Insurance payments, also known as insurance premiums, are not always fixed and can vary depending on the type of insurance and other factors. The premium is the amount of money an individual or business pays for an insurance policy, and it can be paid monthly, quarterly, or annually. Insurance companies consider various factors when determining the premium amount, such as age, health, driving record, geographic location, and the type of coverage. Policyholders may have different options for paying their premiums, including installments or upfront payments for the full year. Understanding the factors that influence insurance premiums is essential for individuals and businesses when choosing an insurance policy that fits their needs and budget.

| Characteristics | Values |

|---|---|

| What is an insurance premium? | The amount of money an individual or business pays for an insurance policy |

| How often are insurance premiums paid? | Monthly, quarterly, or annually, depending on the policy |

| How is the premium amount decided? | Based on various factors such as age, health, driving record, geographic location, type of insurance coverage, etc. |

| Are insurance premiums fixed? | It depends on the context; in some cases, the premium amount is fixed, while in others, it varies based on certain factors |

Explore related products

What You'll Learn

- Premiums are based on factors like age, health, and type of insurance

- Premiums are paid monthly, quarterly, or annually, with possible additional charges

- Policyholders may pay premiums in instalments or upfront for the full year

- Insurance companies make money by collecting premiums and investing revenue

- Claims are paid after an adjuster inspects the damage and offers a sum for repairs

![]()

