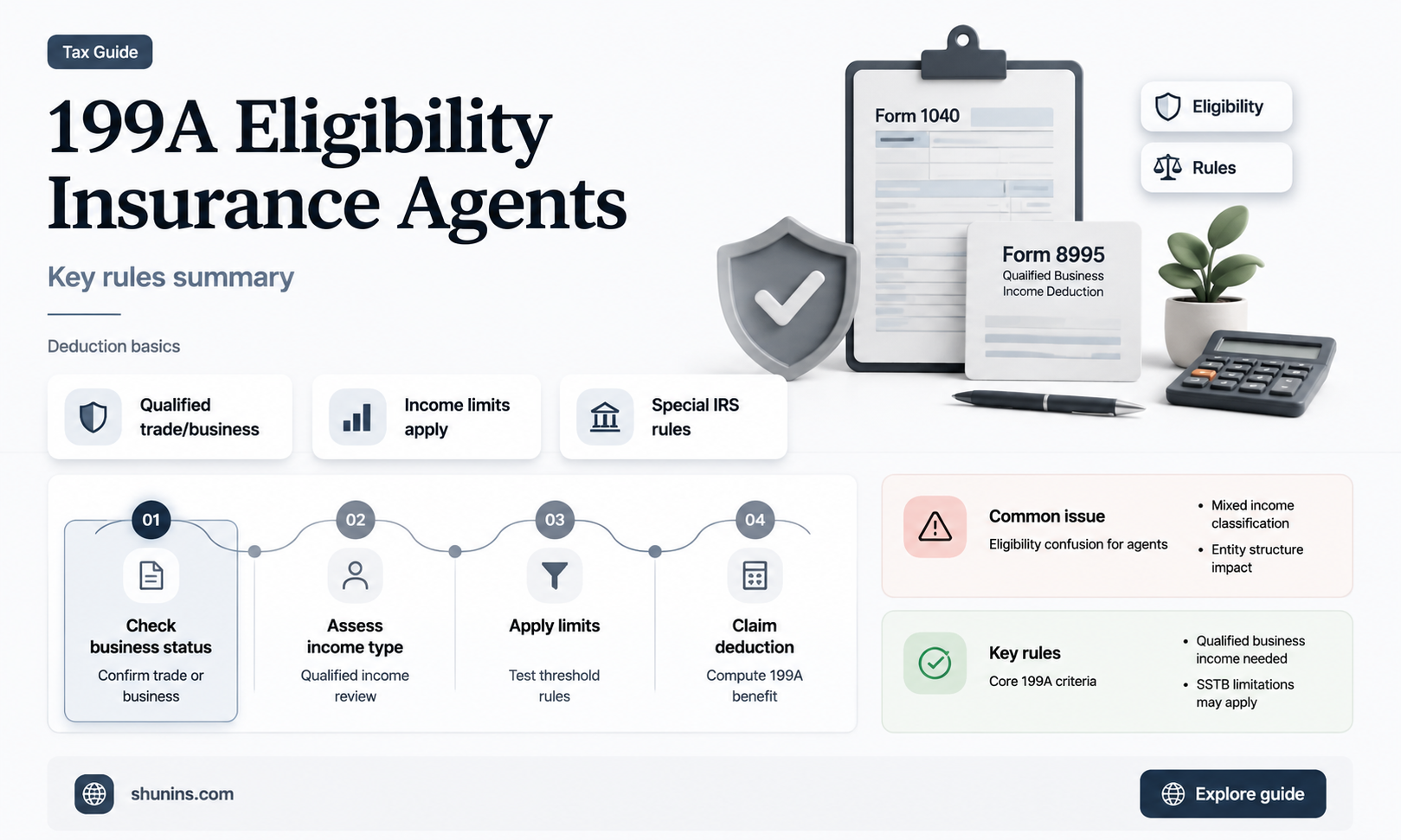

The Section 199A QBI (Qualified Business Income) deduction, also known as the pass-through income deduction, allows eligible taxpayers to deduct up to 20% of their QBI. While this deduction is applicable to a wide range of businesses, there has been confusion and debate about whether insurance agents are eligible for this deduction. This is because insurance agents are treated as selling their company's products rather than their personal services, and their work does not fall under the specified service business category. However, insurance agents who are also brokers, registered representatives, or RIAs may be able to preserve the QBI deduction, especially if they are high-income earners.

