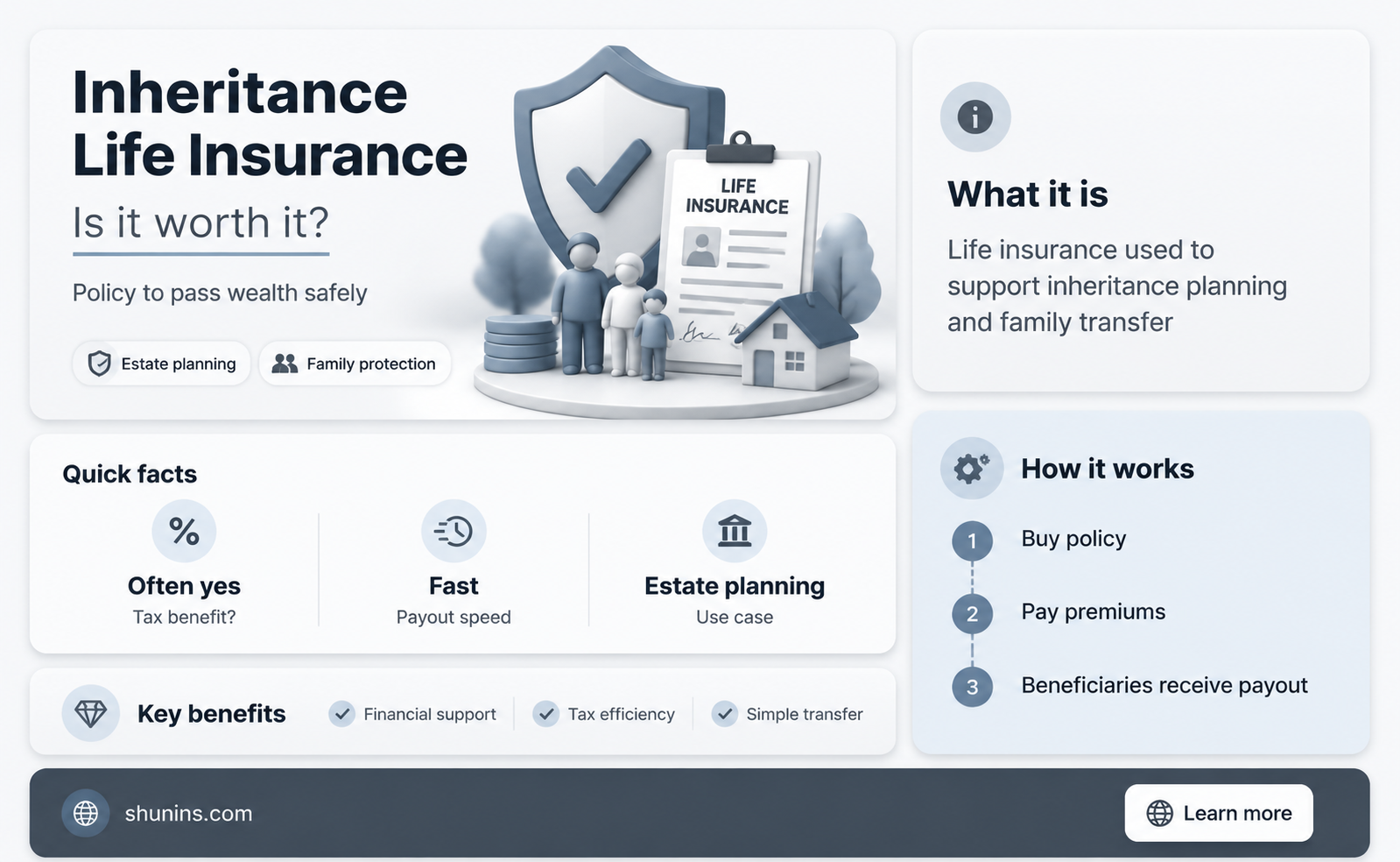

Life insurance is a valuable tool for inheritance planning, offering several benefits over traditional inheritance methods. It guarantees a payout to your chosen beneficiaries, bypassing probate and ensuring your loved ones receive financial support promptly. Unlike inheritances, life insurance payouts are not considered part of your estate, so they aren't reduced by any debts you owe. Additionally, life insurance proceeds are typically tax-free, providing your beneficiaries with the full sum.

