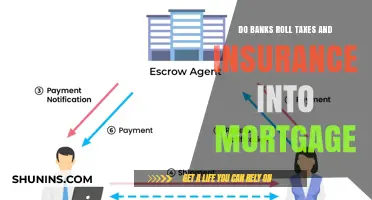

When it comes to owning a home, property taxes and insurance are inevitable costs. These costs can be paid through your mortgage, depending on the terms of your mortgage contract. Lenders often roll property taxes and insurance into borrowers' monthly mortgage bills, which can be convenient for budgeting and avoiding large tax bills. This is typically done through an escrow account, where a portion of your monthly payment is set aside for taxes and insurance. However, this may result in larger monthly payments and less control over when and how your taxes are paid. It's important to understand what's included in your monthly mortgage payment and be aware of potential drawbacks to make informed financial decisions.

| Characteristics | Values |

|---|---|

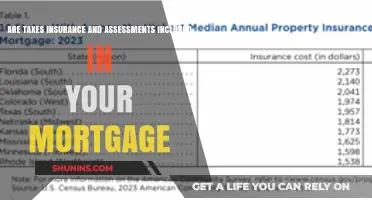

| Are property taxes paid through the mortgage? | Property taxes are usually included in mortgage payments. However, it depends on the loan and the terms of the mortgage contract. |

| How are property taxes paid through the mortgage? | Property taxes are paid through a system called an escrow account, where a portion of the monthly mortgage payment is set aside specifically for property taxes. |

| How much is paid through the mortgage? | The amount paid towards property taxes depends on the local government's tax rate and the property's assessed value. |

| Are there any drawbacks to paying property taxes through the mortgage? | Yes, including property taxes in the mortgage results in larger monthly payments and gives the homeowner less direct control over when and how their taxes are paid. |

| Are there any benefits to paying property taxes through the mortgage? | Paying property taxes through the mortgage makes budgeting more predictable and ensures that property taxes are paid on time, avoiding large tax bills. |

Explore related products

$4.99 $14.99

What You'll Learn

![]()

Property taxes are usually paid through escrow accounts

Property taxes can be paid in several ways. One common method is through an escrow account set up by your lender. This account ensures that your property taxes are paid on time. The lender will estimate your annual tax obligation and divide it into equal monthly payments, which are then added to your mortgage payment. This way, you don't have to worry about large tax bills every few months, and you can rest assured that your taxes are paid on time.

However, it is important to note that not all mortgages include escrow accounts. Some homeowners prefer to handle their property tax payments directly to have more control over their finances. In this case, they would need to keep track of payment deadlines, which can vary by location.

Additionally, the inclusion of property taxes in your mortgage payments depends on the terms of your mortgage contract. Lenders often roll property taxes into borrowers' monthly mortgage bills, but this is not always the case. It is essential to review your monthly mortgage statement and loan closing documents to understand better if your property taxes are included in your mortgage payments.

Overall, property taxes are an inevitable part of homeownership, and whether they are paid through an escrow account or directly to the local government, it is crucial to stay on top of these payments to avoid any financial surprises.

Insurance Reimbursement: Where and How to Report It

You may want to see also

Explore related products

$11.25 $16.99

![Manitoba Lands for Sale by Crotty & Cross, Real Estate Brokers, Financial and Insurance Agents Funds Invested on First Mortgage Security, Rents Collected, Taxes Paid, and 1893 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Homeowners insurance is often included in mortgage payments

When it comes to owning a home, property taxes and insurance are inevitable expenses. While it is possible to pay these separately, they are often included in mortgage payments, which can have its advantages and disadvantages.

Homeowners insurance is typically required by lenders to protect their financial interests in the event of theft, natural disasters, or other losses. This insurance, along with property taxes, can be included in your monthly mortgage payments through an escrow account. An escrow account is a savings account set up by your lender to ensure that property taxes and insurance are paid on time. The money in this account is used to cover essential protections and local tax obligations.

When you apply for mortgage preapproval, your lender will estimate your monthly payment, including the principal and interest, and the estimated monthly escrow payment based on the typical expenses for homes in the area you're looking to buy. This estimate is calculated based on how much the previous owner paid in taxes and insurance or the average taxes in the area. The actual tax total will be determined once you choose a home, and the insurance will be calculated once you select a company and policy.

Including property taxes and homeowners insurance in your mortgage payments has its benefits. It simplifies budgeting by making it easier to predict and manage expenses. You won't have to worry about large tax and insurance bills every few months, and you can rest assured that your taxes will be paid on time, avoiding any consequences of unpaid taxes, such as a tax lien on your property. Additionally, your lender may offer a lower interest rate when you choose to pay your property taxes through an escrow account.

However, there are also potential drawbacks to consider. Including these expenses in your mortgage payments will result in larger monthly payments. You may also have less direct control over when and how your taxes and insurance are paid, as your lender will manage these payments on your behalf. There is also the possibility of escrow shortages or overages, as your tax and insurance bills may fluctuate, leading to adjustments in your monthly payment.

Ultimately, the decision to include homeowners insurance and property taxes in your mortgage payments depends on your financial goals, preferences, and the terms of your mortgage contract. It's essential to understand the components of your mortgage payment to manage your budget effectively and avoid surprises.

Insuring a Home Renovation: What You Need to Know

You may want to see also

Explore related products

![]()

Private mortgage insurance (PMI) may be required

When you apply for a mortgage, your monthly payment will include the principal and interest, as well as an estimated escrow payment for property taxes and homeowners insurance. Escrow accounts are a common way to manage these additional expenses, and they are typically set up by your lender.

Private mortgage insurance (PMI) is an extra expense that may be required when taking out a conventional mortgage with a down payment of less than 20% of the purchase price. PMI is designed to protect the lender in case the borrower fails to make loan payments and defaults on the loan. While PMI does increase the cost of your loan, it can also help you qualify for a loan that you might not otherwise be able to obtain.

