Not having health insurance for three months can be a stressful and potentially risky situation, leaving individuals vulnerable to unexpected medical expenses and limited access to necessary healthcare services. During this gap in coverage, routine check-ups, prescriptions, and emergency care may become unaffordable or inaccessible, potentially exacerbating existing health issues or delaying critical treatments. This period of uninsured status often highlights the importance of continuous coverage and the need for affordable healthcare options, as even a short lapse can have significant financial and health-related consequences.

| Characteristics | Values |

|---|---|

| Prevalence in the U.S. (2022) | Approximately 8.5% of the population was uninsured at any point in 2022. |

| Common Reasons for Uninsured Periods | Job loss, transition between jobs, affordability issues, or policy gaps. |

| Financial Impact | Average out-of-pocket cost for a 3-month uninsured period: $1,200–$3,000. |

| Health Risks | Delayed preventive care, untreated conditions, and higher mortality rates. |

| Legal Implications (U.S.) | No federal penalty for short-term uninsured periods since 2019. |

| Access to Care | Limited access to primary care, specialists, and prescription medications. |

| Demographics Most Affected | Low-income individuals, part-time workers, and young adults (18–34). |

| Short-Term Insurance Options | Short-term health plans (up to 3 months) with limited coverage. |

| Reinstatement Options | Special Enrollment Period (SEP) for ACA plans if qualifying life event. |

| Long-Term Consequences | Accumulated medical debt, worsened health outcomes, and higher premiums. |

Explore related products

What You'll Learn

![]()

Loss of employer-sponsored coverage

Losing employer-sponsored health insurance can feel like falling off a cliff, especially if you’re unprepared. This scenario often occurs during job transitions, layoffs, or reductions in work hours, leaving individuals with a sudden gap in coverage. For those who’ve relied on their employer’s plan, the shock of losing it can be compounded by the complexity of navigating alternatives. The Consolidated Omnibus Budget Reconciliation Act (COBRA) allows you to continue your employer’s plan temporarily, but at full cost, which can be prohibitively expensive. Understanding your options within the 60-day window after job loss is critical to avoiding a 3-month coverage gap.

Consider the case of a 35-year-old marketing professional who was laid off unexpectedly. Without a new job lined up, she faced a 3-month gap in insurance. She initially opted for COBRA but quickly realized the $600 monthly premium was unsustainable. Instead, she turned to the Health Insurance Marketplace, where she qualified for a subsidized plan with a $250 deductible and $40 monthly premium. Her story highlights the importance of comparing costs and eligibility for subsidies, which can significantly reduce out-of-pocket expenses during a coverage lapse.

If you’re in this situation, act fast but strategically. First, assess your financial health and anticipated healthcare needs. If you’re generally healthy and under 30, a short-term health plan might suffice, though these plans often exclude pre-existing conditions and preventive care. For those with chronic conditions or dependents, a Marketplace plan is likely the better option. Use the Healthcare.gov calculator to estimate subsidies based on your income. For instance, a single individual earning $30,000 annually might qualify for a plan with a $0 premium after subsidies.

Beware of common pitfalls. Short-term plans may seem affordable, but they often leave you vulnerable to high costs if you need significant care. COBRA, while comprehensive, can drain savings quickly. Additionally, missing the Marketplace special enrollment period (60 days after job loss) could lock you out of affordable options until the next open enrollment. Pro tip: Set reminders for key deadlines and keep documentation of your job loss, as you’ll need it to prove eligibility for special enrollment.

In conclusion, losing employer-sponsored coverage doesn’t have to mean 3 months without insurance. By understanding your options, acting quickly, and leveraging available resources, you can bridge the gap affordably. Whether through COBRA, the Marketplace, or a short-term plan, the key is to avoid going uninsured, as the financial and health risks far outweigh the temporary costs of maintaining coverage.

When Are Medical Insurance Premiums Due?

You may want to see also

Explore related products

![]()

Affording premiums during unemployment

Unemployment often forces individuals to make difficult financial choices, and health insurance premiums can feel like a luxury when income is scarce. During a three-month gap in employment, affording coverage becomes a critical concern, especially for those with pre-existing conditions or dependents. The average monthly premium for an individual ACA marketplace plan in 2023 was $456, a significant burden without a steady paycheck.

