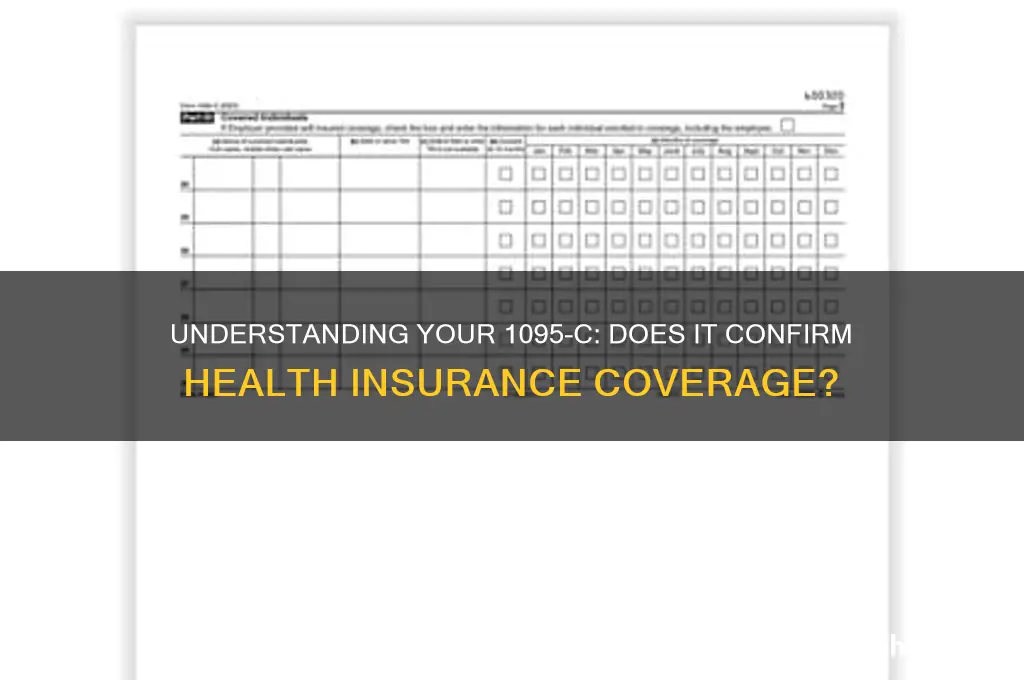

If you received a 1095-C form, it indicates that you were offered health insurance through your employer, but it doesn’t necessarily confirm whether you actually enrolled in the plan. The 1095-C is used by employers with 50 or more full-time employees to report health coverage offers and enrollment details to the IRS. To determine if you had health insurance, review Part II of the form, which shows whether you were enrolled in the employer’s plan. If this section is marked as “Yes,” you likely had health insurance through your employer. However, if it’s marked “No,” you may not have been covered, though you could still have insurance through another source, such as a spouse’s plan or individual coverage. Always verify your coverage status directly with your employer or insurance provider for accurate information.

Explore related products

What You'll Learn

- Understanding Form 1095-C: Details employer-provided health insurance offers and coverage periods

- Minimum Essential Coverage: Confirms if the plan meets ACA requirements for health insurance

- Employee Responsibility: Explains how to verify if you enrolled in the offered plan

- Reporting to the IRS: Shows how 1095-C is used for tax filing purposes

- No Insurance If Declined: Clarifies that declining the offer means no health insurance coverage

![]()

Understanding Form 1095-C: Details employer-provided health insurance offers and coverage periods

Receiving a Form 1095-C from your employer doesn't automatically mean you had health insurance. This form, required by the Affordable Care Act (ACA), primarily serves as proof that your employer offered you health coverage, not that you enrolled in it. Think of it as a snapshot of the options presented to you, not a confirmation of your personal coverage status.

Understanding the Nuances:

The 1095-C breaks down the specifics of the health insurance plans your employer made available during the tax year. It details the coverage period, the minimum value of the plan (a benchmark for affordability), and whether the plan met the ACA's "minimum essential coverage" requirements. This information is crucial for both you and the IRS to determine if you met the individual mandate for having health insurance.

Decoding the Form:

Pay close attention to Part II of the 1095-C. This section outlines the months during which coverage was offered to you and any dependents. A checkmark in a month indicates an offer of coverage for that period. However, it doesn't confirm your enrollment. You'll need to cross-reference this with your own records, such as pay stubs showing insurance deductions or enrollment confirmation documents from your employer.

Implications for Your Taxes:

If your 1095-C shows an offer of affordable, minimum essential coverage for the entire year, and you chose not to enroll, you might face a tax penalty for not having insurance. However, if the offered coverage was unaffordable based on your income, or if you had coverage through another source (like a spouse's plan or Medicaid), you may be exempt from the penalty.

