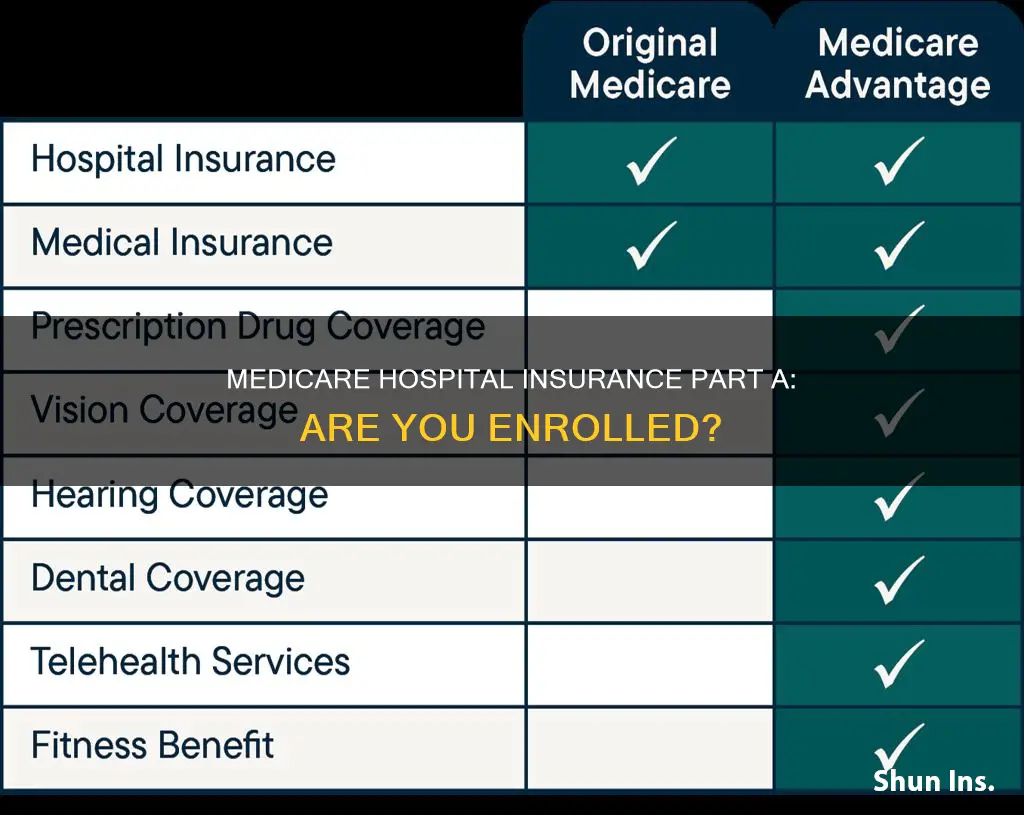

Medicare Part A, also known as Hospital Insurance, is one of the two parts of Original Medicare, the other being Part B or Medical Insurance. Medicare Part A helps cover inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. Most people get Part A for free, but some have to pay a premium for this coverage. Individuals who are already receiving Social Security or Railroad Retirement Board (RRB) benefits at least four months before becoming eligible for Medicare and residing in the United States are automatically enrolled in premium-free Part A.

| Characteristics | Values |

|---|---|

| Name | Medicare Part A |

| Type | Hospital Insurance |

| Coverage | Inpatient hospital care, skilled nursing facility care, hospice care, home health care |

| Eligibility | Individuals receiving Social Security or RRB benefits, individuals with Lou Gehrig's Disease (ALS), individuals with End-Stage Renal Disease (ESRD) |

| Cost | Free for most people, premium for some |

| Enrollment | Automatic for individuals receiving Social Security or RRB benefits, special enrollment period (SEP) for individuals with ESRD or performing volunteer service outside the US |

| Alternatives | Medicare Advantage Plans, Medicare Supplement Insurance (Medigap) |

Explore related products

What You'll Learn

![]()

Eligibility and enrollment

Medicare Part A is insurance for inpatient hospital care, skilled nursing, and hospice. Most people get Part A for free, but some have to pay a premium.

To be eligible for premium-free Part A, you must be entitled to receive Medicare based on your own earnings or those of a spouse, parent, or child. To receive premium-free Part A, you must have a specified number of quarters of coverage (QCs) and file an application for Social Security or Railroad Retirement Board (RRB) benefits. The exact number of QCs required depends on whether you are filing for Part A based on age, disability, or End-Stage Renal Disease (ESRD).

