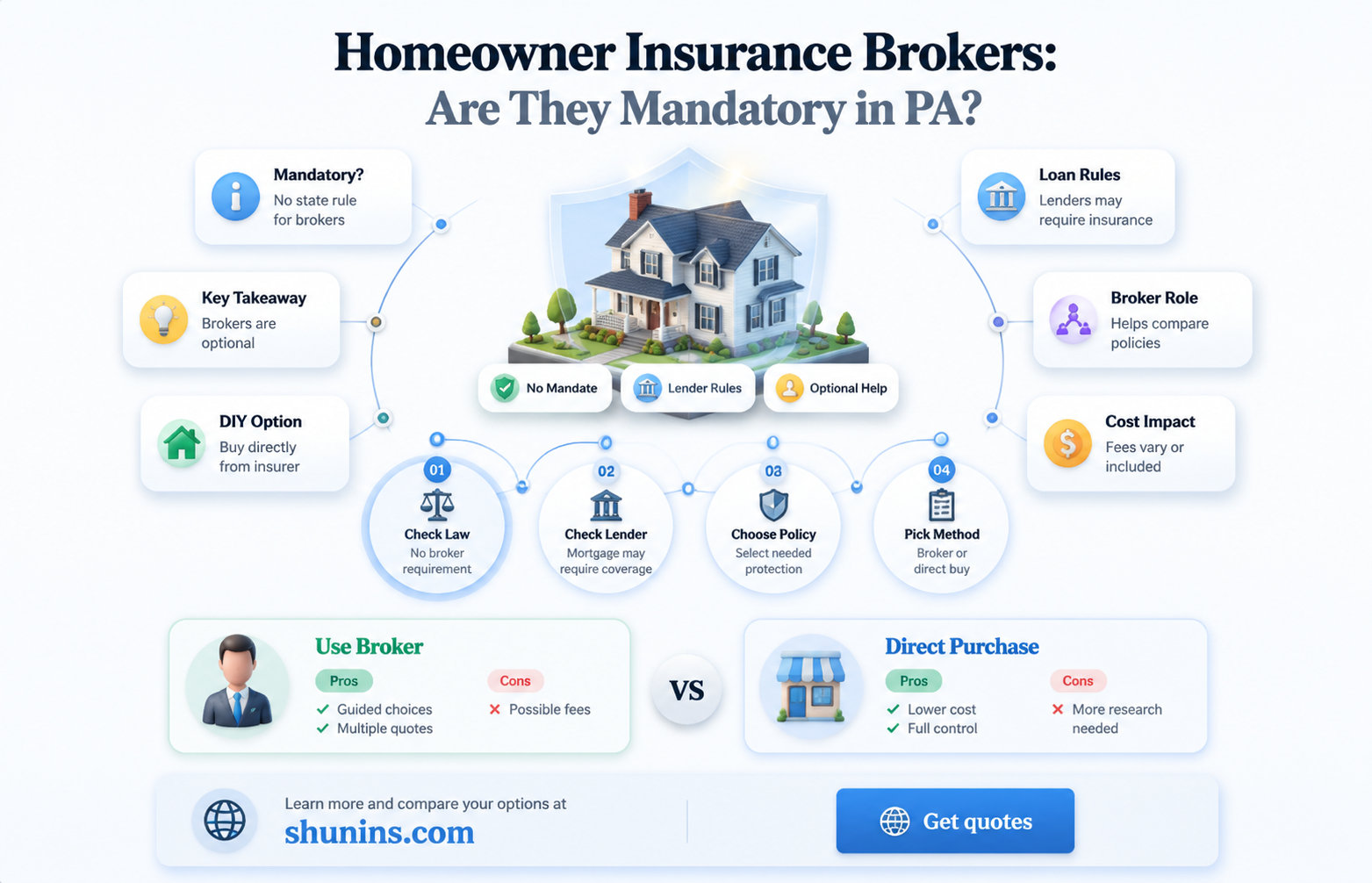

Homeowners in Pennsylvania are not required by law to have home insurance, but most banks or lenders will require coverage for at least the amount of the mortgage. Similarly, while Pennsylvania does not require real estate brokers to have E&O insurance, it is strongly recommended to protect against legal costs related to accusations of negligence, and real estate agencies, brokerages, and client contracts will likely require this coverage.

