When buying a home, two types of insurance come into play: homeowners insurance and private mortgage insurance (PMI). Homeowners insurance is often integrated with mortgage payments through an escrow account, which is commonly required by mortgage lenders. An escrow account is a separate account where your lender collects funds for property taxes and insurance and disburses them when needed. This method benefits both the lender and the borrower, as it simplifies budgeting and ensures compliance with mortgage and insurance terms. However, whether homeowners insurance is included in your mortgage depends on factors such as the type of mortgage, down payment size, and equity. While most lenders require homeowners insurance to protect their investment, it is not always bundled with mortgage payments, and homeowners may have the option to pay it separately.

| Characteristics | Values |

|---|---|

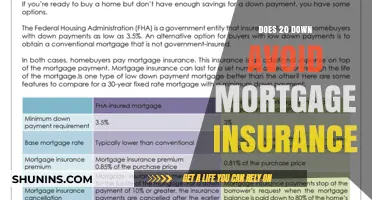

| Homeowner's insurance purpose | Protects the homeowner financially in the event of damage or destruction of their home or possessions. |

| Mortgage insurance purpose | Protects the lender if the homeowner defaults on their loan. |

| Homeowner's insurance necessity | Usually a necessity for all homeowners. |

| Mortgage insurance necessity | Not always necessary; depends on the down payment and type of mortgage. |

| Payment arrangement | Homeowner's insurance is often paid through an escrow account, but can also be paid directly to the insurer. |

| Escrow account | A separate account set up by the lender to collect funds for property taxes and insurance. |

| Cancelling escrow | Escrow can be cancelled once the homeowner has paid off 20% of the mortgage principal. |

Explore related products

$14.37 $24.99

What You'll Learn

- Homeowner's insurance is required by mortgage lenders

- Private mortgage insurance (PMI) protects lenders, not homeowners

- Homeowner's insurance can be paid through escrow

- Homeowner's insurance covers damage to the home and possessions

- Homeowner's insurance is still necessary after the mortgage is paid off

![]()

Homeowner's insurance is required by mortgage lenders

When you buy a home, you'll need to understand the basics of two types of insurance: homeowners insurance and private mortgage insurance (PMI). While PMI is insurance that some lenders may require to protect their interests should you default on your loan, homeowners insurance is required by all mortgage lenders for all borrowers.

Homeowners insurance, also known as home insurance, is coverage that is required by all mortgage lenders for all borrowers. It is not related to the amount of down payment that you make on your home but is tied to the value of your home and property. Homeowners insurance is typically required for anyone who takes out a mortgage loan to buy a home. After you pay off your mortgage, you may still want to continue to have a homeowners insurance policy to protect your investment.

The main purpose of homeowners insurance is to meet your specific needs. It offers property and liability protection, but you can also customise your policy with a wide variety of add-on coverages. For example, homeowners insurance can help pay to repair or rebuild your home after a covered disaster or event such as a break-in, a lightning storm, a house fire, a tornado, or a hurricane. Most policies also cover detached structures on the property, such as a storage shed, gazebo, or guest house. Additionally, homeowners insurance protects your possessions, both inside and outside your home, such as your mobile phone or a newly purchased holiday gift that gets stolen.

Homeowners insurance payments are typically integrated with your mortgage payment through your escrow account, which is commonly required by mortgage lenders. An escrow account, set up by your lender, acts as a financial intermediary, collecting funds for property taxes and insurance and disbursing them when needed. If your down payment is more than 20%, your lender likely won’t require you to have an escrow account, and you may have the option of paying for homeowners insurance and property taxes directly.

PC World Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Private mortgage insurance (PMI) protects lenders, not homeowners

When you buy a home, two types of insurance come into play: homeowners insurance and private mortgage insurance (PMI). Homeowners insurance is usually a necessity for all homeowners. It covers the structure of your home and your possessions, protecting them from disasters or events such as break-ins, lightning storms, house fires, tornadoes, and hurricanes. Most policies also cover detached structures on the property, such as sheds, gazebos, or guest houses.

Private mortgage insurance (PMI), on the other hand, is not meant for homebuyers or homeowners. It is a type of insurance that protects the lender, not the borrower. PMI is typically required when borrowers cannot make a down payment of 20% or more on a conventional loan. In such cases, lenders may require PMI to protect their interests in case the borrower defaults on the loan. It is an additional cost that is usually paid on top of the monthly mortgage payment.

While PMI can help borrowers qualify for loans they might not otherwise be able to obtain, it is important to remember that it does not provide protection for the borrower. If a borrower falls behind on their loan payments, they can still lose their home through foreclosure, even with PMI in place. Therefore, it is essential to understand that PMI is not a substitute for homeowners insurance, which provides financial protection from damages to the home and its contents.

Homeowners may be able to cancel PMI after they have made enough payments to reach more than 20% equity in their home. At this point, it is worth checking with the lender to understand when and how PMI can be removed from the loan. In summary, while PMI is a necessary cost for some homebuyers, it is essential to recognize that it protects the lender's interests and does not replace the need for homeowners insurance.

Allstate: Insuring Old Homes

You may want to see also

Explore related products

$4.99 $14.99

$9.97

![]()

Homeowner's insurance can be paid through escrow

When you buy a home, two types of insurance come into play: homeowners insurance and private mortgage insurance (PMI). Homeowners insurance is an insurance policy that covers the costs of damage to your home, your personal property, and/or guests on your property. Private mortgage insurance, on the other hand, protects the lender rather than the homeowner by paying them if you default on the loan.

