The question of whether President Trump eliminated the health insurance penalty is a significant one, as it directly impacts millions of Americans and the broader healthcare landscape. Under the Affordable Care Act (ACA), individuals were required to have health insurance or face a tax penalty, known as the individual mandate. However, in 2017, as part of the Tax Cuts and Jobs Act, President Trump and the Republican-controlled Congress effectively eliminated this penalty by reducing it to $0 starting in 2019. This change marked a substantial shift in healthcare policy, as it removed a key enforcement mechanism of the ACA, raising questions about its long-term effects on insurance coverage rates, market stability, and the overall accessibility of healthcare in the United States.

| Characteristics | Values |

|---|---|

| Policy Change | President Trump did not directly eliminate the health insurance penalty. |

| Legislation | The penalty was effectively reduced to $0 by the Tax Cuts and Jobs Act of 2017, signed into law by Trump. |

| Effective Date | The penalty reduction took effect starting January 1, 2019. |

| Impact on Individual Mandate | The individual mandate (requirement to have health insurance) remained in place but without financial penalty. |

| State-Level Variations | Some states reinstated their own health insurance penalties after the federal penalty was eliminated. |

| Current Status | As of the latest data, the federal penalty remains at $0, though state penalties may apply in certain states. |

| Political Context | The change was part of broader efforts to dismantle the Affordable Care Act (ACA). |

| Public Reaction | Mixed reactions, with critics arguing it could lead to higher uninsured rates and supporters praising reduced government mandates. |

Explore related products

What You'll Learn

- ACA Mandate Repeal: Trump's Tax Cuts and Jobs Act zeroed out the individual mandate penalty in 2019

- State-Level Penalties: Some states implemented their own penalties to replace the federal mandate

- Impact on Enrollment: Elimination led to slight declines in health insurance sign-ups nationwide

- Legal Challenges: Courts debated the mandate's constitutionality post-penalty removal

- Policy Debate: Critics argued removal increased uninsured rates; supporters cited reduced tax burdens

![]()

ACA Mandate Repeal: Trump's Tax Cuts and Jobs Act zeroed out the individual mandate penalty in 2019

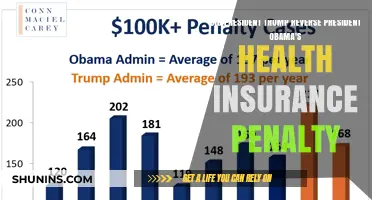

The Tax Cuts and Jobs Act of 2017, signed into law by President Trump, included a provision that effectively eliminated the individual mandate penalty of the Affordable Care Act (ACA) starting in 2019. This penalty, originally designed to encourage Americans to maintain health insurance coverage, was reduced to $0, marking a significant shift in healthcare policy. The move was framed as a way to alleviate financial burdens on individuals who opted not to purchase insurance, but it also raised questions about the potential impact on the broader healthcare market.

From an analytical perspective, zeroing out the individual mandate penalty was a strategic dismantling of a key ACA mechanism. The penalty had been a cornerstone of the ACA’s effort to expand coverage by ensuring a balanced risk pool—healthy individuals offsetting the costs of those with pre-existing conditions. By removing the penalty, the Trump administration aimed to fulfill campaign promises of reducing government mandates. However, critics argued that this change could lead to higher premiums for those remaining in the marketplace, as healthier individuals might opt out of coverage, leaving a sicker and more expensive pool of insured individuals.

For those navigating the post-penalty landscape, understanding the practical implications is crucial. Without the mandate, individuals were no longer required to prove health insurance coverage on their tax returns. This change meant that while there was no federal penalty for being uninsured, some states implemented their own mandates to mitigate potential market disruptions. For example, California, New Jersey, and Massachusetts introduced state-level penalties for lacking coverage. Individuals should check their state’s regulations to avoid unexpected fines and ensure compliance.

