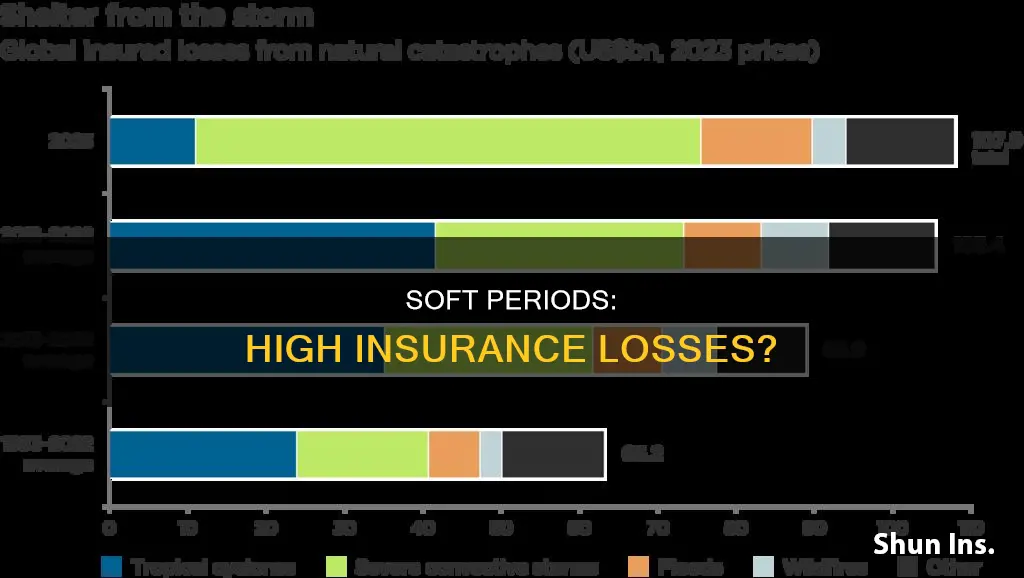

The insurance market is characterised by cyclical fluctuations between 'hard' and 'soft' periods. During soft periods, insurance companies are more lenient about the level of risk they will accept and compete with one another by lowering premiums to attract more customers. This can lead to underwriting losses, where more is paid in claims than is brought in from premiums. While natural disasters, such as hurricanes, can cause large-scale losses for insurance companies, it is unclear whether these losses are specifically associated with soft market periods.

| Characteristics | Values |

|---|---|

| Market Type | Soft Market |

| Market Tendency | Stable or Lowering Premiums |

| Insurer Risk Appetite | Higher |

| Insurer Competition | Higher |

| Insurer Profitability | Lower |

| Insurer Investment Income | Higher |

| Interest Rates | Low |

| Policyholder Coverage | Less |

| Policyholder Non-Renewals | Higher |

| Coverage Availability | Reduced |

| Underwriting Losses | Higher |

| Underwriting Standards | Relaxed |

Explore related products

What You'll Learn

- Soft markets are characterised by lower premiums, broader terms of coverage, and higher available limits of liability

- Insurers are more lenient about the level of risk they will accept in a soft market

- Soft markets generally have high-dollar reserves and can make money in the stock market

- A soft market is precipitated by a catastrophe or similar significant loss

- A soft market is generally preferred by consumers

![]()

Soft markets are characterised by lower premiums, broader terms of coverage, and higher available limits of liability

In a soft market, insurance companies have a broader appetite for "risk" and compete with one another by lowering premiums to attract more customers. This can mean more agents in the market to underprice. Some customers go straight to the source and get their quotes online. For agents who are just entering the market, this is often an ideal time to get started due to the relaxed underwriting criteria. However, the market can change dramatically and unexpectedly.

A soft market is generally a period when insurance companies have high-dollar reserves and can make money in the stock market. Thus, they can lower their premiums to a point where they don't make money or even lose money on the "underwriting" side of the equation. This is also when the underwriting cycle begins to turn, and insurers start to tighten their underwriting standards and sharply raise premiums after a period of severe underwriting losses or negative shocks to capital.

The insurance cycle may harden for a long period to recover. Depending on where in the cycle insurers are, the market may find itself "softening" or "hardening". As a consumer, you would prefer the soft market. The losses stemming from 9/11 caused the last hard insurance market. It has been soft ever since.

Direct Auto Insurance and National General: Are They Synonymous?

You may want to see also

Explore related products

![]()

Insurers are more lenient about the level of risk they will accept in a soft market

The insurance market is characterised by periods of "soft" and "hard" market conditions. A soft market is when insurance companies are more lenient about the level of risk they will accept and compete with one another by lowering premiums to attract more customers. This is generally a period when insurance companies have high-dollar reserves and can make money in the stock market.

In a soft market, insurance companies have a broader appetite for risk and compete by lowering premiums to attract more customers. This results in more agents in the market, and it is an ideal time for new agents to enter the market due to the relaxed underwriting criteria. This is because insurance companies have high-dollar reserves and can afford to lower their premiums to a point where they may not make money or even lose money.

During a soft market, consumers and businesses can find more favourable insurance terms, broader coverage options, and reduced costs. This is because insurers are more lenient and accept a higher level of risk. They can also offer more comprehensive coverage and lower premiums due to the increased competition among insurers. A soft market is marked by lower insurance premiums, more lenient underwriting criteria, and increased competition among insurers.

A soft market is generally preferred by consumers as it offers lower premium rates and more accessible insurance coverage. It is a period when insurance companies are more willing to take on risk and compete for customers by offering lower prices. This increased competition drives down prices and creates more favourable terms for consumers.