Step 1: Explore Subsidized Options

Immediately investigate government-subsidized plans through Healthcare.gov or your state’s marketplace. Under the Affordable Care Act, individuals earning up to 400% of the federal poverty level ($54,360 for a single person in 2023) may qualify for premium tax credits. For example, a 30-year-old earning $30,000 annually could pay as little as $100/month for a benchmark plan. Unemployment also triggers a Special Enrollment Period, allowing you to enroll outside the typical open enrollment window.

Caution: Avoid Short-Term Plans

Short-term health insurance plans, while cheaper (often $100–$200/month), exclude pre-existing conditions and essential benefits like maternity care or prescription drugs. These plans can leave you underinsured during a critical period. Instead, prioritize ACA-compliant plans that offer comprehensive coverage, even if they require a higher premium.

Step 2: Leverage COBRA as a Temporary Bridge

If you recently lost employer-sponsored insurance, COBRA allows you to continue your existing plan for up to 18 months. However, you’ll pay the full premium plus a 2% administrative fee—typically $700–$1,000/month for individual coverage. While costly, COBRA ensures continuity of care, which is vital if you’re undergoing treatment or have specialists within your network.

Comparative Analysis: COBRA vs. ACA

For a 40-year-old in Texas, COBRA might cost $800/month, while an ACA silver plan with subsidies could be $200/month. Unless your employer’s plan is uniquely beneficial, ACA plans often provide better value during unemployment.

Step 3: Negotiate Payment Plans or Hardship Exemptions

Contact your insurer directly to discuss payment flexibility. Some companies offer deferred payment plans or reduced premiums for individuals facing financial hardship. Additionally, if your income drops below the poverty line, you may qualify for a hardship exemption, waiving the penalty for not having insurance.

Takeaway: Proactive Planning Minimizes Risk

Understanding Tax Exemptions for Pre-Tax Medical Insurance

You may want to see also

Explore related products

![]()