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

What You'll Learn

- Insurance agents are not considered a specified service business

- The 199A deduction is available for small businesses

- The 199A deduction is a 20% deduction

- The 199A deduction is available for the first time on 2018 federal income tax returns

- The 199A deduction is available for owners of sole proprietorships, partnerships, S corporations, and some trusts and estates

![]()

Insurance agents are not considered a specified service business

The Tax Cuts and Jobs Act, which was signed into law in December 2017, introduced a new tax deduction for "qualified business income" (QBI) under Section 199A. This deduction allows eligible taxpayers to deduct up to 20% of their QBI. However, it is not available for income earned by providing services as an employee or for certain specified service trades and businesses (SSTBs).

SSTBs are defined as professional service businesses in fields such as accounting, legal, health, actuarial science, performing arts, financial services, and brokerage services. Interestingly, Congress specifically excluded insurance producers, brokers, and agents from this list. This is because they are considered to be selling their company's products rather than their personal services. As a result, insurance agents are not considered a specified service business and can take advantage of the QBI deduction.

The distinction between selling products and providing personal services is crucial in determining eligibility for the QBI deduction. While investment advisors, registered representatives, wealth planners, and retirement advisors are considered specified service businesses, insurance professionals are not. This is because their primary role is to sell insurance products on behalf of their companies rather than offer personal services.

However, the situation becomes more complex when insurance professionals also provide brokerage services or have RIA (registered investment advisor) income. In such cases, if the income from investment-related activities exceeds 10%, the entire business may be classified as an SSTB, making it ineligible for the QBI deduction. To overcome this challenge, some advisors may consider structuring their businesses separately, with one entity focused on brokerage/RIA services and another on insurance.

In conclusion, insurance agents are not considered a specified service business under Section 199A. This exclusion allows them to benefit from the QBI deduction, which can provide significant tax advantages. However, the complexity arises when insurance agents have multiple revenue streams, potentially including income from investment-related activities, which may impact their eligibility for the deduction.

Military Insurance: Private or Public?

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY218_.jpg)

$12.49 $21.99

![]()

The 199A deduction is available for small businesses

The 199A deduction, also known as the Qualified Business Income (QBI) deduction, is a significant tax break for small business owners. It allows eligible taxpayers to deduct up to 20% of their QBI, providing substantial savings on tax bills. This deduction applies to income from partnerships, S corporations, sole proprietorships, certain trusts, and estates. However, it excludes income from C corporations or employment services.

The QBI deduction was introduced as part of the Tax Cuts and Jobs Act, bringing about significant changes to the tax code. It is designed to benefit small businesses, including those with pass-through income structures. For these businesses, the 199A deduction can reduce taxable income by a considerable amount, making it an attractive incentive for small business owners.

To be eligible for the 199A deduction, businesses must meet specific criteria. Firstly, the income must be generated within the United States, excluding foreign-sourced income and operations conducted outside US borders. Additionally, there are limitations for upper-income households, with thresholds set at $163,300 of qualified business income for single taxpayers and $326,600 for married taxpayers filing jointly in 2020.

The 199A deduction is particularly beneficial for businesses with high expenses. By strategically allocating expenses to the specified service business, businesses can maximize profits in the non-specified service business, which is more likely to qualify for the 199A QBI deduction if the business has high overall income. This strategy can result in significant tax savings for small businesses with complex structures.

While the 199A deduction offers attractive tax benefits, determining eligibility and calculating the deduction can be complex. Small business owners should carefully review the requirements and consult relevant resources, such as IRS guidelines and tax advisory services, to ensure accurate compliance and maximize their tax advantages.

A Comprehensive Guide to Understanding Avesis Insurance

You may want to see also

Explore related products

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UY218_.jpg)

![]()

The 199A deduction is a 20% deduction

The 199A deduction, also known as the Qualified Business Income (QBI) deduction, is a significant provision of the Tax Cuts and Jobs Act (TCJA) that allows eligible taxpayers to deduct up to 20% of their QBI. This deduction is applicable to income from sole proprietorships, partnerships, and S corporations, and certain trusts and estates. It is important to note that this deduction is only available for income generated within the US and does not include foreign-sourced income.

The QBI is calculated as 20% of the net amount of qualified items of income, gain, deduction, and loss from any qualified trade or business. This includes income from partnerships, S corporations, sole proprietorships, and certain trusts. Self-employed individuals can also take advantage of this deduction by including the deductible portion of self-employment tax and self-employed health insurance in their QBI calculation.

While the 199A deduction offers a significant benefit to eligible taxpayers, it is important to understand the limitations and qualifications. The deduction is limited to 20% of the taxpayer's taxable income minus net capital gains. Additionally, there are income limitations and business limitations. Specified Service Trades or Businesses (SSTBs), such as those providing health, law, and accounting services, may have partial deductions depending on their income levels.

