FHA loans are the most popular loan type in America for first-time homebuyers. They are guaranteed by the government and require mortgage insurance, which protects lenders from losing money if the borrower defaults on the loan. This insurance comes in the form of a mortgage insurance premium (MIP) and is paid upfront and annually. Unlike private mortgage insurance (PMI), FHA MIP is not cancelled when the borrower reaches a certain home equity percentage. FHA loans are distinct from conventional loans, which are not government-insured and require PMI unless the borrower makes a specific, lender-prescribed percentage down payment.

| Characteristics | Values |

|---|---|

| FHA loans require mortgage insurance | Yes |

| Private mortgage insurance required | No, but FHA loans require an Up Front Mortgage Insurance Premium and MIP instead |

| FHA mortgage insurance premium (MIP) | An additional payment to secure the mortgage loan |

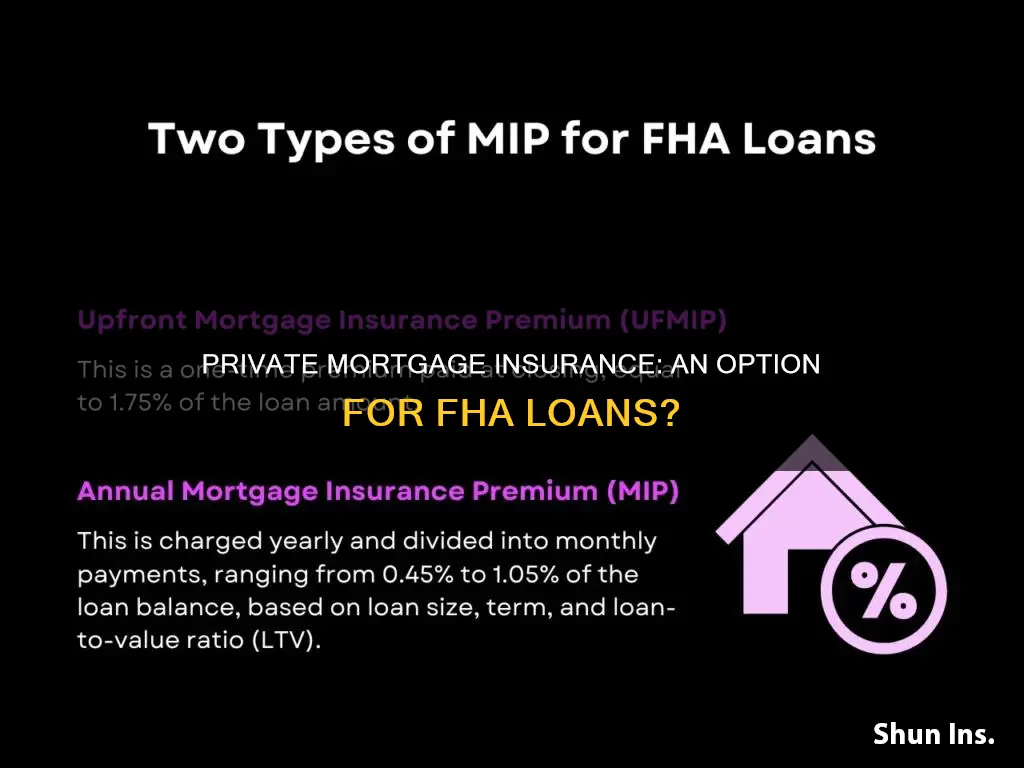

| FHA upfront mortgage insurance premium | 1.75% of the loan amount |

| FHA annual MIP | Varies based on the size, term and loan-to-value (LTV) ratio of the loan |

| FHA loans require both upfront and annual mortgage insurance premiums | Yes |

| FHA mortgage insurance is a government guarantee | Yes |

Explore related products

What You'll Learn

![]()

FHA mortgage insurance premium (MIP)

FHA loans are a popular option for first-time homebuyers due to their low down payment requirements. However, these loans come with mortgage insurance requirements to protect lenders against losses from borrower defaults. This insurance, known as FHA Mortgage Insurance Premium (MIP), is mandatory for all FHA borrowers, regardless of their down payment amount or credit score.