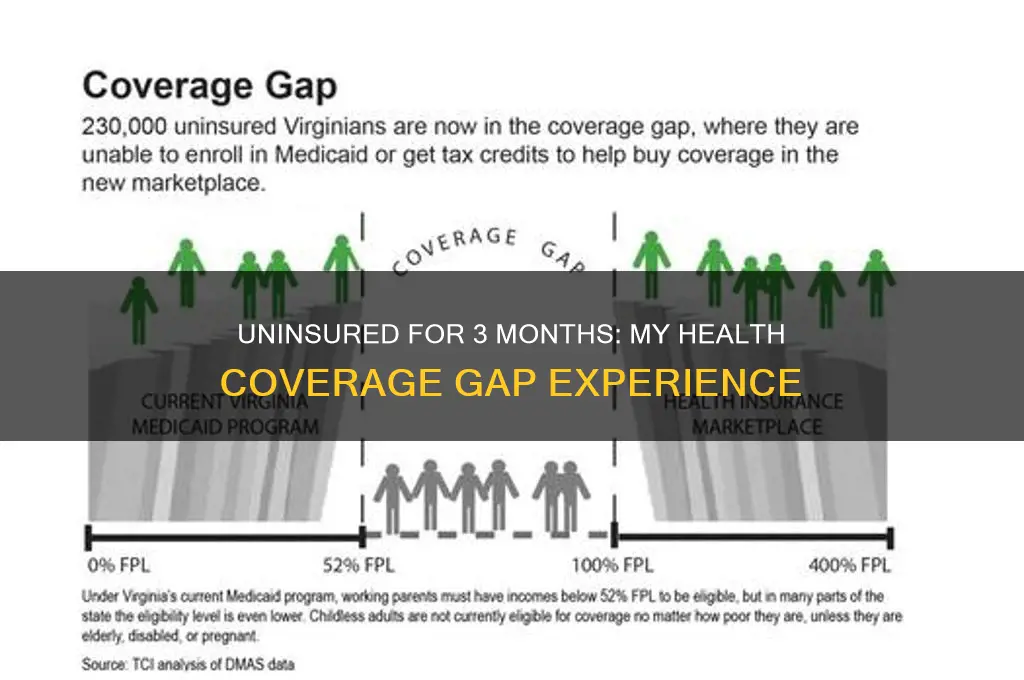

Gaps in Medicaid eligibility

Millions of Americans fall into the Medicaid gap, earning too much to qualify for traditional Medicaid but too little to afford private insurance. This gap is a direct result of the decision by some states not to expand Medicaid under the Affordable Care Act. In these states, individuals with incomes above the traditional Medicaid threshold but below the federal poverty level (FPL) are left without affordable coverage options. For example, in Texas, a single adult with an income of $5,000 annually—just 44% of the FPL—would not qualify for Medicaid and likely couldn’t afford marketplace plans, leaving them uninsured.

Consider the case of Sarah, a 32-year-old part-time worker in Florida earning $12,000 a year. She doesn’t qualify for Medicaid because her state hasn’t expanded it, and she can’t afford the $200 monthly premium for the cheapest marketplace plan. When she developed a severe tooth infection, she faced a $1,500 emergency room bill, forcing her to choose between medical debt and basic needs like rent and food. This scenario highlights how gaps in Medicaid eligibility create financial and health crises for low-income individuals.

To navigate this gap, individuals should first check if their state has expanded Medicaid using the Healthcare.gov tool. If not, explore local clinics offering sliding-scale fees or free services for uninsured patients. For instance, Federally Qualified Health Centers (FQHCs) provide care based on income, often charging as little as $20 per visit. Additionally, prescription assistance programs like RxAssist can reduce medication costs by up to 75%. While these solutions aren’t perfect, they offer temporary relief until broader policy changes occur.

Advocacy is another critical step. Contact state legislators to support Medicaid expansion, as seen in Missouri and Oklahoma, where voter-led initiatives successfully expanded coverage. Share personal stories to humanize the issue—data shows policymakers are more likely to act when constituents share real-life consequences of the Medicaid gap. Organizations like the Center on Budget and Policy Priorities provide templates for effective advocacy letters and talking points to strengthen your case.

In conclusion, the Medicaid gap is a solvable problem, but it requires both individual resourcefulness and collective action. Until expansion becomes universal, uninsured individuals must leverage available tools while pushing for systemic change. Sarah’s story isn’t unique—it’s a call to action for a healthcare system that leaves no one behind.

Travel Insurance: Pre-Existing Medical Conditions Covered?

You may want to see also

Explore related products

![]()

Transitioning between insurance plans

Gaps in health insurance coverage, even as brief as three months, can create significant challenges when transitioning between plans. Understanding the nuances of this process is crucial to avoid disruptions in care and unexpected costs. Here’s a practical guide to navigating this transition effectively.

Step 1: Understand Your Coverage Gap

Begin by identifying why you’re transitioning—job change, aging off a parent’s plan, or COBRA expiration. For example, if you’re switching from an employer-sponsored plan to an individual market plan, know that the Affordable Care Act (ACA) allows a 60-day special enrollment period (SEP) after losing coverage. However, if you’re between plans due to a voluntary resignation without immediate alternatives, you may face a gap unless you qualify for Medicaid or short-term health insurance. Short-term plans, while cheaper, often exclude pre-existing conditions and preventive care, so weigh the risks carefully.

Step 2: Bridge the Gap Strategically

If a gap is unavoidable, consider short-term health insurance as a temporary solution. These plans typically last 1–12 months and can cost as little as $100/month for a healthy 30-year-old. However, they rarely cover prescriptions, mental health, or maternity care. Alternatively, explore health-sharing ministries like Liberty HealthShare, which pool member contributions to cover medical expenses. While not insurance, they offer a faith-based alternative with monthly shares starting at $130. Always verify if your preferred providers accept these options.

Step 3: Coordinate Timing with New Coverage

To minimize uncovered days, align your new plan’s start date with the end of your current coverage. For instance, if your employer plan ends on the 15th, request your new ACA plan to begin on the 1st of the following month. Use Healthcare.gov’s SEP to enroll outside the annual open enrollment period. If you’re over 65, Medicare Part B enrollment requires careful timing—sign up within eight months of losing employer coverage to avoid lifelong penalties.