If you begin receiving Social Security retirement benefits between age 62 and up to 4 months before turning 65, you will be automatically enrolled in Medicare Part A and Part B when you turn 65. If you apply for Social Security 3 months before you turn 65 or later, you can sign up for Medicare when you apply for Social Security. The Initial Enrollment Period to sign up for Medicare begins 3 months before you turn 65 and ends 3 months after the month you turn 65—a total of 7 months. You may have to pay a penalty if you miss your Initial Enrollment Period.

If you are under 65, you may be eligible to get Medicare earlier if you have a disability, ESRD, or Lou Gehrig's Disease (ALS). If you have ESRD, you can learn about Medicare coverage and enrollment on the Medicare website. If you have ALS, you will receive Medicare Parts A and B immediately when you enroll in Social Security disability benefits. If you are 65 or older, you can enroll online for Parts A and B, or Part A only.

Individuals who do not enroll in premium Part A when first eligible because they were performing volunteer service outside of the United States for at least 12 months on behalf of a tax-exempt organization and had health insurance that provided coverage for the duration of their volunteer service may enroll using a Special Enrollment Period (SEP). The SEP is a 6-month period that begins the earlier of the first day of the month following the month for which the individual was no longer serving as a volunteer outside of the United States.

Disability Insurance: Medical or Not?

You may want to see also

Explore related products

![]()

Inpatient hospital care

Medicare Part A, also known as hospital insurance, covers inpatient hospital care when you are formally admitted. This includes inpatient care received as part of a qualifying clinical research study. To be considered inpatient hospital care, you must be formally admitted to a hospital by a physician.

Medicare Part A covers inpatient care in hospitals, critical access hospitals, and skilled nursing facilities. It also helps cover hospice care, nursing home care, and some home health care services. A benefit period begins on the day you are admitted to a hospital as an inpatient and ends once you have been out of the hospital for 60 days in a row. With each new benefit period, you pay a new deductible. After day 60, you will pay a daily hospital coinsurance.

Most people get Part A for free, but some have to pay a premium. To be eligible for premium-free Part A, an individual must be entitled to receive Medicare based on their own earnings or those of a spouse, parent, or child. To receive premium-free Part A, the worker must have a specified number of quarters of coverage (QCs) and file an application for Social Security or Railroad Retirement Board (RRB) benefits.

If you begin receiving Social Security retirement benefits between age 62 and up to 4 months before turning 65, you will be automatically enrolled in Medicare Part A when you turn 65. If you apply for Social Security 3 months before you turn 65 or later, you can sign up for Medicare when you apply for Social Security. The Initial Enrollment Period to sign up for Medicare begins 3 months before you turn 65 and ends 3 months after the month you turn 65—a total of 7 months. You may have to pay a penalty if you miss your Initial Enrollment Period.

If you have Lou Gehrig's Disease (ALS), you will receive Medicare Parts A and B immediately when you enroll in Social Security disability benefits. Individuals who do not enroll in Part A when first eligible because they were performing volunteer service outside of the United States for at least 12 months on behalf of a tax-exempt organization and had health insurance that provided coverage during that time may enroll using a Special Enrollment Period (SEP). The SEP is a 6-month period that begins the earlier of the first day of the month following the month for which the individual was no longer serving as a volunteer outside of the United States.

Keep Medical Bills and Insurance Documents for Seven Years

You may want to see also

Explore related products

![]()

Hospice care

Medicare Part A and Part B are available to individuals who are aged 65 or above. Most people get Part A for free, but some have to pay a premium for this coverage. Medicare Part A helps pay for inpatient care in hospitals, critical access hospitals, and skilled nursing facilities. It also helps cover hospice care and some home health care.

Medicare Part A covers the cost of hospice care facilities to give caregivers a short break, known as respite care. Medicare Part B covers outpatient medical and nursing services, medical equipment, and other treatment services. Medicare Part C (Medicare Advantage Plans) is a private insurance option that covers hospital and medical costs. Medicare Advantage is an alternative to traditional Medicare offered by private health insurers. It covers the same benefits as Medicare Part A and Part B.