Persuasively, the repeal of the penalty reflects a broader ideological debate about personal responsibility versus collective welfare in healthcare. Proponents argue that eliminating the mandate restores individual freedom to choose whether to purchase insurance. Opponents counter that this freedom comes at the expense of destabilizing the insurance market, potentially leading to reduced access and higher costs for those who remain insured. This tension highlights the complexities of balancing individual liberties with systemic stability in healthcare policy.

In conclusion, the zeroing out of the individual mandate penalty in 2019 was a pivotal moment in the evolution of U.S. healthcare policy under President Trump. While it fulfilled a campaign promise and reduced a financial burden for some, it also introduced uncertainties for the insurance market and consumers. Individuals must remain informed about state-level mandates and market trends to navigate this changed landscape effectively. The repeal serves as a case study in the trade-offs between deregulation and the sustainability of healthcare systems.

Why Insurance Companies Require Deposits: Understanding the Financial Logic

You may want to see also

Explore related products

![]()

State-Level Penalties: Some states implemented their own penalties to replace the federal mandate

With the elimination of the federal individual mandate penalty under President Trump's administration, a notable shift occurred in the healthcare landscape. Several states took matters into their own hands, crafting unique penalties to encourage residents to maintain health insurance coverage. This state-level response showcases the diversity of approaches to healthcare policy and the determination of certain states to uphold the principle of shared responsibility.

The Pioneers: States Leading the Charge

A handful of states, including New Jersey, Massachusetts, and California, were among the first to implement their own penalties for residents who failed to secure health insurance. These states recognized the potential consequences of a coverage gap, such as increased premiums and reduced access to care. For instance, California's penalty, which took effect in 2020, is calculated as a percentage of household income, with a minimum penalty of $695 per adult and $347.50 per child, or 2.5% of household income, whichever is greater. This approach not only encourages compliance but also generates revenue to support state-level healthcare initiatives.

A Patchwork of Policies: Variations Across States

The state-level penalties vary significantly in their structure and severity. Some states, like Washington, have opted for a flat fee, while others, such as the District of Columbia, have implemented a percentage-based penalty. In Vermont, the penalty is tied to the state's health insurance exchange, with non-compliant residents facing a surcharge on their state income tax. This diversity highlights the importance of understanding the specific requirements in one's state, as the consequences of non-compliance can differ drastically. For example, in New Jersey, residents who fail to maintain coverage may face a penalty of up to $695 per individual or 2.5% of their household income, whichever is greater.

Compliance and Consequences: What Residents Need to Know

For residents in states with their own penalties, it's crucial to understand the specific requirements and deadlines. In Massachusetts, for instance, the penalty is assessed during tax filing, with residents required to report their health insurance status on their state tax return. Failure to comply can result in a penalty of up to $1,000 per individual. To avoid these penalties, residents should prioritize securing health insurance coverage, either through their employer, a state exchange, or a private insurer. Additionally, staying informed about any changes to state-level policies is essential, as some states may adjust their penalties or requirements over time.

The Broader Impact: State-Level Penalties and Healthcare Access

The implementation of state-level penalties has broader implications for healthcare access and affordability. By encouraging residents to maintain coverage, these penalties can help reduce the number of uninsured individuals, thereby lowering premiums for everyone. Moreover, the revenue generated from these penalties can be used to support state-level healthcare initiatives, such as expanding Medicaid or funding community health programs. However, it's essential to strike a balance between encouraging compliance and ensuring that penalties do not disproportionately burden low-income residents. States must consider exemptions, waivers, or financial assistance programs to help vulnerable populations avoid penalties while still promoting the goal of universal coverage. By doing so, state-level penalties can serve as a vital tool in promoting a healthier, more equitable healthcare system.