The FHA MIP involves two payments: an upfront premium and an annual premium. The upfront mortgage insurance premium (UFMIP) is typically 1.75% of the total loan value, paid as a lump sum or financed into the mortgage. This upfront cost is not refundable unless the borrower replaces their FHA loan with another FHA loan. The annual mortgage insurance premium (MIP) is charged monthly, with the premium amount divided by 12 and added to the borrower's monthly mortgage payments. The annual MIP ranges from 15 to 75 basis points (0.15% to 0.75%) of the loan amount.

The cost of FHA MIP depends on various factors, including the loan amount, loan term, and loan purpose. For loans greater than $726,200 with a Loan to Value (LTV) ratio greater than 90% and a term of up to 15 years, the annual MIP is reduced to 65 basis points. Borrowers with FHA loans originated before June 3, 2013, may be eligible for MIP removal when their loan balance reaches 78% LTV.

While FHA MIP provides protection for lenders, it also benefits borrowers by allowing them to secure a mortgage with a lower down payment. Without MIP, lenders would typically require a much larger down payment. Borrowers who wish to remove or reduce their MIP payments can consider refinancing their FHA loan into a conventional loan or exploring options like an FHA Streamline Refinance.

In summary, FHA Mortgage Insurance Premium (MIP) is an essential component of FHA loans, providing protection for lenders and facilitating homeownership for borrowers with lower down payments. Borrowers should carefully consider the costs and benefits of FHA MIP when deciding on a suitable loan option.

Redundancy Insurance: Is It a Worthy Investment?

You may want to see also

Explore related products

$13.25

![]()

FHA loans require upfront mortgage insurance

FHA loans are a popular option for first-time homebuyers due to their low down payment options. However, these loans come with specific requirements, including the necessity for mortgage insurance. This insurance is designed to protect lenders in the event of borrower default.

FHA loans require both upfront and annual mortgage insurance payments, known as Mortgage Insurance Premium (MIP). The upfront MIP payment is typically 1.75% of the total loan value, paid as a lump sum or added to the loan balance. For instance, a $150,000 loan would require an upfront MIP of $2,500. This payment is due when the loan is closed or during refinancing, and it is non-refundable unless the borrower switches to another FHA loan.

The annual MIP payment is divided into 12 monthly installments, with the amount based on the loan size and down payment. A larger down payment can help reduce the annual MIP cost. It's important to note that FHA loans do not cancel MIP payments once a certain home equity percentage is reached, unlike conventional loans with private mortgage insurance (PMI).

The requirement for upfront and annual MIP payments on FHA loans adds to the overall cost of borrowing. Borrowers should carefully consider their financial situation and explore alternative loan options, such as conventional loans or VA loans, which may offer different insurance requirements and cost structures.

While FHA loans mandate MIP, it offers benefits to homebuyers. Without MIP, lenders would typically demand a much larger down payment. MIP allows homebuyers to secure a mortgage with a lower down payment, making homeownership more accessible.

Insuring Your Home: Market Value or Not?

You may want to see also

Explore related products

![]()

Annual mortgage insurance premiums

FHA loans require both upfront and annual mortgage insurance premiums. The Federal Housing Administration (FHA) requires mortgage insurance to guarantee a lender's losses if a homeowner defaults on an FHA loan. The insurance covers FHA-approved lenders and FHA loans on single-family homes, multifamily properties, manufactured homes, condos, and co-ops.

The annual mortgage insurance premium (MIP) is charged annually based on the following factors: the premium amount, the loan term, the loan amount, and the loan purpose. The premium is divided by 12 and charged in monthly installments that are added to your monthly mortgage payment. The cost of annual MIP ranges between 15 and 75 basis points, which is 0.15% to 0.75% of your loan amount. The monthly premium is the same regardless of your credit score.

The amount of time FHA borrowers will need to pay MIP depends on the down payment. With a 10% or larger down payment on an FHA loan, you'll pay MIP for the first 11 years. With less than 10%, MIP lasts the entire loan term. You can't cancel MIP payments on an FHA loan, but you can lower your payment by making a larger down payment.

