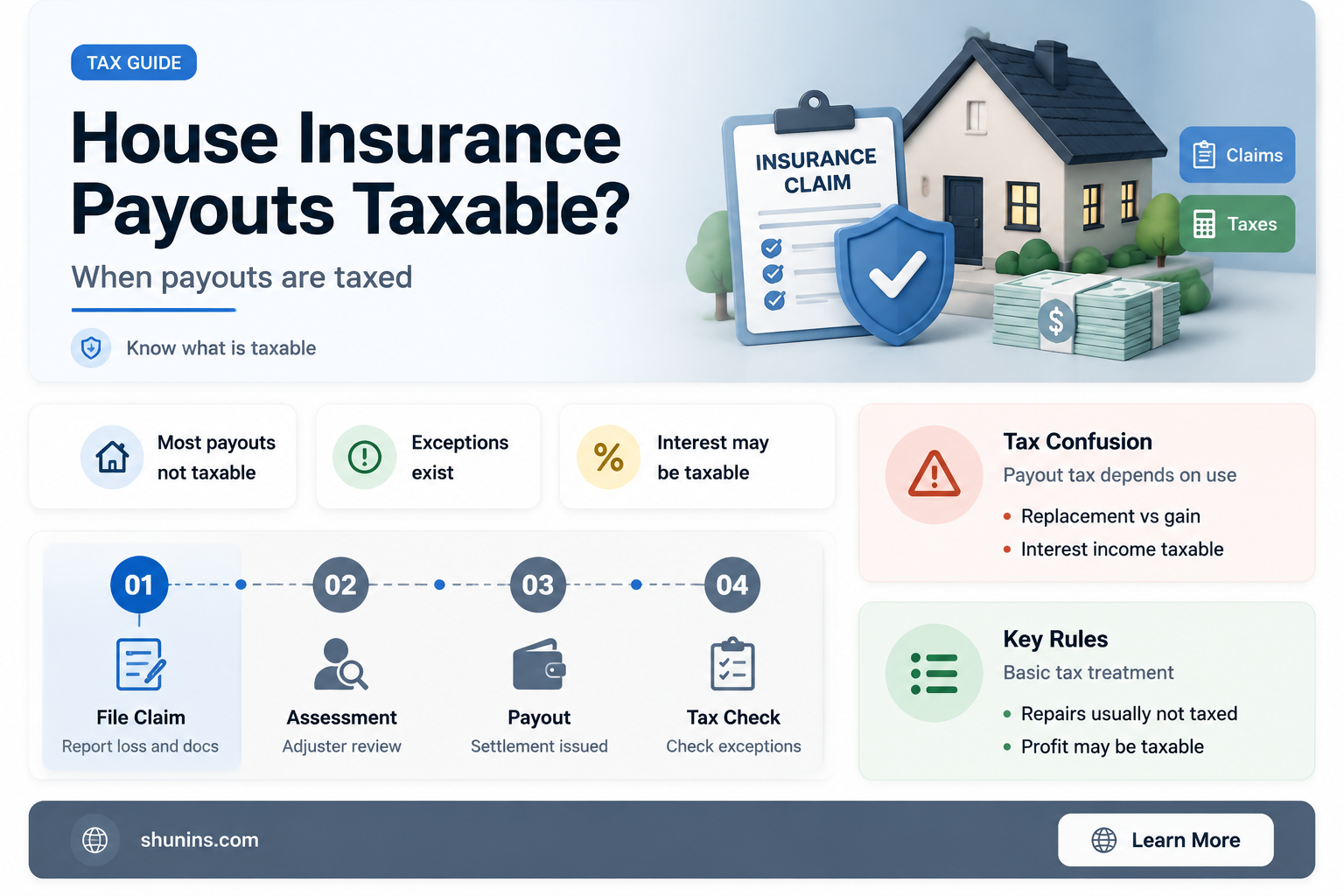

Generally, house insurance payouts are not taxable, as they are not considered income—you're simply restoring the original state of your assets. The IRS taxes your wages and any source of income that increases your wealth. Unless your insurance company overpays you, your payout isn't considered income. You'll likely use the money for repairs, so you're not gaining anything. Even if you decide against repairing your home, the payment replaces lost wealth and doesn't signify a capital gain.

| Characteristics | Values |

|---|---|

| Are house insurance payouts taxable? | Generally, house insurance payouts are not taxable as they are not considered income. |

| When are house insurance payouts taxable? | House insurance payouts may be taxable if: |

| 1. There is leftover money from the claim after repairs have been carried out. | |

| 2. The claim is for rental property damage as it could be considered rental income. | |

| 3. The claim is for an investment property and the money is not reinvested to repair or replace the property quickly enough. |

Explore related products

What You'll Learn

- Home insurance payouts are generally not taxable

- If the insurance company overpaid you, the leftover money may be taxable

- If you made a claim for rental property damage, you might need to pay taxes

- If you profit from the insurance payout, it may be taxable

- If you deduct part of the cost of your car as a business expense, the insurance benefit might be considered a gain

![]()

Home insurance payouts are generally not taxable

The same logic applies to repairs. If your kitchen is destroyed in a fire, your insurance settlement will pay for a new kitchen, plus any repairs, plastering, and redecorating needed to return your kitchen to its previous state. This is known as the principle of indemnification. As long as you receive the right amount of money to fix the damage or replace items, you don't need to report the settlement to the IRS. It's up to you how you spend the payout, but what matters to the IRS is that you receive a check corresponding to the value of what was lost and that you made no profit from the transaction.

