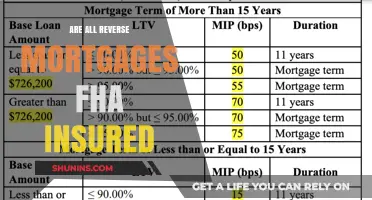

A finance charge is the total amount paid to a lender for borrowing money, including interest and other fees. Finance charges are a form of compensation to the lender for providing funds or extending credit. Mortgage lenders are required to disclose their finance charges and how these are calculated. Finance charges can include interest rates, application fees, discount points, and mortgage insurance. However, charges imposed by third-party closing agents, such as attorneys or escrow and title companies, are typically excluded from the finance charge. Mortgage insurance premiums and other finance charges are sometimes paid at or before consummation or settlement on the borrower's behalf by a non-creditor seller.

| Characteristics | Values |

|---|---|

| Definition | A finance charge is the total amount you pay a lender for borrowing money, including interest and other fees. |

| Calculation | Finance charges are calculated each billing cycle based on the current base rate that banks charge their most creditworthy customers. |

| Components | Interest, application fee, discount points, mortgage insurance, and more. |

| Exclusions | Charges imposed by third-party closing agents such as settlement agents, attorneys, and escrow and title companies. |

| Fluctuations | Finance charges may change monthly if the rate is not fixed. |

| Disclosure | Lenders are required to disclose their finance charges and how these charges are calculated. |

| Regulation | The Truth in Lending Act requires the disclosure of all interest rates, standard fees, and penalty fees. |

Explore related products

What You'll Learn

![]()

Mortgage insurance premiums are finance charges

A finance charge is the total amount of interest and loan charges paid by a borrower over the entire life of a mortgage loan. It is the cost a borrower pays for using a mortgage, personal loan, auto loan, or credit card. Mortgage lenders are required to disclose their finance charges and how these charges are calculated.

Finance charges are a form of compensation to the lender for providing funds or extending credit to a borrower. These charges can include one-time fees, such as an origination fee on a loan, or interest payments, which can be amortized on a monthly or daily basis. Finance charges can vary from product to product or lender to lender. There is no single formula for determining the interest rate to be charged.

Mortgage insurance is included in the finance charge. The finance charge can be found on page 5 of the Closing Disclosure form in the "Loan Calculations" section. The financial fee is a broad term that can include many different fees, including interest. Mortgages have lower interest rates because the debt is secured.

Exposing Unethical Blue Cross Insurance Representatives: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Mortgage lenders must disclose finance charges

A finance charge is the total amount of interest and loan charges you pay over the entire life of a mortgage loan. This includes all prepaid loan charges, such as interest, discount points, mortgage insurance, and other fees. Finance charges are calculated each billing cycle based on the current base rate that banks offer their most creditworthy customers. This rate can fluctuate based on market conditions and the Federal Reserve's monetary policy, so financial fees may change monthly if your rate is not fixed.

Certain fees are excluded from the finance charge. For example, a lump sum charged for conducting or attending a closing (e.g., by a lawyer or title company) is excluded if the charge is primarily for services related to reviewing or completing documents. Additionally, charges imposed solely in connection with the initial decision to grant credit, such as fees for tax lien searches or flood insurance requirements, are excluded.

On the other hand, buyer's points (fees charged to the buyer by the creditor) are considered finance charges. Mortgage insurance premiums and other finance charges may be paid at or before consummation or settlement on the borrower's behalf by a non-creditor seller.

It's important to note that financial expenses are costs you would not typically incur if you paid in cash instead of credit. These expenses can add up and affect your overall financial well-being, so it's essential to stay informed and make careful decisions when taking out a mortgage loan.

Colonial Penn Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Finance charges include interest and fees

A finance charge is the total amount of interest and fees that you pay a lender for borrowing money. This includes interest and other fees, such as account maintenance fees or late fees. Finance charges are usually calculated each billing cycle based on the current base rate that banks charge their most creditworthy customers. This rate can fluctuate based on market conditions and the Federal Reserve's monetary policy, so finance charges may change monthly if your rate is not fixed.

