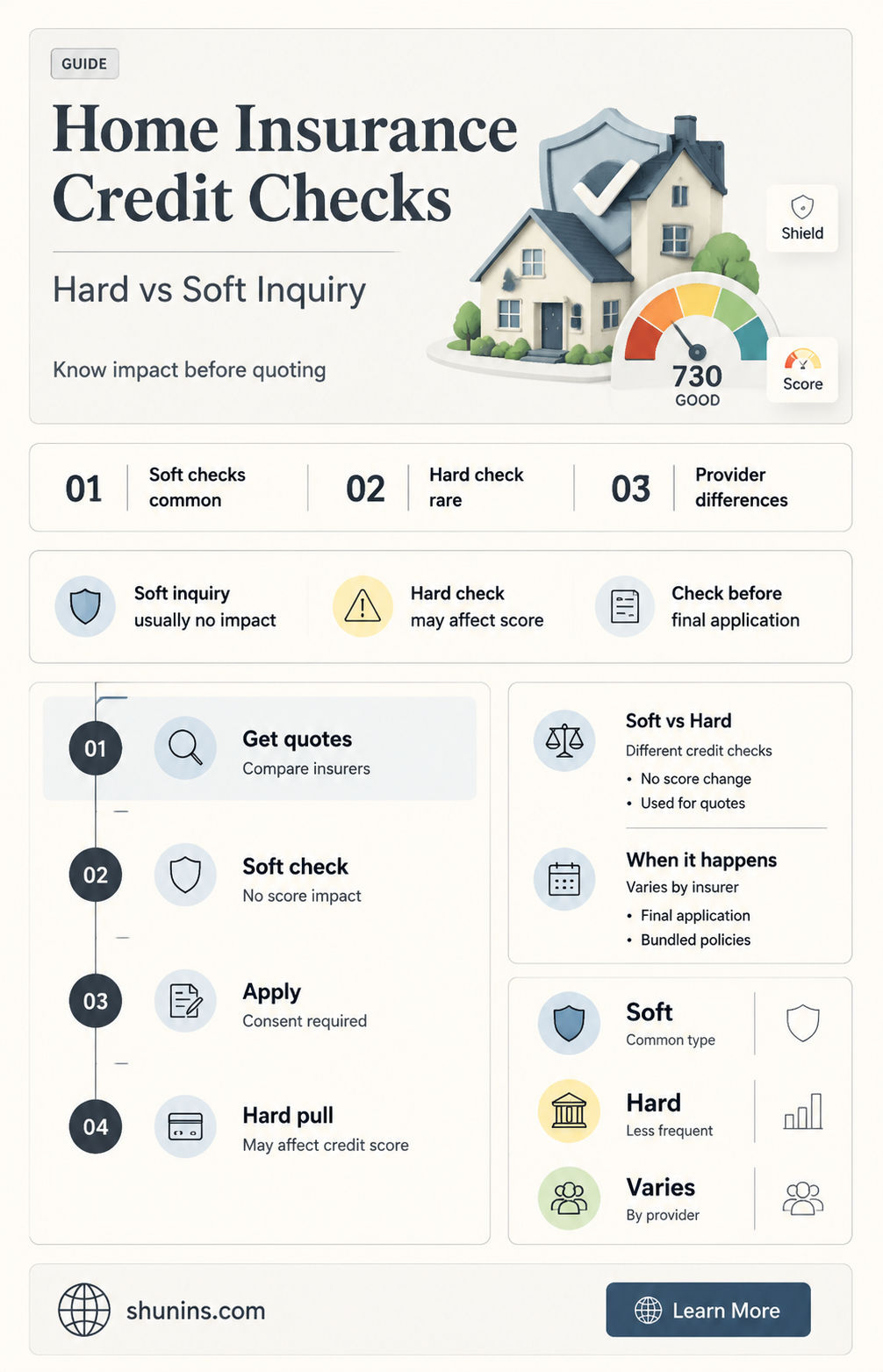

Homeowners insurance quotes are soft pulls, which means that they do not negatively impact your credit score. Soft pulls occur when you are not asking for money, and insurance companies use them to assess your risk of filing a claim. While your credit score can impact your insurance rates, it is not the only factor. In states like California, Maryland, and Massachusetts, credit scores are banned from being used to determine insurance rates. When shopping for homeowners insurance, it is recommended to get multiple quotes to find the best rate.