Premiums are based on factors like age, health, and type of insurance

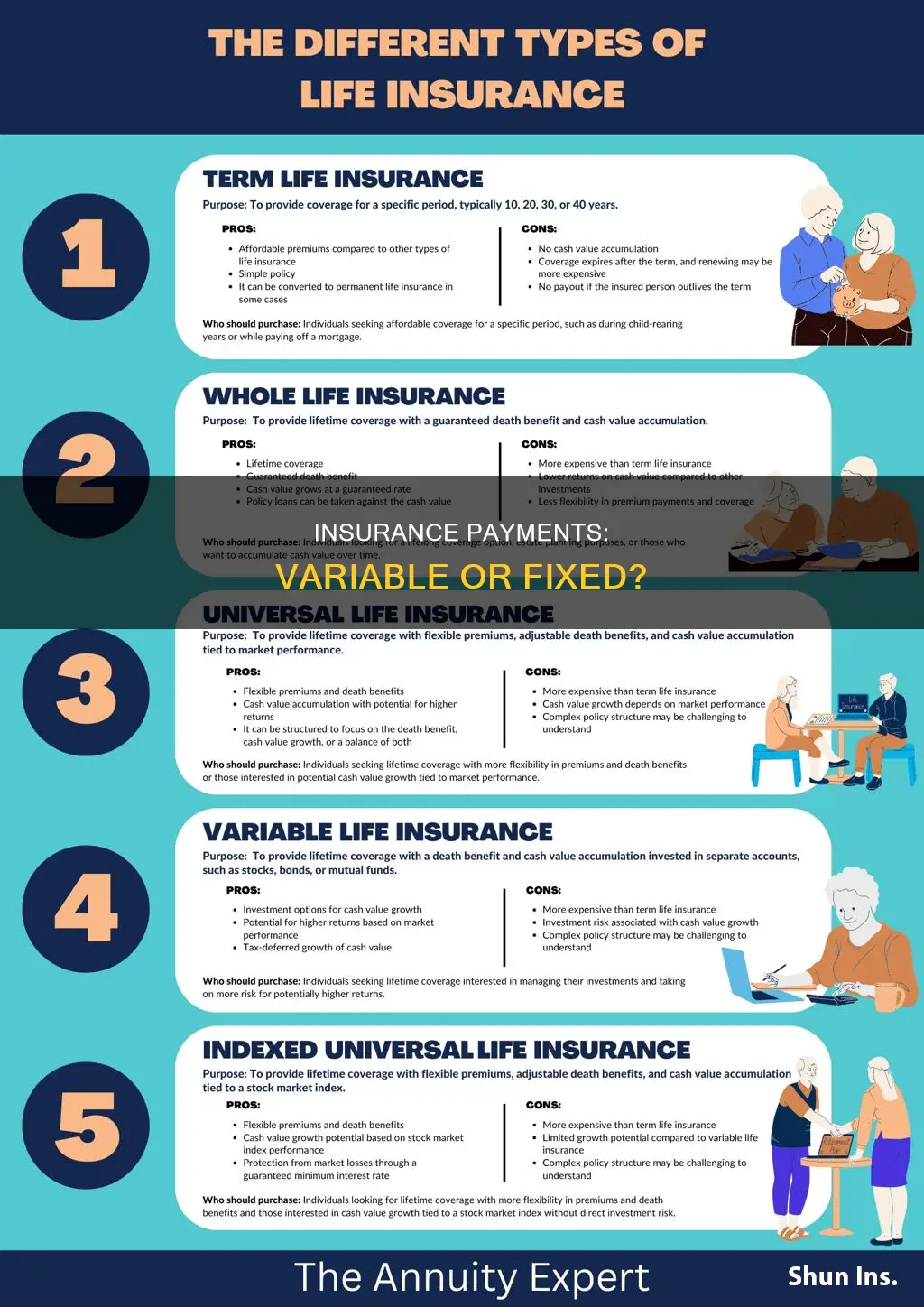

An insurance premium is the amount of money an individual or business pays for an insurance policy. Insurance premiums are paid for policies that cover healthcare, auto, home, life insurance, liability, and other types of protection. The price of the premium depends on a variety of factors, including the type of insurance coverage purchased, the age of the policyholder, their health, and where they live.

When it comes to life insurance, the insured's risk of mortality is a major factor in pricing coverage. The younger you are, the lower your premiums will generally be. Age also affects whether a person will qualify for life insurance coverage at all, with qualifying medical exams getting increasingly stringent as you age. This is because older individuals are more likely to become ill or die while under coverage.

In the case of automobile insurance, the main factors in determining premiums include the policyholder's driving record, geographic location, how often they use their car, the type of car(s) being insured, their gender, credit record, and age. The likelihood of a claim being made is higher for a teenage driver living in an urban area compared to a suburban area, and younger and newer drivers are considered higher-risk than older, more experienced drivers.

Other factors that can influence insurance premiums include the policyholder's history, tobacco use, family size, and the limits on coverage amounts and deductibles. Premiums are often paid monthly, quarterly, or annually, and they can be paid in installments or upfront for the full year. Shopping around and consulting with an independent insurance agent or broker can help individuals find more affordable premiums.

Insurance Producers: Verify Your CE Credits Easily

You may want to see also

Explore related products

![]()

Premiums are paid monthly, quarterly, or annually, with possible additional charges

An insurance premium is the amount of money an individual or business pays for an insurance policy. The premium is the amount you pay to keep your insurance policy in force. Policyholders may choose from several options for paying their insurance premiums, including monthly, quarterly, or annually. Some insurers allow the policyholder to pay the insurance premium in instalments, while others may require an upfront payment for the full year before any coverage starts.

The price of the premium depends on a variety of factors. For example, the main factors in determining automobile insurance premiums include your driving record, your geographic location, how often you use your car, the type of car(s) being insured, your gender, your credit record, and your age. Similarly, in the case of a life insurance policy, the major factors the company looks at in pricing coverage are an insured's risk of mortality, the interest it expects to earn by investing your premium, and the expenses it will incur. The age at which you begin coverage will determine your premium amount, along with other risk factors (such as your current health). The younger you are, the lower your premiums will generally be.

There may be additional charges payable to the insurer on top of the premium, including taxes or service fees. Insurance companies make money by collecting premiums and by investing this revenue in safe financial instruments, such as bonds. If you don't pay all owed premiums, you may lose your coverage dating back to the first month you missed the premium payment. You may also have to wait to get health coverage. A grace period may be available, but you will need to check with your state's Department of Insurance.

Insurance Claims: When to Expect Your Check

You may want to see also

Explore related products

![]()

Policyholders may pay premiums in instalments or upfront for the full year

Policyholders have several options for paying their insurance premiums. The premium is the amount of money an individual or business pays for an insurance policy. Premiums are often paid monthly, quarterly, or annually, depending on the policy. Some insurers allow policyholders to pay premiums in instalments, such as monthly or annually. Other insurers may require upfront payment for the full year before coverage starts.

When signing up for an insurance policy, the insurer will charge a premium to keep the policy in force. The price of the premium depends on various factors, including the age of the insured, the type of insurance coverage, and the likelihood of a claim. For example, younger drivers are considered higher-risk and therefore pay higher premiums than older, more experienced drivers. Similarly, life insurance premiums increase with age, as the risk of mortality is higher.

Policyholders can choose to pay their premiums in instalments or upfront for the full year. Instalment plans can provide flexibility, allowing policyholders to pay in smaller amounts over time. This can be beneficial for expensive premiums or when cash flow is a concern. However, some insurers may require full upfront payment for the year, which could result in a higher initial cost for the policyholder.