Understanding the Importance of Health Insurance for Financial Security

You may want to see also

Explore related products

![]()

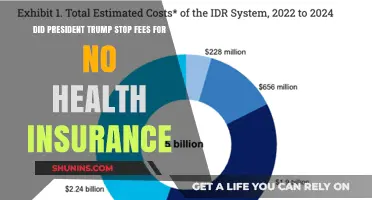

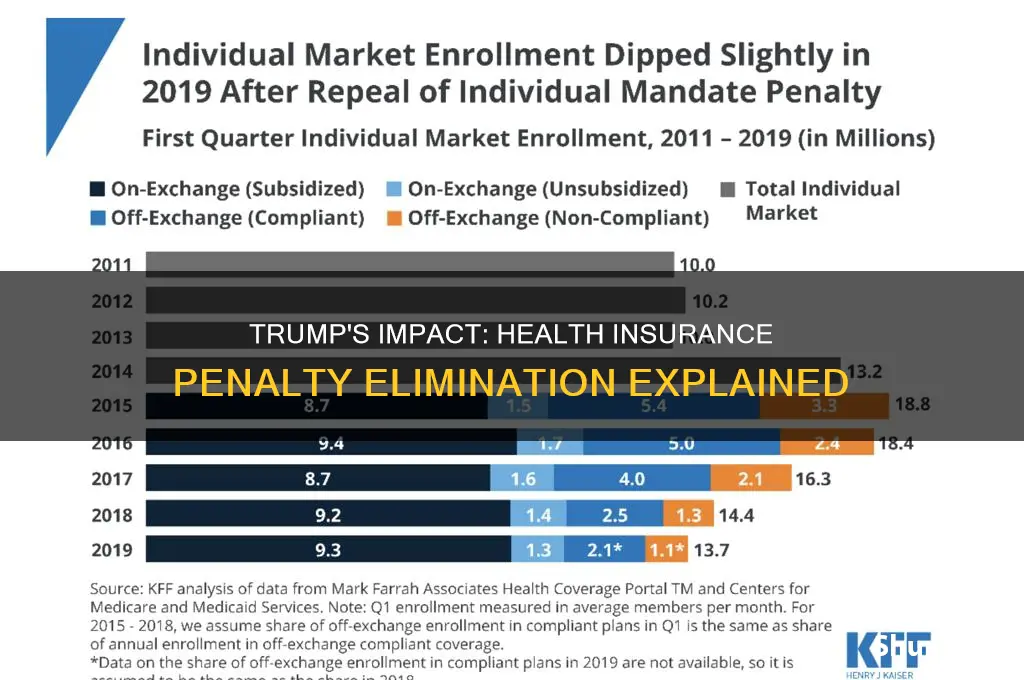

Impact on Enrollment: Elimination led to slight declines in health insurance sign-ups nationwide

The elimination of the health insurance penalty under the Trump administration had a measurable, albeit modest, impact on enrollment numbers across the country. Data from the Centers for Medicare and Medicaid Services (CMS) revealed a 2.3% decline in sign-ups during the first open enrollment period following the penalty’s removal. While this drop may seem insignificant, it translates to hundreds of thousands of individuals opting out of coverage, particularly in states with higher uninsured rates. For instance, Texas and Florida, which already struggled with coverage gaps, saw declines of 4.1% and 3.7%, respectively, highlighting regional disparities in the policy’s effects.

Analyzing the demographics of those who dropped coverage provides further insight. Younger, healthier individuals aged 18–34 were disproportionately represented among those who opted out, accounting for nearly 40% of the decline. This group, often referred to as “young invincibles,” historically viewed the penalty as a financial incentive to enroll. Without it, many chose to forgo coverage, potentially increasing their risk of catastrophic health expenses. Conversely, older adults and families with children showed smaller declines, suggesting that the penalty’s removal had less influence on those with greater perceived health needs.

From a practical standpoint, the slight decline in enrollment has broader implications for both individuals and the healthcare system. For uninsured individuals, the absence of a penalty may offer short-term financial relief but exposes them to higher out-of-pocket costs in the event of illness or injury. For the system, fewer enrollees can lead to a sicker risk pool, as healthier individuals drop out, potentially driving up premiums for those who remain insured. This dynamic underscores the delicate balance between individual choice and collective risk-sharing in health insurance markets.