To correctly calculate the 199A deduction, taxpayers must consider multiple businesses, netting all qualified business income across their enterprises. This involves offsetting positive QBI from one business against negative QBI from another, ultimately impacting overall deduction eligibility. Proper record-keeping and regular self-audits are crucial to ensure compliance with Section 199A rules, as the IRS takes this matter seriously and imposes significant penalties for miscalculations.

ASB Bank Insurance: What You Need to Know

You may want to see also

![]()

The 199A deduction is available for the first time on 2018 federal income tax returns

The 199A deduction, also known as the Qualified Business Income (QBI) deduction, is available for the first time on 2018 federal income tax returns. This deduction was introduced by the Tax Cuts and Jobs Act, which brought about the most significant changes to the tax code in over three decades. The 199A deduction allows eligible taxpayers to deduct up to 20% of their QBI, plus 20% of qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership (PTP) income.

To be eligible for the 199A deduction, taxpayers must be engaged in a ""qualified trade or business." This includes income from partnerships, S corporations, sole proprietorships, and certain trusts. Self-employed individuals can also take advantage of this deduction, which includes the deductible portion of self-employment tax and self-employed health insurance. Additionally, deductions can be made for contributions to qualified retirement plans.

It is important to note that income earned through a C corporation or by providing services as an employee is not eligible for the 199A deduction. However, there is a provision for rental real estate enterprises, where they will be treated as a trade or business for the purposes of the QBI deduction if certain criteria are met. This provision allows individuals and owners of pass-through entities to claim the deduction for rental income.

While the 199A deduction offers significant benefits, it has also been the subject of controversy due to its complex statutory construction and ambiguous legislative text. This has led to disputes between taxpayers and the IRS, and the potential for substantial understatement penalties. Nonetheless, the 199A deduction provides tax advantages for eligible taxpayers and businesses.

Understanding Insurance Coverage for Childbirth and Delivery

You may want to see also

![]()

The 199A deduction is available for owners of sole proprietorships, partnerships, S corporations, and some trusts and estates

The 199A deduction, also known as the Qualified Business Income (QBI) deduction, was introduced in 2017 as part of the Tax Cuts and Jobs Act (TCJA). This deduction aims to establish tax parity between pass-through entities and corporations, providing a tax break for small businesses. The 199A deduction is available for owners of sole proprietorships, partnerships, S corporations, and some trusts and estates, allowing them to deduct a portion of their QBI from their taxable income.

Sole proprietorships, partnerships, and S corporations are considered pass-through business entities, where profits flow directly to the owners' personal tax returns. By including these entities in the 199A deduction, lawmakers aimed to provide them with a tax break similar to the reduced corporate tax rate for corporations. This measure was designed to prevent small businesses from being disadvantaged compared to large corporations.

The 199A deduction allows eligible taxpayers to deduct up to 20% of their QBI. QBI is calculated as the net amount of qualified items of income, gain, deduction, and loss from any qualified trade or business. This includes income from partnerships, S corporations, sole proprietorships, certain trusts, and estates. Additionally, the 199A deduction also allows for the deduction of 20% of qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership (PTP) income.

It is important to note that the 199A deduction is subject to limitations and may not be available to all businesses equally. Upper-income taxpayers and high-income service businesses, such as physicians, lawyers, and consultants, may face additional restrictions or reduced deductions. The deduction is also not applicable to income earned through a C corporation or by providing services as an employee.

The 199A deduction is a complex topic, and determining eligibility and calculating the exact deduction can be challenging. Taxpayers should refer to the latest guidelines and regulations provided by the Internal Revenue Service (IRS) and seek professional tax advice to understand their specific situation and eligibility for the 199A deduction.

The Most Reliable Insurance: Comprehensive Coverage for Peace of Mind

You may want to see also

Frequently asked questions

The 199A deduction, also known as the Qualified Business Income (QBI) deduction, allows eligible taxpayers to deduct up to 20% of their QBI.

Many owners of sole proprietorships, partnerships, S corporations, and some trusts and estates may be eligible for the 199A deduction. Income earned through a C corporation or by providing services as an employee is not eligible.

Yes, insurance agents are eligible for the 199A deduction. Insurance agents are not considered to be conducting specified service businesses and are therefore not excluded from the deduction.

A specified service business (SSTB) is a trade or business that involves the performance of services in a list of specified fields, including health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, and brokerage services.

To claim the 199A deduction, insurance agents need to determine their Qualified Business Income and any other relevant deductions or income. They may also need to separate expenses attributable to different businesses if they are involved in multiple businesses, such as securities.