Taking Action:

Don't let the 1095-C leave you guessing about your insurance status. If you're unsure about your coverage, contact your employer's HR department for clarification. They can provide enrollment records and help you understand the specifics of the plans offered. Remember, the 1095-C is a starting point, not the final word on your health insurance situation.

Unvaccinated Premiums: Will Insurance Rates Rise Without Vaccination?

You may want to see also

Explore related products

![Life and Health Insurance License Exam Secrets Study Guide - Full-Length Practice Test, Detailed Answer Explanations: [2nd Edition]](https://m.media-amazon.com/images/I/71DEXPA5yHL._AC_UL320_.jpg)

![]()

Minimum Essential Coverage: Confirms if the plan meets ACA requirements for health insurance

Receiving a 1095-C form from your employer confirms that you were offered health insurance, but it doesn’t automatically mean you had Minimum Essential Coverage (MEC) under the Affordable Care Act (ACA). MEC is the baseline standard for health plans to qualify as adequate insurance, ensuring they cover essential health benefits like hospitalization, emergency care, maternity care, and preventive services. If your plan meets MEC requirements, you’ve fulfilled the ACA’s individual mandate and avoided potential penalties. However, not all employer-sponsored plans meet this threshold, so it’s critical to verify the details of your coverage.

To determine if your plan qualifies as MEC, review the 1095-C form for Part II, which indicates whether the offered coverage was affordable and provided minimum value. A plan provides minimum value if it covers at least 60% of expected medical costs. For example, if your plan includes comprehensive benefits like doctor visits, prescription drugs, and mental health services, it likely meets MEC standards. Conversely, limited-scope dental or vision plans, or those with high out-of-pocket costs and narrow networks, may fall short. Cross-reference the plan’s Summary of Benefits and Coverage (SBC) with the ACA’s MEC criteria to ensure alignment.

Employers often design health plans to meet MEC requirements, but gaps can exist, especially in part-time or seasonal roles. For instance, a plan might exclude certain age groups, like dependents over 26, or cap annual benefits, which could disqualify it from MEC status. If you’re unsure, contact your employer’s HR department or consult a tax professional. Tools like the IRS’s MEC checklist can also help clarify whether your coverage complies with ACA standards.

Failing to have MEC can result in tax penalties unless you qualify for an exemption. Common exemptions include financial hardship, short coverage gaps (less than three months), or religious conscience objections. If your 1095-C indicates non-MEC coverage, consider purchasing a qualifying plan through the Health Insurance Marketplace during open enrollment or a special enrollment period. Proactive verification ensures compliance and avoids unexpected financial consequences.

In summary, a 1095-C form is a starting point, not a guarantee of MEC. Scrutinize the plan’s benefits, consult available resources, and take corrective action if necessary. Understanding MEC isn’t just about tax compliance—it’s about ensuring you have the coverage you need to protect your health and financial well-being.

Term vs. Medical Insurance: What's the Difference?

You may want to see also

Explore related products

![]()

Employee Responsibility: Explains how to verify if you enrolled in the offered plan

Receiving a 1095-C form confirms your employer offered health insurance, but it doesn't automatically mean you enrolled. This distinction is crucial for understanding your tax obligations and ensuring you have the coverage you need.

Step 1: Scrutinize the 1095-C

Your 1095-C, provided by your employer, contains key details. Part II, lines 14-16, are your starting point. Line 14 indicates if you were offered coverage, while line 15 specifies if you enrolled. If line 15 is marked "Yes," you were enrolled in the employer-sponsored plan. Line 16 details the months you were covered.

If line 15 is marked "No," proceed to the next steps.

Step 2: Consult Your Pay Stubs

Pay stubs often reveal deductions for health insurance premiums. Look for a line item labeled "Health Insurance," "Medical," or something similar. Consistent deductions throughout the year strongly suggest enrollment.

Keep in mind, some employers may use different terminology or lump deductions together. If you're unsure, contact your payroll department for clarification.

Step 3: Review Your Plan Documents

Your employer should have provided you with a Summary Plan Description (SPD) outlining the details of the offered health plan. This document will include information on enrollment procedures, coverage details, and contact information for the plan administrator. If you can't locate your SPD, request a copy from your HR department.

Caution: Don't rely solely on verbal assurances from coworkers or even HR representatives. Written documentation is essential for verification.

Step 4: Contact Your Insurance Provider

If you're still unsure, contact the insurance company directly. Provide them with your name, employer information, and any policy numbers you may have. They can confirm your enrollment status and provide details about your coverage.

Verifying your enrollment in an employer-sponsored health plan is your responsibility. By carefully reviewing your 1095-C, pay stubs, plan documents, and contacting your insurance provider if needed, you can ensure you have the accurate information necessary for tax purposes and peace of mind regarding your healthcare coverage. Remember, proactive verification is key to avoiding potential issues down the line.

