Mortgage calculators are a useful tool for prospective homeowners to estimate their monthly mortgage payments. They can also be used to calculate how much house one can afford based on their income, debt payments, and down payment. While some mortgage calculators include taxes and insurance, others do not. It is important to understand what is included in your monthly mortgage payments, as they may include more than just the repayment of the amount borrowed.

| Characteristics | Values |

|---|---|

| What does a mortgage calculator do? | It estimates monthly mortgage payments. |

| What does it include? | Principal, interest, property taxes, and homeowners insurance. |

| What else can it include? | Private mortgage insurance (PMI), escrow, closing costs, and homeowners association (HOA) fees. |

| What does it depend on? | The home price, down payment, interest rate, and loan term. |

| How does it help? | It helps to understand how much home you can afford and how your monthly payment would change depending on your loan terms. |

| What else can it do? | It can be used to calculate how much you can afford based on income, debt payments, and down payment. |

| Are there other ways to calculate mortgage payments? | Yes, there are standard formulas to calculate mortgage payments manually. |

Explore related products

What You'll Learn

![]()

How to calculate your DTI

Mortgage calculators are useful tools that can help you to estimate your monthly mortgage payments. They can also be used to calculate your debt-to-income ratio (DTI).

Your DTI is an important metric that lenders use to determine whether you can repay your loan. It is the percentage of your gross monthly income that goes towards paying off your debts. Generally, a higher DTI ratio presents more risk for the lender, and a lower DTI indicates that you will more likely be able to afford a mortgage. A DTI of 20% or below is considered excellent, while a DTI of up to 36% is considered ideal. However, some lenders may accept higher ratios, especially if you have other "compensating factors" such as a larger down payment.

To calculate your DTI, you need to add up all your monthly debt payments, such as credit card debt, student loans, alimony, child support, auto loans, and projected mortgage payments. If you are taking out the mortgage with a co-borrower, include their debt payments as well. Then, divide the total of your monthly debt payments by your monthly gross income before deductions for taxes, retirement savings, etc. To get a percentage, multiply the result by 100.

For example, if your monthly debt payments add up to $300 and your monthly income before taxes is $1,000, then your DTI is ($300 / $1,000) x 100 = 30%.

You can use online DTI calculators to quickly understand whether you meet a lender's requirements and to monitor your progress over time.

Airfare Insurance: Is It a Worthy Investment?

You may want to see also

Explore related products

![]()

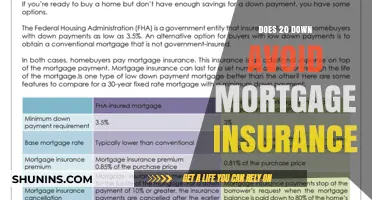

Mortgage insurance

FHA loans, for example, require mortgage insurance, which includes both an upfront cost paid as part of closing costs and a monthly cost included in your monthly payment. On the other hand, VA-backed loans do not require monthly mortgage insurance premiums, but borrowers pay an upfront "funding fee" that can be rolled into the mortgage.

Switching Home Insurance: A Simple Guide

You may want to see also

Explore related products

![]()

Escrow accounts

When you take out a mortgage, your lender may set up a mortgage escrow account, which is a way for them to help you manage the costs associated with homeownership. An escrow account is sometimes called an impound account, depending on where you live. Each month, a portion of your monthly mortgage payment goes into this account, which is then used to cover expenses such as property taxes, insurance premiums, and private mortgage insurance. The benefit of having an escrow account is that you don't have to worry about saving up for or missing large tax or insurance bills, as your lender pays them on your behalf from the funds in your escrow account.

Your lender will calculate your annual tax and insurance payments, divide that amount by 12, and add the result to your monthly mortgage statement. They will then deposit the escrow portion of your mortgage payment into the account and pay your insurance and tax bills when they are due. Your lender may also require an "escrow cushion" to cover any unanticipated costs, such as a tax increase. Additionally, escrow accounts may be required by law in some cases.

It's important to note that not all lenders require an escrow account. Some may allow you to pay taxes and insurance on your own, making you responsible for saving the necessary funds and paying on time. Generally, lenders use the loan-to-value (LTV) ratio to determine if your mortgage loan will require an escrow account. Borrowers whose mortgage amount is 80% or less of the home's value may avoid escrow if they choose. However, if you have less than 20% equity as a buyer, you are typically required to have an escrow account. Loans guaranteed by the Federal Housing Administration (FHA) and Veterans Affairs (VA) also mandate the use of escrow accounts for these expenses.

Off-the-Job Accident Insurance: Is It Necessary?

You may want to see also

Explore related products

![]()

Closing costs

- Origination fees: charged by the lender to cover processing expenses, usually a percentage of the amount loaned.

- Settlement and title fees: these may include document delivery and preparation fees, lender's title insurance, and survey fees.

- Third-party fees: such as home warranty fees, homeowners association (HOA) dues, and homeowners/hazard insurance.

- Taxes and government fees: including property taxes, mortgage surcharges, and recording fees.

- Prepaid interest: this covers the interest that accrues on your loan from the closing date until the last day of the month.

- Discount points or mortgage points: a fee paid to the lender to lower the interest rate. One point equals one percent of the loan amount.

- Private mortgage insurance (PMI): if your down payment is less than 20%, lenders may require you to pay PMI to protect their investment.

It is important to note that closing costs do not represent fees, but rather establish the funds needed to service your loan properly. You can use closing costs calculators to estimate these costs and compare different lenders to find the most suitable loan terms for your needs.

Reporting Fake Insurance: Your Action Plan

You may want to see also

Explore related products

![]()

Affordability

Mortgage calculators typically take into account the home price, down payment, interest rate, and loan term. They may also include property taxes, homeowners insurance, and private mortgage insurance (PMI). By inputting this information, you can get an estimate of your monthly mortgage payments.

Some mortgage calculators allow you to customise your inputs, making assumptions for fields you may not know yet. For example, you can usually adjust the home price, down payment, or mortgage terms to see how your monthly payment changes. This flexibility is particularly useful if you are still in the early stages of planning and are unsure about specific details.

It is important to note that mortgage calculators provide estimates, and actual payments may differ. Factors such as closing costs, HOA fees, and escrow accounts can impact your monthly expenses. Additionally, your down payment amount can affect your mortgage over time. A higher down payment can save you money in the long run, while a lower down payment may require PMI, increasing your monthly payments.

Red Light Camera Tickets: Do Insurers Know?

You may want to see also

Frequently asked questions

A mortgage calculator helps you to estimate your monthly mortgage payments. It takes into account the home price, down payment, interest rate, and loan term.

Monthly mortgage payments often include the loan payment, monthly interest, property taxes, and homeowners insurance.

You can use a mortgage calculator by inputting the home price, your down payment, the property ZIP code, your credit score, and what is most important to you when choosing a loan. The calculator will then provide your estimated total mortgage payment.