Private mortgage insurance (PMI) is an additional expense for conventional mortgage borrowers who make a down payment of less than 20%. Although paid for by the borrower, PMI protects the lender in the event that the borrower defaults on their loan. The cost of PMI depends on several factors, including the size of the loan, the down payment amount, the type of mortgage, and the borrower's credit score. PMI can be cancelled once the mortgage balance reaches 78% of the original value of the home, or the borrower may request cancellation once the balance reaches 80%.

| Characteristics | Values |

|---|---|

| What is it? | Private Mortgage Insurance (PMI) is a type of insurance policy that protects the lender if a borrower defaults on a home loan. |

| Who does it protect? | PMI protects the lender, not the borrower. |

| When is it required? | PMI is required when homebuyers make down payments of less than 20% of the home's value. |

| How much does it cost? | The cost of PMI depends on factors such as the size of the mortgage loan, the down payment amount, credit score, and type of mortgage. The average monthly cost is 0.46% to 1.5% of the loan amount. |

| How is it paid? | PMI is usually paid as part of the monthly mortgage payment, but some lenders may allow upfront or a combination of upfront and monthly payments. |

| Can it be cancelled? | PMI can be cancelled once the mortgage balance reaches 78%-80% of the original value of the home. Borrowers may need to submit a request in writing and get a home appraisal. |

| Are there alternatives? | Yes, there are government-backed loan options such as FHA, USDA, and VA loans that do not require PMI but have their own associated fees. |

Explore related products

What You'll Learn

![]()

Private mortgage insurance (PMI)

The cost of PMI depends on several factors, including the size of the loan, the down payment amount, and the borrower's credit score. Those with a higher credit score will pay less for PMI than those with a lower score. PMI can be paid in different ways, including a one-time upfront premium, monthly premiums, or a combination of both. The monthly premium is added to your monthly mortgage payment.

PMI can help borrowers qualify for a loan they might not otherwise be able to get. It is not required for all types of mortgages and can be avoided by making a larger down payment of 20% or more. Lenders are required to cancel PMI when the mortgage balance reaches 78% of the home's original value or once the borrower is halfway through the loan term, whichever comes first.

To determine if you have PMI, check your Loan Estimate and Closing Disclosure documents, where the PMI premium should be listed. Lenders may offer different PMI options, so it is important to ask about the total costs and compare different choices to find the best deal.

Prescription Insurance: Is It a Worthy Investment?

You may want to see also

Explore related products

$11.01 $17.99

![]()

PMI cost

Private mortgage insurance (PMI) is often required for homebuyers who pay less than 20% upfront on a conventional loan. The insurance covers the lender in the event that the buyer defaults on the loan. The cost of PMI depends on several factors, including the size of the loan, the down payment amount, the debt-to-income ratio, credit score, and loan type.

The average cost of PMI for a conventional home loan ranges from 0.46% to 1.50% of the original loan amount per year, according to the Urban Institute's Housing Finance Policy Center. However, PMI rates can vary from 0.2% to 2% of the loan amount per year, depending on the specific circumstances of the borrower. For example, a higher credit score and a larger down payment will typically result in a lower PMI rate. Conversely, borrowers with low credit scores, high debt-to-income ratios, and smaller down payments will usually pay higher PMI rates.

PMI is typically paid as part of the total loan payment, which includes the mortgage principal, interest, and taxes. While it is an added expense, some borrowers find it worthwhile as it enables them to buy a house sooner. Additionally, PMI can be cancelled once the loan balance reaches a certain threshold or a certain percentage of the loan has been paid off.

There are PMI calculators available online, such as those provided by NerdWallet and Intuit Credit Karma, which can help borrowers estimate their potential PMI costs based on their individual circumstances.

Insurance Bad Faith: California's Guide to Reporting

You may want to see also

Explore related products

![]()

Cancelling PMI

Private Mortgage Insurance (PMI) is an additional monthly cost that is added to your conventional loan if you bought a home with less than 20% down payment. It is not forever and can be removed from your monthly payments in two ways: when you pay your loan balance down below 80% of the purchase price of your home, or once you have achieved 20% equity in your home.

To cancel PMI, you must submit a written request to your mortgage servicer. You can make this request ahead of the scheduled date if you have made additional payments that reduce the principal balance of your mortgage to 80% of the original value of your home. This original value is either the contract sales price or the appraised value of your home at the time of purchase, whichever is lower. If you have refinanced, the original value is the appraised value at the time of refinancing.

Your servicer is legally required to grant your request as long as you meet the criteria. You must be able to provide evidence (for example, an appraisal) that the value of your property hasn't declined below the original value of the home. You must also be current on your payments. If you are not, PMI will not be terminated until your payments are brought up to date.