Medicare Part D may cover the cost of medications if Part A denies coverage for any reason. A Medicare Advantage plan may cover the cost of any additional comfort or support medications or treatment that Part A does not already cover. Medigap may help cover the cost of deductibles or other non-covered costs, but it does not specifically cover long-term care costs.

Get Medical Insurance in Vermont: A Step-by-Step Guide

You may want to see also

Explore related products

![Red Cliff International Version - Part I & Part II [Blu-ray]](https://m.media-amazon.com/images/I/71AI77pz2JL._AC_UY218_.jpg)

![]()

Enrollment periods

When you turn 65, you have a seven-month window to enroll in Medicare Part A and Part B. This window is known as the Initial Enrollment Period and includes the three months before the month you turn 65, your birth month, and the three months after you turn 65. If you are already receiving Social Security benefits, you will be automatically enrolled in Original Medicare (Part A and Part B). If you are aged 65 or older and receive Social Security benefits, you will be automatically enrolled in Part A. Part A coverage begins up to 6 months before the month you apply if you are over 65.

If you miss your Initial Enrollment Period, you may have to wait to sign up and pay a monthly late enrollment penalty for as long as you have Part B coverage. The penalty increases the longer you wait. After your Initial Enrollment Period ends, you can only sign up for Part B and premium Part A during one of the other enrollment periods.

The General Enrollment Period is between January 1 and March 31 each year. Your coverage begins the month after you sign up, and you may have to pay a monthly late enrollment penalty.

The Special Enrollment Period is for unique situations, such as if you were performing volunteer service outside of the United States for at least 12 months and had health insurance coverage during that time. The SEP is a 6-month period that begins the earlier of the first day of the month following the month for which the individual was no longer serving as a volunteer outside of the United States.

You can also make changes to your Medicare Advantage and Medicare drug coverage when certain life events happen, such as if you move or lose other coverage. These changes can be made during Special Enrollment Periods. If you qualify for multiple Special Enrollment Periods, you can use more than one at the same time.

During Medicare’s Annual Enrollment Period, which runs from October 15 to December 7, anyone can make changes to their coverage and enroll in a Medicare plan. If you make a change during this period, your new coverage will begin on January 1.

Caltech's Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Medicare Advantage Plans

There are several types of Medicare Advantage Plans, including Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Special Needs Plans (SNPs), Medicare Medical Savings Accounts (MSAs), and Private Fee-for-Service Plans (PFFS). These plans may vary in their specific benefits and costs, and it's important to review the details of each plan before enrolling.

When considering a Medicare Advantage Plan, it's important to keep a few things in mind. Firstly, these plans are typically only available in certain counties or states, so it's important to verify the service area of the plan. Additionally, eligibility for Medicare Advantage Plans is based on having both Part A and Part B of Medicare. If you move outside the plan's service area, lose Medicare or Medicaid eligibility, or if the plan's contract with Medicare ends, you may be disenrolled from the Medicare Advantage Plan. In such cases, there is a grace period during which you are eligible for a Special Enrollment Period, allowing you to explore other options to ensure continued coverage.

Before enrolling in a Medicare Advantage Plan, it's recommended to consult your employer, union, or benefits administrator to understand how it might affect your existing coverage. Additionally, you can only join, switch, or drop a Medicare Advantage Plan during specific enrollment periods. If you are new to Medicare or considering changing your coverage options, it's essential to familiarize yourself with the different types of plans available, their costs, and the rules they must follow.

Understanding Your Medical Insurance: Summary of Benefits

You may want to see also

Frequently asked questions

Medicare Part A is an insurance plan that covers inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. Most people get Part A for free, but some have to pay a premium.

Individuals who are 65 or older, or those who are under 65 with certain disabilities or conditions, are eligible for Medicare Part A. People who are already receiving Social Security or RRB benefits at least four months before becoming eligible for Medicare and residing in the United States (except Puerto Rico) are automatically enrolled in premium-free Part A.

If you begin receiving Social Security retirement benefits between the age of 62 and up to four months before turning 65, you will be automatically enrolled in Medicare Part A when you turn 65. If you apply for Social Security three months before you turn 65 or later, you can sign up for Medicare when you apply for Social Security.

Medicare Part A (Hospital Insurance) covers inpatient hospital care, while Medicare Part B (Medical Insurance) covers doctors' services and tests, and preventive services.

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)