However, there are some situations in which home insurance payouts may be taxable. If you have any leftover money from your home insurance claim, it may be taxable. This typically applies if you were overpaid by the insurance company, not if you saved money by doing the repairs yourself. If you made a claim for rental property damage, you might need to pay taxes because it could be considered rental income. If you are unsure, it is recommended that you speak to a tax professional for advice.

Phil's Absence: Unraveling the Mystery Behind Mickelson's Skipped Farmers Insurance Open

You may want to see also

Explore related products

$11.25 $16.99

![]()

If the insurance company overpaid you, the leftover money may be taxable

Generally, money received as part of an insurance claim or settlement is not taxed. This is because the purpose of insurance is to "make you whole" again, meaning you should only receive enough payment to bring you back to the state you were in before an incident occurred. In this case, you are not gaining anything, and therefore you have no taxable income.

However, if the insurance company overpaid you, any leftover money may be taxable. This is because you have received more than the amount required to fix the damage or replace items, and therefore your wealth has increased. In this case, you will need to report the gain as income and pay taxes on it.

It is important to note that using a claims payout for anything other than the approved repairs may be considered insurance fraud. If you have leftover money from a claims payout, it is recommended to contact your insurance provider to determine the best course of action.

Additionally, if you have a mortgage on your home, your claims checks may be payable to both you and your mortgage lender. This can make handling excess funds more complicated, as you will need your mortgage lender's permission to cash the check and send back any overage.

If you are unsure about what to do with leftover money from a home insurance claim, it is best to seek advice from a tax professional. They can provide guidance on properly documenting repairs and ensuring you do not trigger an audit.

Farmers Insurance and Pit Bulls: Understanding the Policy Pitfalls

You may want to see also

Explore related products

![]()

If you made a claim for rental property damage, you might need to pay taxes

If you made a claim for rental property damage, you may need to pay taxes on the payout because it could be considered rental income. This is because the IRS taxes your wages and any source of income that increases your wealth. However, if you use the payout to repair your rental property, you are not gaining anything, and it won't be taxable.

Rental income is any payment received for the use or occupation of property. This includes advance rent, security deposits used as final rent payments, payments for cancelling a lease, expenses paid by the tenant, and property or services received instead of money as rent. If you own a part interest in the rental property, you must report your share of the rental income.

If you receive rental income, you can deduct certain expenses from your taxes, such as mortgage interest, property tax, operating expenses, depreciation, repairs, and insurance premiums. These deductions can help offset the tax burden on rental income, including any received through insurance claims.

It's important to keep good records of your rental income and expenses, as you may need to provide documentation in the event of an audit. Consult a tax professional if you have concerns about your specific situation.

The Hunt for the Farmers Insurance Open: A Guide to the Tournament's Historic Venues

You may want to see also

Explore related products

![]()

If you profit from the insurance payout, it may be taxable

Typically, house insurance payouts are not taxable, as they are not considered income—you are simply restoring the original state of your assets. The IRS taxes your wages and any source of income that increases your wealth. However, if you profit from the insurance payout, it may be taxable.

If the insurance company overpaid you or if you performed the repair yourself and paid yourself for it, you may have to pay taxes on the leftover money from your claim. This is because the leftover money is considered a gain in excess of the original value of the property, also known as an "involuntary conversion gain" by the IRS. In such cases, you will need to report this gain as income on Form 1040 in the year you received the insurance money and pay taxes at your standard income tax rate.

There are, however, some exclusions to reduce your tax liability in the event of an involuntary conversion gain. The first is the primary residence exemption. If your main home was damaged or destroyed, and you lived there for at least two of the five years prior to the insurance event, you can exclude up to $250,000 in insurance gains ($500,000 if you file jointly). The second option is a gain deferral election, where you use your insurance check to replace the damaged property with a similar property, allowing you to defer the involuntary conversion gain until you sell the new property.

Farmers Insurance Exchange: A Reputable Option for Consumers?

You may want to see also

Explore related products

![]()

If you deduct part of the cost of your car as a business expense, the insurance benefit might be considered a gain

Generally, money received as part of an insurance claim or settlement is not taxed as it is not considered income by the IRS. The purpose of insurance is to restore your finances to their previous state after an incident, meaning you are not profiting from the transaction. However, if you deduct part of the cost of your car as a business expense, the insurance benefit might be considered a gain.

If you use your car for both personal and business purposes, you can only deduct the cost of its business use. This can be calculated using one of two methods: the standard mileage rate or the actual expense method. The standard mileage rate for 2019 is 58 cents per mile. The actual expense method involves determining the cost of operating the car for the business portion of the overall use, including gas, repairs, insurance, and depreciation.

If you are self-employed or a business owner, you may deduct car expenses on your tax return. Other individuals who can deduct car expenses include armed forces reservists, qualified performing artists, and fee-basis state or local government officials. These deductions can be reported on Schedule C (Form 1040) or Form 2106, depending on the scenario.

It is important to note that you must choose between deducting standard mileage and actual vehicle expenses, as you cannot claim both. Additionally, you will need to keep adequate records to substantiate your expenses. Consulting a tax professional can provide further guidance on properly documenting expenses and navigating any tax implications.

Farmers Insurance Open: A Multi-Day Golfing Extravaganza

You may want to see also

Frequently asked questions

No, house insurance payouts are not considered taxable income. However, if you profit from the insurance claim, you may have to pay taxes on the profit.

If the insurance company overpaid you or if you performed the repair yourself and paid yourself for doing so.

If you own rental property, you may need to pay taxes on any insurance payouts as they could be considered a type of income.

It doesn't matter to the IRS how you spend the money. As long as you don't profit from the transaction, you don't need to report it.

If the settlement is lower than the amount you spend on repairs, there is no taxable gain and there may even be an insurance loss.