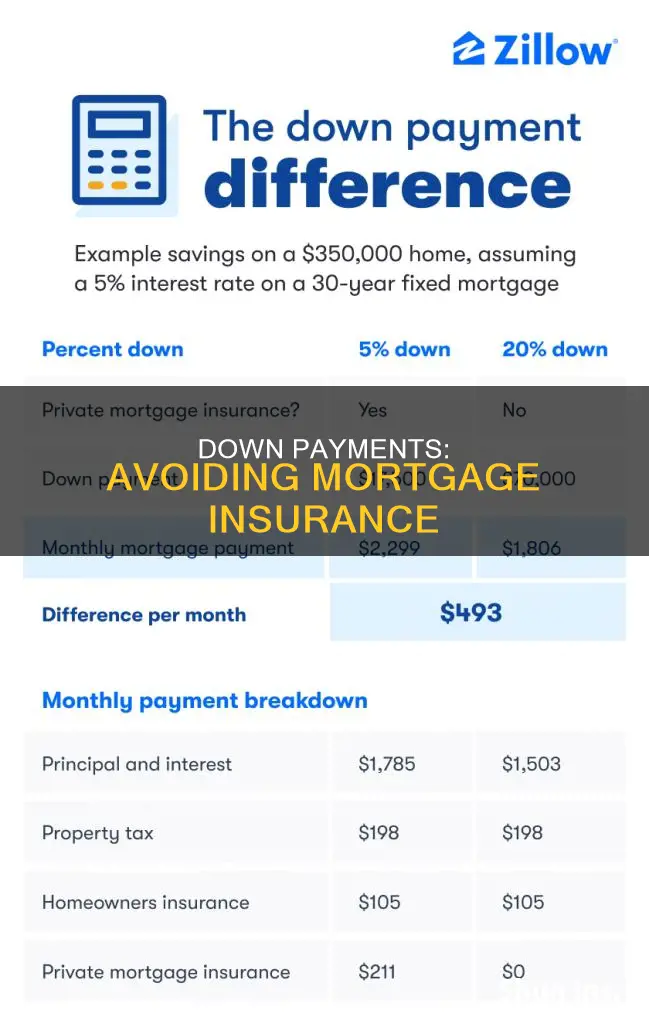

A 20% down payment on a mortgage is a significant sum, and it has long been considered a wise financial move. It can help you avoid paying private mortgage insurance (PMI), which is an additional monthly fee that protects the lender in the event of a loan default. However, it's not mandatory to make a 20% down payment, and there are alternative options available, such as special first-time buyer loans, VA loans, or piggyback loans. These alternatives can help you secure a loan with a smaller down payment, but they may come with their own requirements and costs, such as higher interest rates or funding fees. Ultimately, the decision depends on your financial goals and circumstances.

| Characteristics | Values |

|---|---|

| Down payment | 20% or more |

| Private Mortgage Insurance (PMI) | Not required |

| Mortgage rate | More favorable |

| Monthly payment | Lower |

| Loan size | Smaller |

| Lender's risk | Lower |

| Loan options | VA loans, USDA loans, piggyback loans |

Explore related products

What You'll Learn

![]()

Private mortgage insurance (PMI)

PMI is insurance coverage that protects the lender in case a borrower defaults on a home loan. Typically, a lender will require you to pay for PMI if your down payment is less than 20% on a conventional mortgage. You can get rid of PMI after you build up enough equity in your home. Federal law dictates that your mortgage lender must automatically end your PMI when your loan-to-value (LTV) ratio drops to 78 percent, or when you are one month past the midpoint of your loan term.

There are several ways to avoid paying PMI, including making a 20% down payment on a conventional home loan. Other options include considering lender-paid mortgage insurance or exploring special first-time homebuyer loans without PMI. One strategy to avoid PMI is to use a piggyback mortgage (also called an 80-10-10 loan). This is a unique second loan where the buyer needs only 10% down in cash. The buyer then takes out a second mortgage loan, which provides another 10% of the home's purchase price, effectively giving them a 20% down payment and allowing them to avoid paying mortgage insurance.

VA loans, backed by the Department of Veterans Affairs, do not require a down payment or mortgage insurance, although there is a one-time funding fee. USDA loans, backed by the U.S. Department of Agriculture, are zero-down mortgages for lower- and moderate-income buyers in designated rural and suburban areas. Although USDA loans don't require mortgage insurance, they come with upfront and annual fees.

Insuring Your Home: Application Process

You may want to see also

Explore related products

![]()

Lender-paid mortgage insurance

LPMI is different from private mortgage insurance (PMI), where the borrower pays for the insurance coverage that protects the lender in case of default on a home loan. PMI is typically required when the down payment is less than 20% of the home's value and can add a significant amount to the overall cost of the loan. PMI can be avoided by increasing the down payment to 20% or by exploring alternative options such as LPMI or special first-time homebuyer loans without PMI.

The cost of LPMI is built into the mortgage interest rate, and it remains in effect for the life of the loan unless the loan is refinanced or paid off. LPMI typically costs less than PMI on a monthly basis, but the higher interest rate charged by the lender may result in a higher overall cost over time. Borrowers with excellent credit may pay a quarter-point more in interest for LPMI, which can amount to a significant expense over the loan term.