However, a soft market can change dramatically and unexpectedly. As insurers compete for customers, their profits may diminish or disappear, leading to a hard market. In a hard market, insurers become more cautious and reduce their risk tolerance, only wanting to insure low-risk clients to ensure underwriting profits. This results in higher premiums, stricter underwriting standards, and reduced availability of insurance coverage.

U-Turn: USAA Auto Insurance and Rodent Damage—What's Covered?

You may want to see also

Explore related products

![]()

Soft markets generally have high-dollar reserves and can make money in the stock market

A soft market is a phase in the economic cycle characterised by an excess of sellers over buyers, leading to low prices. This term is most commonly used in the insurance industry, where a soft market can be contrasted with a hard market. In a hard market, there is competition among buyers and low fund availability among insurance companies. As a result, insurance providers become selective about who they will insure, generally avoiding high-risk cases.

A soft market in the insurance industry is characterised by high-dollar reserves, enabling insurance companies to make money in the stock market. This means that they can afford to lower their premiums to attract customers, even to the point where they lose money on the underwriting side of the equation. This is because, with lower premium rates, lower commissions per policy are generated, and insurance companies must sell more policies to maintain their income.

In a soft market, insurance companies can be more lenient about the level of risk they will accept. They may also offer expanded coverage to attract customers who are shopping around. This is in contrast to a hard market, where insurers reduce their risk tolerance and become more exacting in their standards.

The soft market will persist until supply and demand are brought into a new balance, or equilibrium, once prices fall sufficiently. As prices fall, more buyers may enter the market, and some suppliers may even switch roles from seller to buyer. This process can lead to a temporary state of disequilibrium, where sellers compete more for buyers, and buyers have relatively more bargaining power.

Lowering Auto Insurance: Country Financial Tips and Tricks

You may want to see also

Explore related products

![]()

A soft market is precipitated by a catastrophe or similar significant loss

The insurance market cycle, also known as the underwriting cycle, is characterised by fluctuations between profitable and unprofitable periods. The cycle begins when insurers tighten their underwriting standards and raise premiums in response to severe underwriting losses or negative shocks to capital, such as investment losses. This results in higher profits and capital accumulation, leading to increased competition and a subsequent decrease in premiums. Eventually, underwriting losses occur, setting the stage for the cycle to begin again.

A soft market is a period within the insurance cycle where premiums are stable or decreasing, coverage terms are broader, and competition among insurers is more intense. During a soft market, insurers are more tolerant of risk and may lower their standards to attract more customers. This can lead to a situation where insurers either make minimal profits or incur losses on the underwriting side.

A soft market can be precipitated by a catastrophe or similar significant loss, such as Hurricane Andrew or the attacks on the World Trade Center. These events trigger a surge in claims, causing less stable companies to exit the market and larger companies to experience reduced capital. As a result, the market hardens, and premiums rise rapidly as underwriters become more cautious about taking on risks.

The transition from a soft to a hard market can be abrupt and unexpected. For instance, the losses stemming from 9/11 led to a hard insurance market that persisted for an extended period. During a hard market, policyholders may face challenges such as receiving non-renewal notices, reduced coverage options, and higher premium expenses.

Understanding Auto Insurance: Points and Their Impact

You may want to see also

Explore related products

![Going Postal[GOING POSTAL][Mass Market Paperback]](https://m.media-amazon.com/images/I/61wlzoQiVDL._AC_UL320_.jpg)

![]()

A soft market is generally preferred by consumers

In a soft market, insurance companies have a broader appetite for "risk" and are more lenient about the level of risk they will accept. They experience lower claim frequency, milder losses, and improved investment income. As a result, they are more willing to take on risks and offer broader coverage options with lower premiums. Common characteristics of a soft home insurance market include increased accessibility to insurance, more policy choices, lower deductibles, and more flexible policy terms.

For example, if a soft market occurs among auto dealers, prices for cars may drop, along with the requirements needed to qualify for financing. Dealers may try to make up the difference on their narrower margins through higher volume sales.

The opposite of a soft market in the insurance industry is a hard market, which is characterised by competition among buyers and low fund availability among insurance companies. Thus, insurance companies tend to be selective about who they will provide insurance to and generally avoid high-risk cases. A hard market is worse for consumers as it involves more expensive insurance premiums and reduced accessibility.

The insurance cycle may harden for a long period to recover. Depending on where in the cycle insurers are, the market may find itself "softening" or "hardening". A soft market can be ideal for agents who are just entering the market due to the relaxed underwriting criteria. However, the market can change dramatically and unexpectedly, so it is important for consumers to be aware of the characteristics of both hard and soft markets when shopping for insurance.

Uber Drivers and Insurance: What's the Connection?

You may want to see also

Frequently asked questions

A soft market in the insurance industry is when insurance companies have a higher risk appetite and compete with each other by lowering premiums to attract more customers.

Yes, insurance premiums are lower in a soft market. This is because insurance companies can afford to lower premiums due to high-dollar reserves and profits made in the stock market.

Yes, there can be high insurance losses during soft markets. Since insurance companies are more lenient about the level of risk they will accept, large-scale losses from natural disasters can put a strain on their finances.

Examples of large-scale losses that can affect insurance companies during soft markets include hurricanes, wildfires, and other natural catastrophes.

When faced with high insurance losses during a soft market, insurance companies may be driven out of business or forced to sharply raise premiums to recover from the losses. This can lead to a hardening of the insurance market, with insurers becoming more risk-averse and selective about their customers.

![By Brad Meltzer - The Fifth Assassin (Reissue) (2015-06-10) [Mass Market Paperback]](https://m.media-amazon.com/images/I/51FC5e5mxHL._AC_UL320_.jpg)