| Characteristics | Values |

|---|---|

| Homeowners insurance quotes impact on credit score | Does not hurt credit score |

| Type of credit check | Soft pull |

| Soft pull visibility | Soft pulls are not visible to lenders |

| Soft pull impact on insurance rates | Soft pulls do not impact insurance rates |

| Soft pull impact on insurance eligibility | Soft pulls do not impact insurance eligibility |

| States that ban the use of credit scores in insurance rates | California, Maryland, Massachusetts, Michigan |

Explore related products

What You'll Learn

![]()

Homeowners insurance quotes are soft pulls

While your credit score can impact how much you pay for homeowners insurance, it is not the only factor. In many states, credit-based insurance scores can affect your homeowners insurance offers and rates. However, even in these states, your credit score is not the sole factor in an insurance company's decision. Your credit history is used to generate a credit-based insurance score, which is then used to determine your eligibility and premiums. This score incorporates details from your credit report and may include other information.

In some states, the use of credit scores in determining homeowners insurance rates is restricted or banned. These states include California, Maryland, Massachusetts, and Michigan. If you live in one of these states, your credit score will not impact your homeowners insurance rates. However, it is still important to shop around and compare rates to find the best option for you.

When shopping for homeowners insurance, it is recommended to get multiple quotes. This allows you to compare rates and find the most affordable option. By getting multiple quotes, you can also see how each company weighs your credit history when determining your premiums. This can help you find the best option for your specific situation.

Protecting Your Art: What Home Insurance Covers

You may want to see also

Explore related products

![]()

Soft pulls don't affect your credit score

When it comes to homeowners insurance quotes, it's important to understand the difference between hard and soft pulls and their impact on your credit score. Getting homeowners insurance quotes typically involves a soft pull of your information, which means your credit score remains unaffected.

Soft pulls, also known as soft credit checks or soft inquiries, do not impact your credit score. This is because they are not attached to a specific application for credit. When you request a quote, the insurance company performs a soft pull to assess your risk and determine your insurance rates, but this type of inquiry is not visible to lenders and does not indicate that you are trying to borrow money.

Soft pulls are commonly used in situations where you are not asking for credit or a loan. For example, background checks for employment or pre-approvals for certain credit card offers are instances where a soft pull may be conducted. Since soft pulls are not indicative of greater risk, they won't leave a negative mark on your credit report or lower your credit score.

In the context of homeowners insurance, multiple quotes from different companies may be encouraged to find the best rates. Soft pulls allow you to shop around without worrying about any negative consequences on your credit score. This is particularly beneficial when you are looking to improve your credit score, as it gives you the flexibility to explore various options without any adverse effects.

While soft pulls don't affect your credit score, it's worth noting that hard pulls, or hard credit inquiries, can have an impact. Hard pulls are typically done by financial institutions before making lending decisions, such as providing a loan or issuing a new credit card. These inquiries indicate that you are actively seeking to borrow money, and they are visible to other lenders. As a result, hard pulls can temporarily lower your credit score and may affect your ability to obtain credit in the short term.

Mortgage Insurance: Protecting Your Home Loan

You may want to see also

Explore related products

![]()

Hard pulls are done by financial institutions before lending

When it comes to lending decisions, financial institutions will often perform a hard credit check, also known as a hard pull. This occurs when an individual is seeking to borrow money, such as applying for a loan or credit card. Hard pulls can impact an individual's credit score and are visible to other lenders. This type of credit check indicates that the person is actively seeking additional credit.

In the context of homeowners insurance quotes, it's important to understand the difference between hard and soft pulls. Soft credit checks, or soft pulls, occur when an individual is not directly asking for money. Getting insurance quotes typically falls under this category. Soft pulls do not affect an individual's credit score, even if multiple quotes are obtained. This is because insurance companies are not making a lending decision but rather providing a quote based on the individual's information.

While soft pulls from insurance companies don't impact credit scores, it's worth noting that insurance rates can be influenced by credit history. In most states, insurance companies are allowed to consider an individual's credit score when determining rates. However, it is not the sole factor, and other criteria are also taken into account. Additionally, certain states, such as California, Maryland, Massachusetts, and Michigan, have made efforts to restrict or ban the use of credit scores in determining homeowners insurance rates.

It's important for individuals to be mindful of their credit history and how it can impact various financial aspects, including homeowners insurance. While shopping for insurance and obtaining quotes, individuals should be aware that insurance companies may perform soft pulls, which will not negatively affect their credit scores. This encourages individuals to compare rates and make informed decisions without worrying about their credit being affected by multiple inquiries.

