The question of whether Ted Cruz voted to deny health insurance has been a contentious issue in political discourse, particularly in the context of his stance on healthcare legislation. As a Republican Senator from Texas, Cruz has consistently opposed the Affordable Care Act (ACA), also known as Obamacare, and has voted in favor of various proposals aimed at repealing or replacing it. Critics argue that these votes effectively sought to reduce access to health insurance for millions of Americans, particularly those with pre-existing conditions, by dismantling key provisions of the ACA. Cruz, however, has defended his actions by advocating for a more market-based approach to healthcare, claiming that such measures would lower costs and increase choice. This debate highlights the deep ideological divide over the role of government in ensuring healthcare access and the implications of policy decisions on vulnerable populations.

| Characteristics | Values |

|---|---|

| Senator Involved | Ted Cruz (R-TX) |

| Vote Context | Votes related to healthcare and insurance policies |

| Key Votes | - Voted against the Affordable Care Act (ACA) repeal and replace efforts |

| Specific Bills | - American Health Care Act (2017) |

| Outcome of Votes | Supported measures that could reduce access to health insurance for some |

| Position on Medicaid Expansion | Opposed Medicaid expansion under the ACA |

| Stance on Pre-existing Conditions | Supported measures that could weaken protections for pre-existing conditions |

| Recent Activity (as of 2023) | Continued opposition to ACA and government-funded healthcare expansion |

| Public Statements | Advocates for free-market healthcare solutions over government mandates |

| Impact on Constituents | Potentially reduced access to health insurance for low-income Texans |

| Party Alignment | Consistent with Republican Party stance on healthcare policy |

Explore related products

What You'll Learn

![]()

Cruz's Vote on ACA Repeal

Ted Cruz's vote on the Affordable Care Act (ACA) repeal in 2017 was a pivotal moment that underscored his long-standing opposition to the legislation. As a Republican senator from Texas, Cruz consistently argued that the ACA, often called Obamacare, was a government overreach that stifled free-market solutions in healthcare. When the opportunity arose to vote on a partial repeal of the ACA, Cruz supported measures like the "skinny repeal" bill, which aimed to dismantle key provisions such as the individual mandate. This vote reflected his ideological commitment to reducing federal involvement in healthcare, even if it meant potentially leaving millions without insurance coverage.

Analyzing Cruz's vote reveals a strategic calculus beyond mere partisanship. By supporting repeal efforts, he aligned himself with the conservative base, which viewed the ACA as a symbol of government overreach. However, the practical implications of his vote were significant. The Congressional Budget Office estimated that the "skinny repeal" could have resulted in 16 million more uninsured Americans by 2026. Critics argued that Cruz prioritized political ideology over the tangible impact on constituents, particularly those with pre-existing conditions who relied on ACA protections. This tension between principle and practicality highlights the complexities of Cruz's stance.

To understand Cruz's position, consider the broader context of his healthcare philosophy. He has long advocated for state-based solutions and market-driven reforms, such as allowing insurance to be sold across state lines. In his view, these measures would increase competition and lower costs without federal mandates. However, opponents counter that such proposals lack the safeguards provided by the ACA, leaving vulnerable populations at risk. For instance, without the ACA's prohibition on denying coverage for pre-existing conditions, individuals with chronic illnesses could face insurmountable barriers to obtaining insurance.

A comparative analysis of Cruz's vote with those of his colleagues reveals a stark divide within the Republican Party. While some Republicans, like Senator John McCain, famously opposed repeal efforts due to concerns about their impact on coverage, Cruz remained steadfast in his support for dismantling the ACA. This contrast underscores the ideological spectrum within the party and the differing priorities among its members. For voters, Cruz's vote serves as a clear indicator of his policy priorities: a smaller federal role in healthcare, even at the potential expense of widespread coverage.

In practical terms, Cruz's vote on the ACA repeal has implications for anyone navigating the healthcare system. If you're a Texan or a resident of a state with similar political leanings, understanding his stance can help you anticipate future policy shifts. For example, if Cruz's vision of state-based healthcare were realized, you might need to explore private insurance options more aggressively or advocate for state-level protections. Additionally, staying informed about legislative developments and participating in public debates can help mitigate the potential negative impacts of such policy changes. Cruz's vote is not just a historical footnote—it’s a roadmap to his ongoing approach to healthcare policy.