| Characteristics | Values |

|---|---|

| Homeowners insurance mandatory in Pennsylvania | No |

| Real estate business insurance mandatory in Pennsylvania | Yes |

| E&O insurance mandatory for real estate agents and brokers in Pennsylvania | No, but strongly recommended and required by agencies, brokerages, and client contracts |

| Average insurance premium for E&O insurance in Pennsylvania | $47 per month |

| Average insurance premium for general liability insurance in Pennsylvania | $32 per month |

| Average insurance premium for workers' comp insurance in Pennsylvania | $59 per month |

Explore related products

What You'll Learn

![]()

Homeowners insurance isn't mandatory in Pennsylvania

Homeowners insurance is not mandatory in Pennsylvania, but it is highly recommended. Without insurance, you are responsible for repairs or replacements if your home is damaged or destroyed. Most banks and lenders will require you to have insurance to cover your home for at least the amount of the mortgage.

Homeowners insurance provides financial protection for your home, personal belongings, and other structures on your property. It also covers personal liability, such as injuries to guests on your property. You can also add coverage for valuable items like jewellery and protection against credit card fraud or identity theft.

When considering homeowners insurance in Pennsylvania, it's important to understand the exclusions and limitations. For example, flood and earthquake damage are typically excluded from standard policies. Additionally, there may be limits on the amount of coverage provided for certain high-value items.

It's also worth noting that Pennsylvania has specific laws governing homeowners insurance. Insurance companies cannot cancel your policy solely based on your claims history or loss history. However, they may request improvements to address recurring issues. If you don't comply with these requests, your policy could be canceled. Late payments can also lead to policy cancellation, and there is no legal requirement for insurance companies to provide a grace period.

When shopping for homeowners insurance in Pennsylvania, it's essential to compare coverage and prices from multiple providers to find the best fit for your needs. While insurance is not mandatory, it provides valuable financial protection for your home and belongings.

Reporting Insurance Settlements: 1040 Form and You

You may want to see also

Explore related products

![]()

Most banks require insurance for at least the mortgage amount

Homeowners insurance is not mandatory in Pennsylvania, but most banks or lenders will require you to cover your home for at least the amount of the mortgage. This is because the bank has a financial interest in your property. With a homeowners insurance policy in place, your lender is assured of a payout in the event of a covered peril. The amount of insurance you need will depend on factors such as how much you paid as a down payment, the amount of your loan, and whether your home's location calls for additional coverage. For example, if you live in an area prone to hurricanes, windstorms, or other natural disasters, your lender may require you to have windstorm coverage or purchase flood insurance.

Mortgage lenders typically require homeowners insurance to protect their financial investment in your home. In the event of a loss or damage to the property, homeowners insurance provides financial protection for both the homeowner and the lender. This type of insurance covers damage to the home and attached structures, such as garages, as well as detached structures like sheds and fences. It also reimburses you for damage to or theft of your personal property, including furniture, appliances, and electronics.

While homeowners insurance is not legally required in most states, including Pennsylvania, it is highly recommended by financial experts. This is because it offers financial protection in the event of damage to your home or belongings. Additionally, it can provide liability coverage if someone is injured on your property. When purchasing homeowners insurance, it is important to shop around and compare coverage and prices to find the best policy for your needs.

It is worth noting that mortgage insurance, which is different from homeowners insurance, may be required in certain situations. Mortgage insurance protects the lender in the event that the borrower falls behind on their payments. It is typically required for borrowers who make a down payment of less than 20% of the purchase price of the home and is included in the borrower's monthly payments. Private mortgage insurance (PMI) rates vary by down payment amount and credit score and are generally paid monthly.

Earthquake Insurance: Is CEA Coverage Worth the Cost?

You may want to see also

Explore related products

![]()

Home insurance covers damage to the house and personal property

Homeowners insurance is not mandatory in Pennsylvania, but it is a good idea to have it as it protects you financially from damages and losses to your home and personal property. Most banks or lenders will require you to insure your home for at least the amount of the mortgage. Home insurance covers a broad range of possible damages, including damage to the physical dwelling and other structures on the property, such as a garage, fence, driveway, or shed. It also covers damage to or theft of personal property, including furniture, appliances, electronics, and clothing. However, coverage may be limited for certain high-value items, such as jewelry or artwork, and additional coverage may be needed.