While life insurance can be an effective way to leave an inheritance, it's important to understand the different types of policies available, such as term life and permanent life insurance, and their respective advantages and disadvantages.

| Characteristics | Values |

|---|---|

| Payout | Goes directly to beneficiaries |

| Tax | Tax-free |

| Purpose | Can be used for any purpose |

| Probate | Not required |

| Debt | Not used to pay off debts |

| Beneficiaries | Can be individuals or an estate/trust |

| Cost | Permanent life insurance is more expensive than term life insurance |

Explore related products

$12.99 $14.95

$16.99 $16.99

What You'll Learn

- Life insurance can be used to leave an inheritance to your heirs tax-free

- It can be an effective tool for financial planning and estate planning

- Life insurance policies are not subject to probate, meaning quicker payouts to beneficiaries

- Life insurance proceeds can be used to cover funeral costs, pay off debts, and provide financial security for loved ones

- There are different types of life insurance policies, such as term life insurance and permanent life insurance, each with its own advantages and considerations

![]()

Life insurance can be used to leave an inheritance to your heirs tax-free

Life insurance is a way to leave an inheritance to your heirs without them having to pay taxes on it. When the policyholder of a life insurance policy passes away, the proceeds or death benefits are paid to the named beneficiary or beneficiaries. This money is generally not taxable income for the beneficiary, meaning they don't have to report it on their taxes.

However, there are some situations where taxes may be owed on a life insurance payout. If the payout is structured as multiple payments over time, rather than a lump sum, the payments may include proceeds and interest, and the interest may be subject to taxes. Similarly, if the policyholder has withdrawn money or taken out a loan against the policy, any proceeds paid out may be taxable if the amount withdrawn is more than the total amount of premiums paid.

If the policyholder names their estate as the beneficiary, rather than an individual, the person or people inheriting the estate may have to pay estate taxes. According to the IRS, if life insurance proceeds are included as part of the deceased's estate and together exceed the federal estate tax threshold of $12.92 million (as of 2023), estate taxes must be paid on the proceeds over the allowed limit.

Life insurance can be a useful tool for leaving an inheritance, as the proceeds typically go directly to the beneficiaries without having to go through probate or pay off any outstanding debts of the estate. This means that beneficiaries will receive the payout regardless of how the estate is handled. However, it is important to regularly review the beneficiaries and policy details to ensure that all information is up to date and to communicate any changes in circumstances.

Understanding Tax Implications of Life Insurance Cash Surrender

You may want to see also

Explore related products

$32 $32

![]()

It can be an effective tool for financial planning and estate planning

Life insurance can be an effective tool for financial planning and estate planning in several ways. Firstly, it guarantees a payout to your beneficiaries, ensuring that your loved ones receive financial support after your death. This payout is typically tax-free and can be used for various purposes, such as covering final expenses, burial costs, and providing financial security for your family.

Another advantage of life insurance is that it sidesteps probate, which is the process an inheritance usually needs to go through. Life insurance is paid out immediately upon being processed, rather than being caught up in the estate for an extended period. This timely payout can relieve financial strain on your family and help cover immediate expenses.

Additionally, life insurance is not subject to the same tax implications as traditional inheritances. While inheritance tax can be considerable for large estates, life insurance proceeds are generally not taxed as income. By using life insurance, you can ensure that the full death benefit goes to your beneficiaries.

Life insurance also offers flexibility in how the payout is distributed. Beneficiaries can choose to receive a lump-sum payout or establish an annuity, receiving installment payments over several years. This option can be beneficial for beneficiaries who need to manage their money over a longer period and want to avoid the burden of large expenses right away.

Furthermore, life insurance can be particularly useful if you started saving for retirement later in life. It can provide a cost-effective way to ensure a financial legacy for your loved ones, even if you don't have significant savings.

Overall, life insurance can be a valuable component of your financial and estate plan, providing peace of mind that your beneficiaries will receive financial support and allowing you to plan for the distribution of your assets according to your wishes.

GST and Life Insurance: What's the Connection?

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Life insurance policies are not subject to probate, meaning quicker payouts to beneficiaries

However, if there is no named beneficiary or if the named beneficiary has died, the life insurance funds will be paid to the estate and will be subject to probate. It is therefore important to keep beneficiary designations up to date. For example, after a divorce, it is important to change the beneficiary of a life insurance policy to avoid the proceeds going to an ex-spouse.

Life insurance policies can be written into a trust, which means that the payout is made from the trust and not the estate, and is usually exempt from taxes.

Do I Have Mortgage Life Insurance?

