Texas Mutual Insurance offers workers' compensation insurance to businesses, protecting them from fluctuations and changes throughout the year. The company requires employers to report payroll, which can be done online, to ensure that they are paying the right amount for coverage. While there is no explicit mention of 1099 reporting, Texas Mutual does refer to 1099 workers and businesses in their payroll reporting requirements. Additionally, the State of Texas has outlined specific procedures for 1099 reporting, indicating that payments to non-corporate payees exceeding $600 during a calendar year must be reported to the IRS using Form 1099-MISC. Given the context of payroll reporting and the specific mention of 1099 workers, it is likely that payments to Texas Mutual Insurance may be subject to 1099 reporting requirements, particularly if certain conditions, such as payment amounts and recipient types, are met.

| Characteristics | Values |

|---|---|

| Payments to Texas Mutual Insurance reportable on Form 1099-MISC | Payments to non-corporate payees totaling $600 or more for services or interest during a calendar year |

| Payments to corporations reportable on Form 1099 | Legal and medical services |

| Payments not reportable on Form 1099-MISC | Payments made with a credit card by State of Texas agencies and institutions of higher education |

| Payments reportable on Form 1099-NEC | Payments of at least $600 for services performed by someone who is not an employee, including parts and materials; cash payments for fish or other aquatic life purchased from someone in the trade or business of catching fish |

| Payments reportable on Form 1099-INT | Interest on a business debt to someone (excluding interest on an obligation issued by an individual) |

| Payments reportable on Form 1099-DIV | Dividends or other distributions to a company shareholder |

| Payments reportable on Form 1099-R | Distribution from a retirement or profit plan, or from an IRA or insurance contract |

| Payments reportable on Form 1099-K | Payments to merchants or other entities in settlement of reportable payment transactions, including payment card or third-party network transactions |

| Payments reportable on Form 1099-S | Sale or exchange of real estate |

| Payments reportable on Form 1099-B | Sale of a covered security belonging to a customer by a broker |

| Payments reportable on Form 1099-A | Release of someone from paying a debt secured by property or abandonment of property subject to the debt |

| Payments reportable on Form 1099-C | Forgiveness of a debt |

| Payments reportable on Form 1099-MISC | Direct sales of at least $5,000 of consumer products to a buyer for resale anywhere other than a permanent retail establishment |

Explore related products

What You'll Learn

![]()

Reporting payments to non-corporate payees

Identifying Reportable Payments

Not all payments to non-corporate payees are reportable. Generally, you must report a payment as non-employee compensation if the following conditions are met:

- The payment is made to someone who is not your employee (an independent contractor, freelancer, or non-resident alien, for example).

- The payment is made for services rendered in the course of your trade or business, including payments to government agencies and nonprofit organizations.

- The payment is made to an individual, partnership, estate, or, in some cases, a corporation.

- The total payments to the payee amount to $600 or more during the calendar year.

Forms for Reporting Non-Corporate Payee Payments

The specific form used to report payments to non-corporate payees depends on the circumstances:

- Form 1099-NEC (Nonemployee Compensation): This form is generally used to report payments of $600 or more made to non-corporate payees, including independent contractors and freelancers, for services provided in the course of your business. It is used for U.S. citizens and resident aliens.

- Form 1042-S (Foreign Persons' U.S. Source Income Subject to Withholding): This form is used for reporting payments to non-resident aliens. Withholding requirements may apply to these payments, and Form 1042-T is used to transmit paper Forms 1042-S to the IRS. Non-resident aliens may qualify for exemption from withholding by providing a U.S. Social Security Number or Individual Taxpayer Identification Number, having a tax treaty with the U.S., and not exceeding the maximum allowable days in the country.

- Form 1099-MISC: While primarily used for miscellaneous income, this form may be relevant for reporting payments to non-corporate payees in specific situations, such as legal and medical services provided by corporations.