To mitigate the impact of declining enrollment, states and insurers have implemented creative strategies. Some states, like California and New Jersey, reintroduced their own penalty systems to encourage sign-ups, while others expanded outreach efforts targeting younger demographics. Insurers have also adjusted their marketing tactics, emphasizing the long-term benefits of coverage rather than focusing solely on compliance. For individuals, the takeaway is clear: while the penalty’s elimination provides flexibility, the value of health insurance extends beyond avoiding a fine, offering financial protection and access to preventive care.

In conclusion, the elimination of the health insurance penalty led to slight but significant declines in enrollment, particularly among younger, healthier individuals. While the policy change offered immediate financial relief for some, it also exposed gaps in coverage and heightened risks for both individuals and the broader healthcare system. Understanding these dynamics can help policymakers, insurers, and consumers make informed decisions to ensure access to affordable, comprehensive care.

DACA Recipients and Health Insurance: Eligibility and Coverage Explained

You may want to see also

Explore related products

![]()

Legal Challenges: Courts debated the mandate's constitutionality post-penalty removal

The removal of the health insurance penalty under President Trump's administration sparked a wave of legal challenges, with courts across the nation grappling to determine the constitutionality of the individual mandate in its new form. At the heart of these debates was the question: Can the mandate stand without the tax penalty that previously enforced it? This issue became a critical juncture in the ongoing saga of healthcare reform, pitting legal scholars, judges, and policymakers against one another in a battle of interpretations and ideologies.

The Legal Landscape Shifts

When the Tax Cuts and Jobs Act of 2017 reduced the individual mandate penalty to $0 starting in 2019, the legal foundation of the Affordable Care Act (ACA) was suddenly on shaky ground. Critics argued that without the penalty, the mandate was no longer a valid exercise of Congress’s taxing power, which had been the Supreme Court’s rationale for upholding it in *NFIB v. Sebelius* (2012). Proponents countered that the mandate remained constitutional as a regulatory measure under the Commerce Clause, even without enforcement. This shift set the stage for a series of lawsuits, most notably *Texas v. United States*, where 20 Republican-led states challenged the ACA’s constitutionality post-penalty removal.

The Courts Weigh In

In *Texas v. United States*, a federal district court in Texas ruled in 2018 that the entire ACA was unconstitutional because the mandate, now toothless, could no longer be justified as a tax. This decision was appealed, and in 2021, the Supreme Court dismissed the case on procedural grounds, holding that the plaintiffs lacked standing to challenge the law. However, the Court sidestepped the constitutional question, leaving the door open for future challenges. Other lower courts have since issued conflicting rulings, with some upholding the mandate as severable from the penalty and others questioning its enforceability. This patchwork of decisions underscores the complexity of the issue and the lack of a clear legal consensus.

Practical Implications for Individuals

For consumers, the legal uncertainty surrounding the mandate’s constitutionality has created confusion. While the penalty was eliminated, the requirement to have health insurance technically remains in place in some states that have enacted their own mandates. For example, states like California, New Jersey, and Massachusetts impose penalties for uninsured residents, while others have no such requirement. Individuals must stay informed about their state’s laws to avoid unexpected fines. Additionally, the absence of a federal penalty has led to a slight decline in insurance enrollment, raising concerns about the stability of the individual market and the potential for higher premiums for those who remain insured.

The Broader Takeaway

The legal challenges to the mandate post-penalty removal highlight the fragility of healthcare policy in the face of political and judicial shifts. While the Supreme Court’s dismissal of *Texas v. United States* preserved the ACA for the time being, the underlying constitutional questions remain unresolved. Policymakers and advocates must navigate this uncertain terrain, balancing the need for accessible healthcare with the legal constraints imposed by the courts. For now, the mandate stands, but its future hinges on the outcome of potential future challenges and the evolving interpretations of constitutional law.