Additionally, there may be additional charges on top of the premium, such as taxes or service fees. These charges are payable to the insurer, and policyholders should be aware of these potential extra costs when considering their payment options. When choosing an insurance plan, it is essential to understand the payment structure and any associated fees to make informed decisions about the affordability and suitability of the policy.

In summary, policyholders have the option to pay their insurance premiums in instalments or upfront for the full year, depending on the insurer and the specific policy. The choice between instalments and upfront payment can impact the cash flow and overall cost for the policyholder, so it is important to carefully review the payment options offered by different insurers before selecting a policy.

Penfed Accounts: Are They Federally Insured?

You may want to see also

Explore related products

![]()

Insurance companies make money by collecting premiums and investing revenue

Insurance companies make money by collecting premiums from policyholders and investing those funds to generate additional income. An insurance premium is the amount of money an individual or business pays for an insurance policy. Premiums are often paid monthly, quarterly, or annually, depending on the policy. When you sign up for an insurance policy, your insurer will charge you a premium to keep the policy in force.

The price of the premium depends on a variety of factors, including the age of the insured, their driving record, geographic location, credit record, and the type of insurance coverage purchased. Insurance companies use complex mathematical models to predict how many claims they will need to pay out and set premiums accordingly. If they collect more in premiums than they pay out in claims and operating expenses, they make a profit.

Insurance companies invest the premiums they collect in various financial instruments, such as stocks, bonds, and real estate, to earn a return on their capital. This is known as "float" in the insurance industry. By investing the premium payments, insurance companies can significantly increase their revenue and profit margins.

In addition to investing premiums, insurance companies also generate revenue by underwriting, or assuming the financial risk of an event on behalf of an individual or business. The revenue model for insurance companies may vary depending on the type of insurance, such as auto, health, or property insurance. However, the industry generally operates by transferring the financial risk from the customer to the insurer.

Insurance and Court: Do Judges Verify Your Coverage?

You may want to see also

Explore related products

![]()

Claims are paid after an adjuster inspects the damage and offers a sum for repairs

When it comes to insurance claims, the process typically involves an adjuster inspecting the damage and offering a monetary sum for repairs. This is based on the specific terms and limits outlined in the insurance policy of the claimant. The adjuster's role is to determine the appropriate compensation for the loss incurred, which may include damage to property, personal injury, or both.

Upon assessing the damage, the adjuster will consider various factors, such as the extent of the damage, the policy's coverage, and any applicable deductibles. They may also interview the claimant and witnesses, review relevant documents, and consult with experts, such as accountants, architects, or engineers, to ensure an accurate evaluation of the claim.

Once the adjuster has completed their assessment, they will offer a settlement amount to the claimant. It is important to note that the initial payment received is often an advance against the total settlement and not the final payment. This means that if additional damage is discovered later, the claimant can reopen the claim and file for an additional amount.

In cases where both the structure of the home and personal belongings are damaged, insurance companies typically provide separate checks for each category of damage. Moreover, if the home is deemed uninhabitable during repairs, the claimant may receive a separate check for additional living expenses (ALE) incurred.

It is worth mentioning that if there is a mortgage on the property, the check for repairs is usually addressed to both the homeowner and the mortgage lender. Lenders often require that they be named in the homeowner's policy and be included in any insurance payments related to the property's structure. In some instances, the lender may place the funds in an escrow account, releasing payments as the repair work progresses.

Wellness Checks: Insurance's Vital Health Screening

You may want to see also

Frequently asked questions

An insurance premium is the amount of money an individual or business pays for an insurance policy.

Premiums are often paid monthly, quarterly, or annually, depending on the policy. Some insurers allow the policyholder to pay the insurance premium in instalments, while others may require an upfront payment for the full year before any coverage starts.

Insurance premiums are not always fixed and can vary depending on the type of insurance and the factors that affect the premium. For example, the premium for property insurance for a factory building is a fixed cost when the independent variable is the number of units produced within the factory.

The main factors in determining automobile insurance premiums include your driving record, your geographic location, how often you use your car, the type of car(s) being insured, your gender, your credit record, and your age.

The major factors that affect life insurance premiums are the insured's risk of mortality, the interest the insurance company expects to earn by investing your premium, and the expenses it will incur. The age at which you begin coverage will determine your premium amount, along with other risk factors such as your current health.