It's important to understand what is and isn't covered by your homeowner's insurance policy. Most policies cover damage caused by specific perils such as hurricanes, frozen pipes, theft, vandalism, and fire. Home insurance may also provide liability protection if someone is injured on your property or if you are responsible for damaging someone else's property. It can also help cover additional living expenses if you need to move temporarily while your house is being repaired due to covered damage.

While home insurance provides financial protection for your home and personal belongings, it's important to note that not all types of damage or loss are covered. Common exclusions include damage caused by flooding and earthquakes. Additionally, if you run a business on your property in a separate structure, homeowners insurance typically does not cover it. It's always a good idea to review your policy carefully and discuss any questions or concerns with your insurance agent to ensure you have the coverage you need.

In the event of a disaster or if you need to file a homeowner's insurance claim, having an accurate home inventory is crucial. This allows your insurance carrier to have the necessary information to help settle your claims. There are tools available, such as the NAIC app, that can assist in creating a comprehensive record of your belongings, making it easier to navigate the claims process during stressful times.

Single Limit Earthquake Insurance: Worth the Cost?

You may want to see also

Explore related products

$47.22 $84.99

![]()

It also covers lawsuits and injuries on the property

In Pennsylvania, homeowners' insurance is not mandatory. However, most banks or lenders will require you to insure your home for at least the amount of the mortgage. Homeowners' insurance protects your home and your personal property, and may also protect you against lawsuits and injuries on the property.

Homeowners' insurance policies typically include personal liability coverage, which may cover lawsuits brought against you by third parties for bodily injury or property damage, up to the limits of your policy. For example, if a guest slips and falls on an icy walkway on your property and decides to sue, your personal liability coverage may pay for the damages and provide you with a legal defence, depending on your policy's limits.

Medical payments coverage is another feature of homeowners' insurance that can pay small injury claims resulting from accidents on your property, regardless of who is at fault. This coverage usually ranges from $1,000 to $5,000 and can help cover an injured guest's medical expenses.

It is important to note that homeowners' insurance policies typically exclude intentional acts and criminal acts. For example, if you deliberately push someone down the stairs in your home, your insurance will likely not cover their medical bills or any legal costs if they decide to sue. Similarly, if you assault someone, your policy's criminal acts exclusion may apply, and you may not be covered.

Additionally, bodily injury or property damage in connection with running a business out of your home is typically excluded from homeowners' insurance coverage. For instance, if you operate a baking business from your home and accidentally give a client food poisoning, your homeowners' insurance may not cover any medical or legal costs if they decide to sue.

Homeowners' insurance policies may also have exclusions for certain dog breeds or types of pets. For example, some insurers may not cover dog bites or exclude specific breeds from coverage. Therefore, it is essential to carefully review your policy to understand all coverage exclusions.

Vacant Lot Conundrum: Exploring Insurance Options with Farmers for Unused Land

You may want to see also

Explore related products

![]()

Exclusions include floods and earthquakes

Homeowners insurance is not mandatory in Pennsylvania. However, most banks or lenders require you to insure your home for at least the amount of the mortgage. This insurance protects your home and your personal property, and may also protect you against lawsuits if someone gets hurt on your property.

While homeowners insurance is not mandatory, flood insurance is required for homes and businesses in high-risk flood areas with mortgages from government-backed lenders. Flood insurance can be purchased through licensed property and casualty insurance agents in Pennsylvania to cover almost any building and its contents, including rental property and condominiums. Tenants can also buy protection for their belongings.

Standard homeowners insurance does not cover flood damage. This includes the National Flood Insurance Program (NFIP) and private insurers. The NFIP is administered by the Federal Emergency Management Agency (FEMA), which provides educational resources to help consumers understand the basics of flood insurance, how to protect their homes, and what to do if they are victims of a flood.

In addition to floods, earthquake coverage is also excluded from standard homeowners insurance policies. Earthquake coverage is available from most insurance companies as a separate policy or an endorsement to your homeowners insurance.

Home Insurance: Is It a Legal Requirement?

You may want to see also

Frequently asked questions

No, homeowners insurance is not mandatory in Pennsylvania. However, most banks or lenders will require you to insure your home for at least the amount of the mortgage.

No, Pennsylvania does not require insurance brokers to have E&O insurance. However, it is strongly recommended as it protects against legal costs related to accusations of negligence.

Homeowners insurance in Pennsylvania typically covers damage to your house and any attached structures, such as garages. It also covers damage to detached structures like sheds and fences. Additionally, it reimburses you for damage to or theft of your personal property, including furniture, appliances, and electronics.