Additional Considerations

It's important to note that payments made with a credit card or payment card may not need to be reported by the payer, as the payment settlement entity, such as Citibank N.A., is generally responsible for reporting such transactions on Form 1099-K. Additionally, certain payments, such as those for research participants or occasional services unrelated to regular employment, may have unique reporting requirements.

For assistance with specific scenarios and complex tax issues, it is recommended to consult the IRS directly or seek professional tax advice.

Home Insurance: What Counts as Accidental Damage?

You may want to see also

Explore related products

![]()

Reporting payments to corporations

Generally, payments to corporations do not need to be reported. However, there are several exceptions to this rule. If the following four conditions are met, you must report a payment as nonemployee compensation:

- The payment was made to someone who is not your employee

- The payment was made for services in the course of your trade or business, including government agencies and nonprofit organizations

- The payment was made to an individual, partnership, estate, or, in some cases, a corporation

- The payment(s) to a non-corporate payee totalled $600 or more during a calendar year

In this case, you must report the payment(s) to the Internal Revenue Service (IRS) on a Form 1099-NEC, Nonemployee Compensation, or Form 1099-MISC. For nonemployee compensation paid to nonresident aliens, Form 1042-S, Foreign Persons' U.S. Source Income Subject to Withholding, is required.

There are other instances where payments to corporations are reportable on Form 1099-MISC. These include:

- Medical and healthcare payments of $600 or more made to a corporation in the course of your trade or business

- Attorneys' fees, including gross proceeds paid to an attorney

- Substitute payments in lieu of dividends or tax-exempt interest of $10 or more

- Payments made by a federal executive agency to a corporation for services

It is important to note that the term "corporation" includes both S and C corporations, as well as limited liability companies (LLCs) that have elected to be taxed as a corporation with the IRS.

Assessing Home Value for Insurance

You may want to see also

Explore related products

![]()

Reporting payments to attorneys

There are multiple types of Form 1099, and the specific form used to report payments to attorneys depends on the nature of the payment. Form 1099-NEC is used to report payments made to attorneys for services rendered directly to the payor. This form is used when the attorney is providing legal services to the business, such as drafting contracts or collecting fees. Form 1099-NEC is also used when a business makes a settlement payment to a claimant's lawyer. In this case, the payment must be made in connection with the trade or business of the payor, and the payment must be at least $600.

Form 1099-MISC is a catch-all form for various types of payments, including legal payments when the attorney is not the payee's lawyer. This form is used when a business pays damages or settlement proceeds to the lawyer of an injured party. Form 1099-MISC also includes a box specifically for "Gross proceeds to an attorney," where settlement payments are reported. It's important to note that not all legal disputes will require the issuance of Form 1099, as damages or settlements for physical injuries are not taxable and, therefore, do not need to be reported.

Attorneys are also required to report payments made to other attorneys. This ensures that all legal fees are appropriately disclosed and taxed. The specific form used for this reporting depends on the nature of the payment and the relationship between the attorneys.

Unraveling the Mystery of Farmers Insurance: A Comprehensive Guide to Interview Questions

You may want to see also

Explore related products

![]()

Reporting payments to employees vs non-employees

Reporting payments to employees and non-employees is an essential aspect of financial compliance for businesses. In the United States, these payments are typically reported using specific forms, such as Form 1099 for non-employees and Form W-2 for employees. Let's delve into the details of reporting payments to these two distinct categories.

Reporting Payments to Employees

Reporting payments to employees is a standard procedure for businesses. Employers are generally required to report wages, tips, and other forms of compensation paid to their employees. This is typically done by filing forms with the Internal Revenue Service (IRS). The specific form used for this purpose is Form W-2, also known as the Wage and Tax Statement. Form W-2 must be furnished to employees and filed with the Social Security Administration (SSA) by January 31 of each year. It is important to note that employers are also responsible for withholding and depositing federal income tax, as well as Social Security and Medicare taxes, on behalf of their employees.