Finance charges are subject to government regulation. The federal Truth in Lending Act requires that all interest rates, standard fees, and penalty fees must be disclosed to the consumer. Additionally, the Credit Card Accountability Responsibility and Disclosure (CARD) Act of 2009 mandated a minimum 21-day grace period before interest charges can be assessed on new purchases.

For mortgages, finance charges include interest, discount points, and mortgage insurance. These charges are calculated over the entire life of the mortgage loan, assuming the loan is kept through the full term until it matures. Mortgage interest rates are typically lower than other types of loans because the debt is secured—if someone defaults on their mortgage, the bank can become the owner of the house.

It's important to carefully review the contract to understand all the fees being charged and whether there are any penalties for early repayment. By paying off a loan early, it may be possible to save on finance costs.

Burial Insurance: Seniors' Peace of Mind

You may want to see also

Explore related products

![]()

Finance charges vary by loan type and lender

Finance charges refer to the total amount paid to a lender for borrowing money, including interest and other fees. These charges vary depending on the type of loan and the lender. For instance, mortgage loans often have lower interest rates than unsecured loans, such as credit cards, due to the lower risk associated with the loan being backed by an asset.

The specific terms and conditions set by each lender can result in different finance charges for similar loans. For example, a customer may qualify for two similar products from different lenders, but each product could have a different set of finance charges. These charges can include interest rates, origination fees, transaction fees, maintenance fees, and other fees. Understanding these charges is crucial for borrowers, as they can significantly impact the overall cost of a loan.

The Truth in Lending Act requires lenders to disclose all interest rates, standard fees, and penalty fees to consumers. However, it's important to note that finance charges do not include certain fees, such as those for conducting or attending a closing, which are primarily for services related to reviewing or completing documents.

Additionally, mortgage insurance premiums and other finance charges may be paid on behalf of the borrower by a non-creditor seller, in which case they are excluded from the finance charge. It's important for borrowers to carefully review the loan agreement and disclosures to understand the specific finance charges associated with their loan.

Finance charges can be either a flat fee or a percentage of the amount borrowed. Percentage-based charges are common in credit cards and large loans, such as mortgages or auto loans. The interest rate, expressed as an annual percentage rate (APR), is a percentage of the loan amount charged by the lender for borrowing funds. This rate is based on the outstanding balance of the loan and can fluctuate based on market conditions and the borrower's payment history.

Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Finance charges are compensation for lenders

A finance charge is a fee charged for the use of credit or the extension of existing credit. It is the total amount paid to a lender for borrowing money, including interest and other fees. Finance charges compensate lenders for providing funds or extending credit, allowing them to make a profit on the use of their money.

Finance charges can take different forms depending on the loan product and lender. Some common types of finance charges include interest payments, origination fees, transaction fees, and maintenance fees. Interest payments are typically expressed as an annual percentage rate (APR) and represent the cost of borrowing money. Origination fees are one-time charges that cover the processing and initiation of the loan. Transaction fees are associated with specific transactions, such as cash advances or balance transfers. Maintenance fees include annual or monthly service fees related to maintaining the loan account.

In the context of mortgages, finance charges can include interest, discount points, and mortgage insurance. These charges are calculated based on the current base rate that banks offer to their most creditworthy customers and can fluctuate with market conditions and monetary policies. Mortgages often have lower interest rates compared to other forms of credit because they are secured by the underlying asset, reducing the risk for the lender.

It is important to note that finance charges are regulated in many countries to prevent excessive or predatory lending practices. The Truth in Lending Act requires lenders to disclose all interest rates, standard fees, and penalty fees to consumers. Borrowers should carefully review loan agreements and disclosures to understand the specific finance charges associated with their loans and make informed decisions.

Cheap Insurance: Worth the Risk?

You may want to see also

Frequently asked questions

A finance charge is the total amount of interest and loan payments you will have to pay over the life of the mortgage. It is the cost a borrower pays for using a mortgage, personal loan, auto loan or credit card.

Finance charges can include one-time fees, such as an origination fee on a loan, or interest payments. Mortgage finance charges can include the interest rate, application fee, discount points, mortgage insurance and more.

You can find your finance charge on page 5 of the Closing Disclosure form in the “Loan Calculations” section. Finance charges are calculated each billing cycle based on the current base rate that banks charge their most creditworthy customers.

Yes, mortgage insurance is included in the finance charge.