Understanding Eligibility for High Net Worth Insurance

You may want to see also

Explore related products

![]()

FHA loans are guaranteed with government funds

FHA loans are a popular option for first-time homebuyers due to their low down payment options. They are guaranteed by the Federal Housing Administration (FHA), a government agency created in 1934 during the Great Depression. At that time, the housing industry faced high default and foreclosure rates, and only one in ten households owned their homes.

The FHA was established to reduce the risk to lenders and make it easier for borrowers to qualify for home loans. By guaranteeing or insuring the loan, the FHA ensures that the lender does not bear the default risk, making it more likely for borrowers to get approved. This guarantee is funded by the government and protects lenders against losses resulting from defaults on home mortgages.

FHA loans require borrowers to pay a mortgage insurance premium (MIP) to secure the mortgage loan. This insurance premium is paid upfront and annually, with the upfront payment typically financed into the mortgage amount. The upfront MIP is equal to 1.75% of the total loan value, while the annual MIP is charged monthly based on factors such as the loan amount, loan term, and the home's loan-to-value ratio. These MIP payments provide protection for lenders in case of borrower default and are beneficial to homebuyers as they reduce the required down payment amount.

While FHA loans offer advantages, it is important to note that the mortgage insurance requirement can make them more expensive than conventional loans. Additionally, FHA loans have specific criteria, including credit score requirements, and may not be suitable for all borrowers. However, they have helped increase homeownership rates, and potential homebuyers should explore their options to determine if an FHA loan aligns with their financial goals and qualifications.

Balance Protection Insurance: Worth the Cost?

You may want to see also

Explore related products

$6.99

![]()

FHA mortgage insurance is more expensive than private mortgage insurance

FHA loans are an attractive option for many first-time homebuyers due to their low down payment requirements. However, one of the drawbacks of FHA loans is the requirement for mortgage insurance, which can be more expensive than private mortgage insurance (PMI).

FHA loans require borrowers to pay a mortgage insurance premium (MIP) to protect lenders against losses in the event of default. This insurance consists of two parts: an upfront premium and an annual premium. The upfront premium is typically 1.75% of the loan amount, which can be paid in cash or financed into the mortgage. The annual premium varies based on factors such as loan size, term, and loan-to-value ratio, and it is paid in monthly installments along with the mortgage payment.

On the other hand, conventional loans typically require PMI when the down payment is less than 20%. PMI can be cancelled once the borrower reaches a certain level of equity in their home, usually 20% to 78%. FHA mortgage insurance, however, cannot be cancelled unless the borrower refinances into a non-FHA loan.

The higher cost of FHA mortgage insurance compared to PMI is a significant consideration for borrowers. While FHA loans offer advantages for first-time homebuyers, the ongoing expense of mortgage insurance can add up over time. Borrowers with higher credit scores may find that PMI is a more cost-effective option, as FHA monthly payments are lower for borrowers with credit scores under 720.

It's important to note that FHA loans have specific requirements and limitations, and borrowers should carefully consider their options before deciding on a loan type. Down payment assistance programs and other loan types, such as VA or USDA loans, may offer alternatives to FHA loans and their associated mortgage insurance costs.

Report Traffic Incidents: What to Tell Your Insurance Company

You may want to see also

Frequently asked questions

FHA loans are mortgages insured by the Federal Housing Administration. They are the most common loan type in America for first-time homebuyers.

Private mortgage insurance (PMI) is a type of insurance that protects lenders against losses that result from defaults on home mortgages. It is required for conventional loans when the down payment is below 20%.

No, FHA loans do not require PMI. However, they do require an Upfront Mortgage Insurance Premium (UFMIP) and a Mortgage Insurance Premium (MIP) to be paid instead.

The upfront premium is 1.75% of the loan amount. The annual premium varies based on the size, term and loan-to-value (LTV) ratio of the loan.

You can pay the upfront premium in a lump sum or include it in your FHA closing costs. The annual premium is paid in monthly installments that are added to your mortgage payments.