Additionally, employers need to file quarterly reports, such as Form 941, which is the Employer's Quarterly Federal Tax Return. This form includes withholding on sick pay and supplemental unemployment benefits. Other quarterly forms may include Form 943 for agricultural employees and Form 944, depending on the deposit schedule determined by the employer. At the end of the year, employers must also complete Form 940, the Employer's Annual Federal Unemployment (FUTA) Tax Return, to report their FUTA taxes. These forms help ensure compliance with employment tax regulations.

Reporting Payments to Non-Employees

Reporting payments to non-employees, such as independent contractors or non-resident aliens, is equally important. If certain conditions are met, payments to non-employees must generally be reported as nonemployee compensation. These conditions include making a payment to someone who is not your employee, for services provided in the course of your trade or business, and meeting a minimum payment threshold. The current threshold is $600 during the year. Form 1099-NEC, Nonemployee Compensation, is used to report these payments.

It is important to note that nonemployee compensation paid to nonresident aliens may require additional reporting on Form 1042-S, Foreign Persons' U.S. Source Income Subject to Withholding. This form is transmitted to the IRS using Form 1042-T, and Form 1042 may also need to be filed. For non-corporate payees, Form 1099-MISC, Miscellaneous Income, is used if the payments for services or interest total at least $600 during the calendar year. However, payments to corporations are generally not reportable, except for legal and medical services, which are reportable to the IRS.

In summary, reporting payments to employees and non-employees involves distinct procedures and forms. While Form W-2 and related forms are used for employees, Form 1099-NEC and other variations are used for non-employee compensation reporting. Businesses must stay compliant with these reporting requirements to maintain accurate financial records and meet their tax obligations.

Farmers Insurance and Unsolicited Calls: Why Your Phone May Be Ringing

You may want to see also

Explore related products

![]()

Reporting payments for services

If you pay independent contractors, you may need to file a Form 1099 to report these payments for services. Form 1099 is used to report payments for services performed for your trade or business. This includes payments to individuals, partnerships, estates, or corporations. Generally, payments to corporations are not reportable, except for legal and medical services, which must be reported to the IRS.

If you pay a non-employee $600 or more for services during a calendar year, you must report the payment to the IRS using Form 1099-MISC or Form 1099-NEC, Nonemployee Compensation. This form has replaced the previous requirement to report nonemployee compensation in box 7 of Form 1099-MISC. Nonemployee compensation paid to nonresident aliens is reported on Form 1042-S, with a Form 1042-T used to transmit paper forms to the IRS.

Form 1099-K is used to report payments from payment apps, online marketplaces, and credit, debit, or stored-value cards. Payment processors, including PayPal, are required to report to the IRS about customers who receive payments for the sale of goods and services above a certain threshold. This threshold has changed over time, with the current threshold being $600 in gross sales from goods or services in a calendar year. This threshold is expected to change to \$2,500 for the 2025 tax year and \$600 for the 2026 tax year.

State agencies and institutions of higher education are not required to issue Form 1099-MISC for payments made with a credit card; instead, Citibank N.A. is responsible for reporting these credit card payments via Form 1099-K.

Understanding Farmers Insurance for Planting: A Guide to Agricultural Coverage

You may want to see also

Frequently asked questions

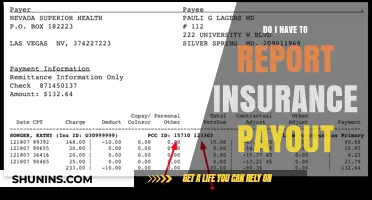

A 1099 form is a USAS-generated form used to report payments to non-corporate payees.

Payments to Texas Mutual Insurance are not explicitly mentioned as being reportable on a 1099 form. However, Texas Mutual Insurance requires employers to report payroll and submit claims, which may involve reporting payments on a 1099 form.

For assistance with USAS-generated 1099 forms and reports, you can contact the 1099 helpline at (512) 463-6307. If you have specific questions about the reportability of payments, you can contact the Internal Revenue Service (IRS) at (866) 455-7438.