Informed Insurance: Accidents and Notifications

You may want to see also

![]()

Policy Debate: Critics argued removal increased uninsured rates; supporters cited reduced tax burdens

The elimination of the health insurance penalty under President Trump's administration sparked a heated policy debate, with critics and supporters presenting starkly contrasting views. At the heart of this debate was the individual mandate, a key provision of the Affordable Care Act (ACA) that required most Americans to have health insurance or pay a penalty. When the Tax Cuts and Jobs Act of 2017 reduced this penalty to $0 starting in 2019, the move was both celebrated and condemned, depending on the perspective. Critics swiftly argued that removing the penalty would lead to higher uninsured rates, as the mandate had been a critical tool in encouraging enrollment. Supporters, however, countered that the penalty’s removal alleviated an unnecessary financial burden on individuals and families, particularly those who found insurance premiums unaffordable.

To understand the critics’ stance, consider the mandate’s role in stabilizing the insurance market. By requiring healthy individuals to enroll, the mandate helped balance the risk pool, preventing premiums from skyrocketing for those with pre-existing conditions. When the penalty was eliminated, enrollment in ACA marketplaces declined by approximately 2.5 million people between 2017 and 2019, according to the Centers for Medicare & Medicaid Services. Critics pointed to this drop as evidence that the penalty’s removal directly contributed to rising uninsured rates, particularly among younger, healthier individuals who might forgo coverage without a financial incentive. For example, the uninsured rate among 18- to 24-year-olds increased by 2.2 percentage points from 2017 to 2019, a demographic shift that aligned with predictions.

Supporters of the penalty’s removal, however, framed it as a matter of financial freedom and relief from government overreach. They argued that the mandate disproportionately penalized low-income individuals who could not afford insurance premiums, even with subsidies. For instance, a family of four earning $50,000 annually might face premiums exceeding $12,000 per year, leaving them with a difficult choice: pay the penalty or go without coverage. By eliminating the penalty, supporters claimed, these families were no longer forced to choose between healthcare and other essential expenses like rent or groceries. This perspective resonated with those who viewed the mandate as an unfair tax on the uninsured, rather than a necessary tool for market stability.

A comparative analysis of states further illuminates this divide. States that expanded Medicaid under the ACA saw smaller increases in uninsured rates post-2019, as Medicaid served as a safety net for low-income individuals. Non-expansion states, however, experienced more significant spikes in uninsured rates, highlighting the penalty’s role in driving enrollment in the absence of alternative coverage options. For example, Texas, a non-expansion state, saw its uninsured rate rise from 17.3% in 2018 to 18.4% in 2019, while California, which expanded Medicaid, maintained a relatively stable uninsured rate of around 7%. This data suggests that the penalty’s removal had a more pronounced impact in states with fewer coverage alternatives.

In practical terms, the debate over the penalty’s removal underscores the tension between individual choice and collective responsibility in healthcare policy. Critics emphasize the societal cost of higher uninsured rates, including increased uncompensated care and strain on safety-net providers. Supporters, meanwhile, advocate for policies that prioritize affordability and flexibility, such as expanding health savings accounts or promoting short-term health plans. For individuals navigating this landscape, the takeaway is clear: understand your state’s policies, explore all coverage options, and weigh the risks of going uninsured against the financial burden of premiums. The penalty’s removal shifted the calculus, but the decision to enroll in health insurance remains a critical one, with implications for both personal finances and public health.

Sleep Study: Is Medical Insurance Coverage Available?

You may want to see also

Frequently asked questions

Yes, President Trump signed the Tax Cuts and Jobs Act in 2017, which reduced the individual mandate penalty of the Affordable Care Act (ACA) to $0, effective January 1, 2019.

At the federal level, the penalty for not having health insurance was eliminated starting in 2019. However, some states have implemented their own mandates and penalties for uninsured residents.

The elimination of the penalty does not repeal the ACA but removes a key enforcement mechanism for the individual mandate. The ACA remains in effect, including its provisions like pre-existing condition protections and marketplace subsidies.

Yes, several states, including California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia, have enacted their own health insurance mandates and penalties for residents who do not have coverage.