The requirement to purchase PMI usually applies when refinancing a conventional loan, and your equity is less than 20% of your home's value. PMI can be paid through a one-time upfront premium at closing, or it may be added to your monthly mortgage payments. Lenders may offer different options for paying PMI, and it is essential to understand the total costs over different timeframes to make an informed decision.

It is worth noting that PMI is not permanent, and lenders are required to cancel it once your mortgage balance reaches 78% of your home's original value or when you reach the halfway point of your loan term, whichever comes first. Additionally, you can avoid PMI altogether by saving up for a 20% down payment on a conventional loan. This larger down payment can also result in a lower interest rate for your mortgage.

In summary, while PMI may be an added expense for homebuyers, it can provide the benefit of facilitating loan approval and homeownership. By understanding the requirements and options for PMI, homebuyers can make informed decisions about their mortgage choices.

Insurance Binder: Your Temporary Home Insurance

You may want to see also

Explore related products

![]()

HOA fees are typically paid separately

When you take out a mortgage, it's important to understand what's included in your monthly payments. While property taxes and insurance are often included, HOA fees are typically paid separately.

Homeowners Association (HOA) fees are paid to a homeowners association, which is an organization that governs a community of homeowners. These fees are used to maintain and improve the community, and they can vary widely depending on the services provided. HOA fees can range from just $100 a year to more than $1,000 per month, and they are usually paid monthly or quarterly.

When you buy a home in an HOA-governed community, you become a member of the HOA and are subject to its rules and regulations, known as Covenants, Conditions, and Restrictions (CC&Rs). These rules can place restrictions on how you use your home, such as forbidding home-based businesses or renters. It's important to carefully review the CC&Rs before purchasing a home in an HOA community to ensure you understand the restrictions and fees associated with membership.

While HOA fees are typically paid separately from your mortgage, some lenders may allow you to include them in an escrow account. This means that you would pay the fees as part of your monthly mortgage payment, and the lender would hold the money until it is time to pay the HOA. However, this is not standard practice, and most HOA fees are paid directly to the HOA by the homeowner.

It's worth noting that HOA fees can impact your ability to qualify for a mortgage. Lenders will consider the required HOA fee when evaluating your debt-to-income ratio, and a high HOA fee could affect the size of the mortgage you are eligible for. Therefore, it is crucial to consider the cost of HOA fees when budgeting for a new home and to communicate openly with your lender about how these fees may affect your financial situation.

The Complex Web of Farmers Insurance: Unraveling the Oligopoly's Reach and Impact

You may want to see also

Explore related products

![]()

Maintenance and repairs are the homeowner's responsibility

When it comes to property taxes and insurance, there are a few things to keep in mind. Firstly, property taxes are indeed included in most mortgage payments, along with the principal, interest, and homeowners insurance. These additional expenses are typically managed through an escrow account set up by the lender. However, it's worth noting that property taxes can vary significantly by location, and in some cases, they may increase after the sale of a property. Therefore, it's essential to factor in property taxes when calculating your potential mortgage payment.

Now, regarding maintenance and repairs, it is essential to understand that homeowners have a significant responsibility in this area. While specific obligations may vary depending on the community and the provisions of the Homeowners Association (HOA) governing documents, there are some general guidelines. Homeowners are typically responsible for maintaining the interior of their units, including any repairs to walls, floors, ceilings, fixtures, and appliances. This also includes preventive maintenance to keep their units in good condition and avoid costly repairs down the line. Additionally, homeowners are responsible for maintaining their personal property within their units, such as furniture, electronics, and other belongings.

In the case of common areas, the responsibilities may be shared between the HOA and individual homeowners. The HOA is generally responsible for maintaining and repairing areas accessible to everyone in the community. However, if there is an area shared by only a few community members, it becomes a shared responsibility. It's important to note that disputes may arise between homeowners and the HOA regarding repair responsibilities, and resolving them amicably requires careful review of the HOA's governing documents.

To ensure a harmonious living environment, homeowners should promptly report any maintenance issues within their units or common areas to the HOA. This allows for timely repairs and prevents further damage. Additionally, homeowners should maintain adequate insurance coverage for their units and personal property, as it provides financial protection in the event of damage or loss that may not be covered by the HOA's insurance policy.

To stay on top of maintenance and repairs, homeowners can refer to seasonal home maintenance checklists, which provide recommendations for various tasks throughout the year. These checklists cover tasks such as cleaning gutters, inspecting roofing, power-washing siding, and more. By following these checklists and staying proactive with maintenance, homeowners can help keep their homes in prime condition and avoid costly repairs.

Salary Continuance Insurance: Is It Worth the Cost?

You may want to see also

Frequently asked questions

It depends on the loan. Most loans include property taxes and insurance in the monthly payment, but this is not always the case. If your mortgage doesn't include an escrow account, you'll pay your property taxes and insurance premiums directly to your local government and insurance company.

An escrow account is a savings account set up by your lender to fund essential expenses like property taxes and homeowners insurance. This ensures that your property taxes and insurance get paid on time.

Check your monthly mortgage statement. If you see a line item labelled "escrow" or "escrow payment", your lender is likely collecting money to cover property taxes and insurance. You can also check your loan closing documents, which should outline whether your mortgage includes an escrow account.

Including property taxes in your mortgage payments can make it easier to budget and avoid large tax bills. It also protects your lender, as they will likely have to pay the remaining property tax amount if a homeowner is forced into foreclosure.

Your monthly mortgage payments will be higher, and you will have less direct control over when and how your taxes and insurance are paid. There is also the potential for escrow shortages or overages, as your tax bills may fluctuate.