Medical Insurance: A Legal Obligation or Personal Choice?

You may want to see also

Explore related products

![]()

Reporting to the IRS: Shows how 1095-C is used for tax filing purposes

The 1095-C form is a critical document for both employers and employees when it comes to reporting health insurance coverage to the IRS. If you’ve received a 1095-C, it means your employer is confirming whether they offered you health insurance that meets the Affordable Care Act (ACA) standards. This form is not just a piece of paperwork; it directly impacts your tax filing, particularly in proving compliance with the ACA’s individual mandate. Understanding how the 1095-C is used in tax reporting can help you avoid penalties and ensure accurate filings.

When filing taxes, the 1095-C serves as proof of employer-sponsored health insurance coverage. Part II of the form details the months you were eligible for coverage and whether you enrolled. The IRS uses this information to verify that you, as an individual, had access to affordable, minimum essential coverage. For example, if Line 14 of the 1095-C indicates you were offered coverage all 12 months, it supports your claim of having insurance for the entire year. Conversely, gaps in coverage or unaffordable offers may trigger further scrutiny or penalties.

One common misconception is that receiving a 1095-C automatically means you had health insurance. However, the form only confirms that your employer offered it—not that you accepted it. If you declined the offer, you’ll need to explore other coverage options or qualify for an exemption to avoid the ACA penalty. For instance, if your employer’s plan cost more than 9.5% of your household income, Line 16 of the 1095-C would indicate this, potentially exempting you from penalties if you remained uninsured.

To use the 1095-C effectively during tax filing, start by reviewing it for accuracy. Ensure the months of coverage align with your records and that the affordability calculations are correct. If discrepancies exist, contact your employer immediately for a corrected form. When completing Form 8962 (Premium Tax Credit) or Form 1040, reference the 1095-C to confirm your coverage status. For example, if you received a premium tax credit through the Marketplace, the 1095-C helps reconcile whether you maintained eligible coverage throughout the year.

Finally, retain your 1095-C with your tax records, as the IRS may request it during audits or inquiries. While you don’t need to attach it to your tax return, having it on hand ensures you can quickly address any questions about your health insurance status. By understanding the 1095-C’s role in tax reporting, you can navigate the complexities of ACA compliance with confidence and accuracy.

Insurance Medical Bill Claims: How Long Do You Have?

You may want to see also

Explore related products

![]()

No Insurance If Declined: Clarifies that declining the offer means no health insurance coverage

Receiving a 1095-C form doesn't automatically mean you had health insurance. This form simply confirms that your employer offered you coverage, not that you accepted it. Declining that offer, even if documented on the 1095-C, leaves you without employer-sponsored health insurance.

Imagine this scenario: Your employer provides a comprehensive health plan, but you opt out, believing you're young and healthy. A surprise medical emergency lands you with hefty bills. The 1095-C won't shield you from these expenses; it merely serves as proof of the offer, not your enrollment.

Key Takeaway: The 1095-C is a record of an offer, not a guarantee of coverage. Declining the offer explicitly means you lack employer-provided health insurance.

Let's break down the implications. Declining employer-sponsored insurance can have significant consequences. You may face penalties for not having minimum essential coverage under the Affordable Care Act (ACA). Additionally, you'll be responsible for all medical costs, potentially leading to financial hardship.

Practical Tip: If you decline employer-sponsored insurance, explore alternative options like purchasing a plan through the Health Insurance Marketplace or a private insurer. Carefully consider your health needs and budget to ensure you have adequate coverage.

Top Pregnancy Insurance Providers: A Comprehensive Guide for Expecting Parents

You may want to see also

Frequently asked questions

A 1095-C form is provided by employers with 50 or more full-time employees to report health insurance offers and coverage. Receiving a 1095-C does not automatically mean you have health insurance; it only indicates that your employer offered you coverage. You must check Part II of the form to see if you enrolled in the plan.

No, if you did not enroll in your employer’s health insurance plan, you do not have coverage through them, even if you received a 1095-C. The form only confirms that the offer was made, not that you accepted it.

If your employer offered you affordable, minimum essential coverage (as reported on the 1095-C), and you enrolled in it, then you meet the ACA’s individual mandate. If you declined the offer, you may need to obtain coverage elsewhere or face a penalty (if applicable in your state).

Yes, if you enrolled in your employer’s health insurance plan, the 1095-C serves as proof of coverage for tax purposes. You’ll need it when filing your taxes to show compliance with the ACA’s individual mandate.

If you had health insurance through another source, the 1095-C from your employer is still relevant for reporting purposes. You’ll need to report all sources of coverage when filing taxes, but the 1095-C only pertains to the offer and enrollment through your employer.