LPMI can be a good option for borrowers who want to keep their monthly payments low and are willing to accept a higher interest rate. However, it is important to consider the long-term costs associated with LPMI due to the higher interest rate. Borrowers should compare the costs of LPMI with other options, such as PMI or alternative loan programs without mortgage insurance requirements, to make an informed decision based on their financial situation and homeownership goals.

Overall, LPMI is a viable alternative to PMI for borrowers who cannot afford a 20% down payment and want to keep their monthly payments manageable. However, borrowers should carefully consider the potential long-term costs and seek advice to ensure they choose the most suitable option for their circumstances.

Cut Home Insurance Costs

You may want to see also

Explore related products

![]()

Piggyback loans

A piggyback loan is a type of loan that involves getting two mortgages at once. This strategy is often used to avoid paying private mortgage insurance (PMI) when the buyer cannot afford a 20% down payment. The first, or primary mortgage, covers the bulk of the total borrowed amount, while the second mortgage finances a smaller portion. The second mortgage, or junior loan, is typically a home equity loan or home equity line of credit (HELOC) that uses the property as collateral.

The most common type of piggyback loan is the 80-10-10 loan, where the first mortgage covers 80% of the home's value, the second mortgage covers 10%buyer puts down a 10% down payment. This allows the buyer to effectively make a 20% down payment and avoid paying PMI. Other variations of piggyback loans include the 75-15-10 loan, which is more common for condominiums, and the 80-15-5 loan, which reduces the buyer's down payment obligation to just 5%.

While piggyback loans can be a unique strategy to avoid PMI, there are also other options to consider. For example, VA loans backed by the Department of Veterans Affairs and USDA loans backed by the U.S. Department of Agriculture do not require a down payment or mortgage insurance. Additionally, some lenders offer special first-time homebuyer loans without PMI, and buyers can also explore lender-paid mortgage insurance options.

Farmers Insurance and Accident Binders: Understanding the Process

You may want to see also

Explore related products

![]()

No-PMI loans

Private mortgage insurance (PMI) is a type of insurance commonly required by lenders when home buyers make a down payment of less than 20% of the home's value. Mortgage insurance protects the lender in case the borrower defaults on the loan. It is typically rolled into the monthly mortgage payment and can add a significant amount to the overall cost of the loan.

There are several ways to avoid paying PMI. The most common way is to make a 20% down payment on a conventional home loan. However, there are other options for borrowers who cannot afford a 20% down payment. These include:

- Piggyback mortgages: This is a unique second loan where the buyer needs only 10% down in cash. The buyer then takes out a second mortgage loan, which provides another 10% of the home's purchase price. This effectively gives the buyer a 20% down payment, allowing them to avoid PMI.

- Lender-paid mortgage insurance: Some lenders may offer to pay for the mortgage insurance themselves in exchange for a higher interest rate on the loan. This option can be more expensive in the long run but may be a good choice for borrowers who cannot afford the upfront cost of PMI.

- Special first-time homebuyer loans: Some lenders offer special loans for first-time homebuyers that do not require PMI, even with a low down payment. These loans may have other requirements or restrictions, so be sure to read the fine print carefully.

- VA loans: Backed by the Department of Veterans Affairs, these loans are available to current and veteran service members and their eligible spouses. VA loans do not require a down payment or mortgage insurance, although there is a one-time funding fee.

- USDA loans: Backed by the US Department of Agriculture, these are zero-down mortgages for lower- and moderate-income buyers in designated rural and suburban areas. Although USDA loans don't require mortgage insurance, they come with upfront and annual fees.

- FHA loans: These loans only require a 3.5% down payment for creditworthy buyers. However, FHA loans do not have PMI; instead, they come with Mortgage Insurance Premium (MIP), which is required regardless of the down payment size. The only way to eliminate MIP costs is by refinancing into a conventional loan without PMI when you have built enough equity in your home.

Gearbest Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

VA loans

The VA provides insurance to lenders, assuring them that they will be repaid if the veteran can no longer make payments. This insurance is called the VA guaranty. It is not issued by the Department of Veterans Affairs but by private companies, including banks, credit unions, and mortgage companies.

Accident Insurance: Dave Ramsey's Take on Coverage

You may want to see also

Frequently asked questions

Yes, a 20% down payment helps you avoid paying private mortgage insurance (PMI).

PMI is a type of insurance that protects the lender in case the borrower defaults on the loan.

PMI rates vary by credit score and other factors, but they typically range from 0.58% to 1.86% of the original loan amount.

There are several options for avoiding PMI without a 20% down payment, including:

- A piggyback loan or a second mortgage that covers 10% of the home's purchase price, so you effectively have a 20% down payment.

- Lender-paid mortgage insurance, where you pay a higher interest rate instead of PMI.

- Special first-time homebuyer loans or bank programs for low-income buyers that do not require PMI.

- VA loans, which are available to veterans and service members and do not require a down payment or mortgage insurance, although there is a one-time funding fee.

- USDA loans, which are for low- and moderate-income buyers in designated rural and suburban areas and do not require a down payment or mortgage insurance, although there are upfront and annual fees.

A 20% down payment can help you secure a lower interest rate and lower your monthly payments. It also gives you more equity in the home, which can be useful if you need to sell quickly.