You may want to see also

Explore related products

![]()

Life insurance proceeds can be used to cover funeral costs, pay off debts, and provide financial security for loved ones

Life insurance is a way to provide financial security for your loved ones after you're gone. It can be used to cover funeral costs, pay off debts, and provide financial support during a difficult time. Here are some key ways in which life insurance proceeds can be beneficial:

Covering Funeral Costs

Funerals can cost upwards of several thousand dollars, and many people don't plan ahead for these expenses. Burial insurance and preneed funeral insurance are two types of life insurance policies designed to cover funeral costs. Burial insurance pays the death benefit directly to the beneficiary, who can use the money as they see fit, including for funeral expenses, medical bills, legal costs, or other debts. Preneed funeral insurance, on the other hand, is paid directly to the funeral service provider to cover predetermined expenses such as funeral home services, merchandise, and burial services.

Paying Off Debts

Life insurance can also help protect your loved ones from inheriting your debt. In most cases, debt does not disappear when you die, and it can become the responsibility of your estate or surviving family members. Life insurance proceeds can be used to pay off these debts, including unsecured debts like credit card debt and secured debts like mortgages or auto loans. This can prevent your loved ones from having to sell off assets to pay off creditors.

Providing Financial Security

Life insurance can provide financial security for your family, especially if they rely on your income for support. It can help them maintain their standard of living, cover medical expenses, and provide peace of mind during a difficult time. The death benefit from a life insurance policy is typically tax-free, and beneficiaries can use the money for any purpose, such as daily living expenses, education, or maintaining their current lifestyle.

In summary, life insurance proceeds can be used to cover funeral costs, pay off debts, and provide financial security for loved ones. By planning ahead with life insurance, you can ensure that your family has the financial support they need during a challenging time.

Fidelity's Ladder Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

There are different types of life insurance policies, such as term life insurance and permanent life insurance, each with its own advantages and considerations

There are two main types of life insurance policies: term life insurance and permanent life insurance. Each type has its own advantages and considerations that should be taken into account when deciding which policy is best for your needs.

Term life insurance provides coverage for a specified period, such as 10, 15, 20 years, or until a specified age. The policy will pay out a death benefit to the beneficiaries if the insured person dies during the term. Term life insurance is generally the least costly option as it offers coverage for a restricted time and doesn't build cash value. However, if the policy expires before the death of the insured, there is no payout, and the policy will lapse without any cash value. Term life insurance is ideal for people who want substantial coverage at a low cost.

Permanent life insurance, on the other hand, provides coverage for the entire lifetime of the insured. It is more expensive than term life insurance but offers the security of lifetime protection. Permanent life insurance policies typically have a cash value component, which acts as a savings account and can be used for various purposes, such as taking out loans or paying policy premiums. The cash value also grows over time, providing additional financial benefits. People who buy permanent life insurance pay more in premiums but have the advantage of knowing they are protected for life.

When choosing between term and permanent life insurance, it's important to consider your financial situation, the length of coverage needed, and the desired level of protection. Term life insurance is suitable for those who want affordable coverage for a specific period, while permanent life insurance is designed for those seeking lifelong protection and additional financial benefits.

In addition to these main types, there are also other variations of life insurance policies, such as whole life insurance, universal life insurance, and variable universal life insurance, each with its own unique features and considerations. It's essential to carefully review the terms and conditions of different policies to determine which one aligns best with your specific circumstances and goals.

DUI's Impact on Life Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Life insurance can be a good way to provide an inheritance for your loved ones, as it offers several benefits:

- The payout goes directly to your beneficiaries, bypassing probate and any outstanding debts.

- The death benefit is typically tax-free.

- Your beneficiaries can use the payout for any purpose.

- Life insurance policies pay out more at a fraction of the cost.

- Life insurance will always pay to specific beneficiaries, whereas a will can be contested.

- Life insurance isn't taxed in the same way that an inheritance can be.

The two main types of life insurance are term life and permanent life. Term life insurance covers a set number of years (e.g. 10, 20 or 30 years), while permanent life insurance can last your entire life. If you want a long-term policy, consider permanent coverage such as whole life insurance. If you only need temporary coverage, term life insurance may be a more affordable option.

When you buy life insurance, you choose the amount of coverage you want. This is the sum of money your beneficiaries will receive upon your death, known as the "death benefit". You can choose to have the payout distributed as a lump sum or in installments. You can also designate an estate or trust as the beneficiary, in which case the proceeds will be distributed according to the instructions in a will or trust document.