Homeowners insurance can be paid through escrow, which is a separate account where your lender collects your payments for homeowners insurance and property taxes, which are built into your mortgage. This method benefits both you and your lender. You don’t have to worry about keeping track of multiple bills, and they are assured that you are staying current on your financial obligations. Some borrowers will be required to escrow their insurance and property taxes into their mortgage payments, while others may have the option to opt into an escrow account or pay their insurance and property taxes directly. This depends on the type of mortgage, the size of the down payment, and the equity. If you make a down payment of 20% or more, you will usually be able to choose whether or not to pay your insurance with your mortgage.

If you pay your homeowners insurance through escrow, it will be included in your monthly mortgage payment, along with PMI costs and property taxes. This simplifies budgeting and ensures that you are complying with your mortgage and insurance terms. It also reduces the risk of late or missed payments by consolidating your homeownership expenses into one convenient payment.

However, there may be times when paying your homeowners insurance directly is preferable. Paying your insurance premiums directly to the insurer can provide more flexibility and understanding of your policy and allow you to switch providers with ease. For instance, you could choose how to pay and how frequently to make payments. If you prefer a more hands-on approach to financial management, you may want to ask your lender if you can pay your homeowners insurance yourself.

Citations and Insurance: When to Report and Why

You may want to see also

Explore related products

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)

![]()

Homeowner's insurance covers damage to the home and possessions

When buying a home, two types of insurance come into play: homeowners insurance and private mortgage insurance (PMI). Homeowners insurance, also known as home insurance, is required by all mortgage lenders for borrowers. It is tied to the value of your home and property and is usually necessary for anyone taking out a mortgage loan.

Homeowners insurance covers damage to your home and possessions. It typically covers the structure of your home and your belongings in the event of a disaster, such as a fire, heavy wind, lightning, thunderstorm, or hurricane. It may also cover detached structures on the property, such as a storage shed, gazebo, or guest house. Most policies will also cover your possessions outside of your home, such as your mobile phone, and may provide financial support if you damage someone else's property.

The amount of coverage you have for your home and possessions may vary depending on your policy. Homeowners insurance policies generally have different limits for each type of coverage. For example, you may have a coverage limit of $300,000 for the structure of your home and $150,000 for your belongings. It is important to read the fine print before purchasing a policy to understand the specific coverage provided.

You can choose to pay for your homeowners insurance separately or roll it into your mortgage payments. If you pay for it as part of your mortgage, your lender will take your payments for homeowners insurance and make the payments for you through an escrow account. This benefits both you and your lender, as it ensures you stay on top of your financial obligations.

Alliance Global Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Homeowner's insurance is still necessary after the mortgage is paid off

When you buy a home, two types of insurance come into play: homeowners insurance and private mortgage insurance (PMI). While PMI is a protective layer for lenders, ensuring they are covered if you can't repay the loan, homeowners insurance is a shield for the property owner, covering potential damages to the home and its contents.

Homeowners insurance is typically required for anyone who takes out a mortgage loan to buy a home. However, after you pay off your mortgage, you are no longer required to carry home insurance. Nevertheless, it is highly recommended that you continue to invest in it to offset potential costs in the event of damage or other home issues. Here are some reasons why homeowners insurance is still necessary even after the mortgage is paid off:

Financial Protection

Your home is one of your biggest financial assets, and without insurance, you would bear the full cost of any damage or loss. Homeowners insurance can help pay to repair or rebuild your home after a covered disaster or event, such as a break-in, a lightning storm, a house fire, a tornado, or a hurricane. Most policies also cover detached structures on the property, such as a storage shed, gazebo, or guest house.

Protection of Possessions

Homeowners insurance also protects your possessions within the home, such as furniture, clothing, sports equipment, and tools. Additionally, it may cover items outside your home, such as your mobile phone or other valuable items that get stolen while you are away.

Liability Protection

Homeowners insurance provides liability protection for your assets if you are sued due to an accident or injury on your property. For example, if a guest injures themselves on your property and takes legal action, homeowners insurance can help cover the costs.

Simplified Budgeting

Including homeowners insurance in your mortgage payments through an escrow account can simplify budgeting and financial management. An escrow account acts as a financial intermediary, collecting funds for property taxes and insurance and disbursing them when needed. This method ensures that you comply with your mortgage and insurance terms while also reducing the risk of late or missed payments.

In conclusion, while homeowners insurance may no longer be mandatory after paying off your mortgage, maintaining a policy is crucial for protecting your financial investment, possessions, and liability. By continuing your coverage, you can have peace of mind knowing that you are prepared for any unforeseen events that may impact your home and assets.

Unoccupied Home Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Homeowners insurance is a shield for the property owner, covering potential damages to the home and its contents. Mortgage insurance, also known as PMI, is a protective layer for lenders, ensuring they're covered if you can't repay the loan.

Home insurance payments are typically integrated with mortgage payments through an escrow account. This is a separate account where your lender collects funds for property taxes and insurance and disburses them when needed. However, whether your lender will allow you to pay homeowners insurance separately depends on your type of mortgage, down payment size and equity.

Paying homeowners insurance through an escrow account guarantees adherence to your mortgage lender's terms and conditions. It also simplifies budgeting and ensures you don't miss any payments.

Paying homeowners insurance separately can give you greater control over your finances. Paying premiums directly to the insurer can provide more flexibility and understanding of your policy and allow you to switch providers with ease.