Your lender or servicer must end the PMI the month after you reach the midpoint of your loan's amortization schedule. This is true even if the principal balance has not reached 78% of the original value of your home. For 30-year loans, the midpoint is after 15 years.

Strategies to Remove Mortgage Insurance

You may want to see also

Explore related products

![]()

Conventional loans

Private mortgage insurance (PMI) is a type of insurance that is usually required for conventional loans when the buyer makes a down payment of less than 20% of the home's value. PMI is designed to protect the lender, not the borrower, in the event that the buyer defaults on their mortgage payments. It is an additional monthly cost that is rolled into the mortgage payment. The amount paid for PMI depends on the loan and down payment size, the type of mortgage, and the borrower's credit score.

Lenders consider low down payments to be a greater risk, and PMI provides financial protection for them should they have to foreclose on the home. While PMI can increase the cost of a loan, it can also help borrowers qualify for loans that they may not otherwise be able to obtain. Borrowers with smaller amounts of available cash can purchase a home without paying costly PMI by taking out a conventional loan with a higher interest rate.

There are two types of PMI: borrower-paid and lender-paid. With borrower-paid PMI, the borrower's insurance payment is added to their monthly mortgage payment. Borrowers may also have the option to pay PMI upfront or through a combination of upfront and monthly payments. Lender-paid PMI, also known as a no-PMI loan, is paid by the lender in a lump sum, and the borrower repays it through a higher interest rate on the loan. This type of PMI cannot be cancelled in the same way as borrower-paid PMI and is generally more expensive in the long run.

PMI is not permanent and can be removed from monthly payments once the loan balance reaches 78-80% of the home's original value or when the borrower has achieved 20% equity in the home. To request PMI cancellation, borrowers must be current on their mortgage payments, and an appraisal must verify the current property value.

It is important to note that PMI is different from homeowners insurance, which provides financial protection against damages to the home. Homeowners insurance is typically required for any type of mortgage. When considering a conventional loan, borrowers should carefully review the terms and conditions, including the requirement for PMI, to ensure they understand their financial obligations.

The Catchy Rhythm of Insurance: Exploring the BPM of Farmers Insurance Jingle

You may want to see also

Explore related products

![]()

Alternative loans

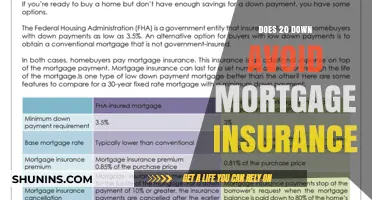

Private mortgage insurance (PMI) is a type of mortgage insurance that you may be required to buy if you take out a conventional loan with a down payment of less than 20% of the purchase price. PMI rates vary depending on the down payment amount, credit score, loan type, and mortgage type. While PMI can help you qualify for a loan that you might not otherwise be able to get, it increases the cost of your loan.

- Save for a 20% down payment: If you can save enough for a 20% down payment, you can avoid paying PMI on a conventional loan. This option may take time but can result in lower overall costs and a lower interest rate.

- Federal Housing Administration (FHA) loan: FHA loans are insured by the government and do not require PMI. Instead, FHA loans have their own form of mortgage insurance, which is required for all FHA loans. FHA mortgage insurance costs the same regardless of your credit score, with a slight increase for down payments less than 5%. However, FHA loans may have higher interest rates and could be more expensive in the long run.

- U.S. Department of Agriculture (USDA) loan: USDA loans are similar to FHA loans but are typically cheaper. Like FHA loans, USDA loans require mortgage insurance, which is paid at closing and as part of your monthly payment.

- Department of Veterans' Affairs (VA)-backed loan: If you are a servicemember, veteran, or family member, you may be eligible for a VA-backed loan. With this option, the VA guarantee replaces mortgage insurance, and there is no monthly mortgage insurance premium. However, you will need to pay an upfront "funding fee," which can be rolled into your mortgage.

- "Piggyback" second mortgage: As an alternative to PMI, some lenders may offer a "piggyback" second mortgage. This option may be marketed as cheaper, but it's important to compare the total costs before deciding.

When considering alternative loans, it's important to evaluate your financial situation and seek professional advice. Each loan type has its own requirements, costs, and benefits, and choosing the right option will depend on your specific circumstances.

Insuring Your Irish Home: Valuation Factors

You may want to see also

Frequently asked questions

Private mortgage insurance, or PMI, is a type of insurance policy that protects only the lender, not the borrower, if the borrower defaults on a home loan.

You will need to pay for PMI if you have a conventional loan and put down less than 20% when purchasing a home, or have less than 20% equity when refinancing.

The cost of PMI depends on several factors, including the size of the mortgage loan, the down payment amount, your credit score, and the type of mortgage. The more you borrow and the lower your credit score, the more you will pay for PMI.