In summary, hard pulls are typically associated with lending decisions made by financial institutions, while soft pulls are common in the insurance quoting process. Understanding this distinction can help individuals navigate their financial journeys and make informed choices regarding their homeowners insurance options.

Mortgage Insurance: Governmental Policies and Your Home

You may want to see also

Explore related products

![]()

Credit scores impact homeowners insurance rates

Homeowners insurance quotes are soft pulls, which means they do not negatively impact your credit score. Soft pulls occur when you are not asking for money, and insurance quotes are one example. Since you can get as many insurance quotes as you want without buying a policy, an insurance company's soft pull of your credit information will not affect your credit score. However, hard credit checks are done by financial institutions before making a lending decision and can affect your credit score.

Credit scores can impact homeowners' insurance rates, and maintaining a good credit score can help you get the best price from most home insurance companies. While insurers may consider other factors when determining rates, such as your home's characteristics, claims history, and marital status, credit scores are a significant factor in calculating premiums. A high credit score indicates good lending and repayment practices, which is favourable to insurers.

In most states, insurers use credit-based insurance scores (CBI) to determine home insurance rates. CBI scores are derived from credit scores and are used to assess an individual's risk of filing a claim. While each insurer calculates CBI scores differently, they are generally affected by similar factors as credit scores, such as payment history and debt. A good credit score is typically between 690 and 719, while a score below 630 is considered poor.

The impact of credit scores on insurance rates varies by state and insurer. In California, Maryland, Massachusetts, and Michigan, the use of credit scores to determine insurance rates is restricted or banned. In these states, insurance companies cannot use credit history as a rating factor, and a low credit score will not impact insurance costs. However, in most other states, a poor credit score can lead to significantly higher insurance premiums. For example, a NerdWallet analysis found that someone with good credit pays an average of $2,110 per year for homeowners insurance, while someone with poor credit pays an average of $3,620 per year, over 71% more.

It is important to note that while credit scores are a factor, they are not the sole determinant of homeowners' insurance rates. Other factors, such as claims history and home maintenance, can also play a significant role in calculating premiums. Additionally, some insurers may offer leniency for customers with bad credit scores due to extraordinary life events, such as illness or the death of a family member.

Mortgage Insurance: What Laws Govern Private Policies?

You may want to see also

Explore related products

![]()

Some states ban using credit scores for insurance rates

When shopping for homeowners insurance, insurance companies may request a credit check to assess your risk of filing a claim. This is known as a soft pull, which will not affect your credit score. However, it's important to note that practices may vary depending on the state you live in.

In recent years, some states have restricted or banned the use of credit scores in determining insurance rates or approving policies. This is because credit scores may not accurately predict an individual's risk and can disproportionately affect certain groups, such as low-income consumers and minorities. As of 2025, California, Hawaii, Maryland, Massachusetts, and Michigan have implemented bans or restrictions on using credit scores for homeowners insurance rates. Here's a closer look at the regulations in these states:

- California: Insurance companies in California are prohibited from using credit-based scores or credit history for underwriting or setting rates for homeowners insurance. As a result, your credit standing will not impact your ability to obtain or renew a policy or the amount you pay in premiums.

- Hawaii: While Hawaii bans the use of credit ratings for auto insurance, it is unclear if the same restrictions apply to homeowners insurance.

- Maryland: Homeowners insurance companies in Maryland cannot refuse coverage, cancel a policy, deny renewal, or base insurance rates on an individual's credit history. However, credit information can be used to determine auto insurance rates.

- Massachusetts: Insurance companies in Massachusetts are banned from using credit scores or credit information when setting rates, underwriting, or renewing both auto and homeowners insurance policies.

- Michigan: Both home and auto insurers in Michigan are prohibited from using credit scores or credit information when approving, denying, cancelling, or renewing policies. Credit scores cannot be used to determine insurance rates for either type of insurance.

It's worth noting that these regulations are subject to change, and other states may also have introduced similar restrictions since 2025. While these states have taken steps to limit the impact of credit scores on insurance rates, most states still allow insurance companies to use credit-based insurance scores when making decisions about whom to insure and how much to charge.

Guitar Center Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

Soft pull.

No, it will not. Soft pulls do not affect your credit score.

No. While most companies do a soft pull, there is a chance that some may do a hard pull.

A high credit score is better for your homeowners insurance rates. It indicates good lending and repayment practices, which is favourable to your insurer. However, it is not the sole factor.

Yes, California, Maryland, and Massachusetts have banned the use of credit scores to determine insurance rates.