Step 4: Manage Prescriptions and Ongoing Care

Gaps can disrupt access to medications. Ask your doctor for 90-day prescriptions or samples before coverage ends. Websites like GoodRx offer discounts on out-of-pocket medications—a 30-day supply of generic Lipitor can drop from $30 to $10. For ongoing treatments, negotiate cash-pay rates with providers; some offer 20–30% discounts for upfront payments. Document all expenses; if you later enroll in an HSA-eligible plan, you can reimburse yourself tax-free.

Cautions and Takeaways

Transitioning without a plan risks accruing medical debt or delaying care. Short-term plans may seem appealing but leave you vulnerable to high out-of-pocket costs for serious conditions. Always compare premiums, deductibles, and network providers before enrolling in a new plan. For those under 30, catastrophic plans offer lower premiums but high deductibles ($8,000+), suitable only if you rarely use healthcare. Finally, consult a broker or navigator to explore all options, including state-specific programs like California’s Covered California, which offers subsidies for incomes up to 600% of the federal poverty level.

By proactively planning, you can mitigate risks and ensure continuous access to care during transitions.

Medical Records: Physical Exams and Insurance Claims

You may want to see also

![]()

Impact on accessing healthcare services

Going without health insurance for three months can create a cascade of barriers to accessing healthcare. Financial concerns become the primary obstacle. Without insurance, individuals face the full brunt of healthcare costs, often leading to delayed or forgone care. A routine doctor's visit, which might cost $150-$250 out-of-pocket, becomes a luxury. Prescription medications, even generics, can easily run into hundreds of dollars per month. This financial burden disproportionately affects low-income individuals and families, forcing them to prioritize basic needs like rent and food over preventative care or treatment for existing conditions.

A 2019 study by the Commonwealth Fund found that 44% of uninsured adults reported problems paying medical bills, compared to only 17% of insured adults. This financial strain often leads to a vicious cycle: untreated conditions worsen, requiring more expensive interventions later.

The impact extends beyond financial hardship. The lack of a consistent healthcare provider disrupts continuity of care. Without insurance, individuals are less likely to have a primary care physician, leading to fragmented care and missed opportunities for early detection and management of chronic conditions. Imagine a 45-year-old woman with a family history of diabetes. Without insurance, she might skip her annual checkup and blood sugar screening, delaying diagnosis and increasing the risk of complications like heart disease and kidney damage.

Furthermore, the absence of insurance limits access to preventive services. Vaccinations, cancer screenings, and routine checkups are crucial for maintaining health and preventing costly illnesses. A 30-year-old man without insurance might forgo a colonoscopy, a potentially life-saving screening for colorectal cancer, due to the high out-of-pocket cost. This lack of preventive care not only jeopardizes individual health but also contributes to higher healthcare costs for society as a whole.

A 2020 study estimated that preventable hospitalizations cost the U.S. healthcare system over $30 billion annually.

While some safety net clinics and community health centers offer services on a sliding scale, they often have long wait times and limited resources. Navigating these systems can be complex and time-consuming, further delaying access to care. For those with acute conditions or chronic illnesses requiring specialized care, the lack of insurance can be particularly devastating.

In conclusion, going without health insurance for even a short period significantly impedes access to healthcare services. It creates financial barriers, disrupts continuity of care, limits preventive measures, and ultimately jeopardizes both individual and public health. Addressing this issue requires systemic solutions that ensure affordable and accessible healthcare for all.

Accident Insurance: How Much Coverage Do You Need?

You may want to see also

Frequently asked questions

If you did not have health insurance for 3 months, you may face a penalty under the Affordable Care Act (ACA) unless you qualify for an exemption. Additionally, you were financially responsible for any medical expenses incurred during that period.

Yes, you can enroll in health insurance after not having it for 3 months, but you may need to wait for the Open Enrollment Period or qualify for a Special Enrollment Period due to a qualifying life event, such as losing coverage or having a change in income.

Not having health insurance for 3 months typically does not affect your future coverage options, but it may impact your eligibility for certain subsidies or exemptions. It’s important to enroll as soon as possible to avoid gaps in coverage.

Yes, there are exemptions for not having health insurance, such as financial hardship, short coverage gaps (less than 3 months in some cases), or qualifying life events. Check with the ACA or your state’s marketplace to see if you qualify for an exemption.