Why Assurant Lost Home Insurance Partnership with GEICO: Key Factors

You may want to see also

Explore related products

![]()

Impact on Pre-existing Conditions

Ted Cruz's voting record on healthcare legislation has significant implications for individuals with pre-existing conditions, a demographic that constitutes roughly 54% of non-elderly Americans. His support for the 2017 American Health Care Act (AHCA) is particularly noteworthy, as this bill would have allowed states to waive essential health benefits and community rating protections. In practice, this could have enabled insurers to charge higher premiums for those with pre-existing conditions, such as asthma, diabetes, or cancer, effectively pricing many out of the market. For instance, a 40-year-old with a pre-existing condition like hypertension might have faced an additional $4,270 in annual premiums under the AHCA, according to a 2017 analysis by the Center for American Progress.

Consider the case of a 55-year-old with a history of heart disease, a condition that affects approximately 121.5 million adults in the U.S. Under the Affordable Care Act (ACA), this individual is guaranteed coverage without being charged more due to their health status. However, the AHCA, which Cruz supported, would have permitted states to opt out of these protections, potentially leaving this person with limited options: either pay exorbitant premiums or go without insurance altogether. This scenario underscores the tangible impact of Cruz's vote on vulnerable populations, where access to affordable care can be a matter of life and death.

To mitigate risks if such policies were enacted, individuals with pre-existing conditions should take proactive steps. First, stay informed about legislative changes at both federal and state levels, as waivers could vary by jurisdiction. Second, explore alternative coverage options, such as employer-sponsored plans or state-run high-risk pools, though these often come with higher costs or limited benefits. Third, maintain detailed medical records and consult with healthcare providers to anticipate potential gaps in coverage. For example, a person with Type 2 diabetes should ensure their medication regimen, which averages $2,500 annually, remains affordable under any new insurance framework.

Cruz's stance also highlights a broader policy debate: the trade-off between lowering premiums for healthy individuals and protecting those with pre-existing conditions. While the AHCA aimed to reduce costs by allowing insurers to offer skimpier plans, this came at the expense of comprehensive coverage for sicker populations. Critics argue that such an approach undermines the principle of shared risk, a cornerstone of insurance markets. Proponents, however, contend that increased flexibility would foster competition and innovation. Yet, empirical evidence from states like Iowa, which implemented similar waivers, shows that premiums for healthy individuals decreased by only 5-10%, while those with pre-existing conditions faced increases of up to 40%.

Ultimately, Cruz's vote to support the AHCA reflects a prioritization of market-based solutions over robust consumer protections. For individuals with pre-existing conditions, this translates to heightened uncertainty and financial vulnerability. Policymakers must balance fiscal considerations with the moral imperative to ensure equitable access to care. Until then, affected individuals should remain vigilant, advocate for their needs, and explore all available resources to safeguard their health and financial stability.

Navigating Gaps in Medical Insurance Coverage: Your Essential Guide

You may want to see also

Explore related products

![[Ted Cruz]-[One Vote Away]-[Hardcover]](https://m.media-amazon.com/images/I/31N0+nnfJ7L._AC_UL320_.jpg)

![]()

Texas Medicaid Expansion Stance

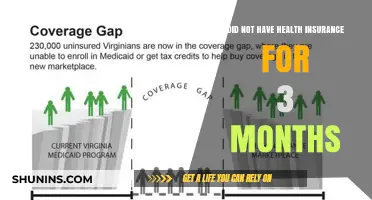

Texas stands as one of 10 states that have not expanded Medicaid under the Affordable Care Act (ACA), leaving a coverage gap for approximately 1.5 million low-income adults. Senator Ted Cruz has consistently opposed Medicaid expansion, aligning with his broader critique of the ACA. His votes and public statements reflect a belief that expansion would burden state budgets and perpetuate a flawed healthcare system. This stance has significant implications for uninsured Texans, particularly those earning too much to qualify for traditional Medicaid but too little to afford private insurance.

Consider the practical impact: without expansion, a single adult in Texas earning up to 138% of the federal poverty level ($19,392 annually in 2023) remains ineligible for Medicaid. This group often faces catastrophic healthcare costs or forgoes care altogether. Cruz argues that market-based solutions, such as health savings accounts and deregulation, would better address affordability. However, critics counter that these alternatives fail to provide immediate relief for those in the coverage gap, who are disproportionately people of color and rural residents.

A comparative analysis highlights the contrast with expansion states. In neighboring New Mexico, which expanded Medicaid, uninsured rates dropped from 20% to 10% between 2013 and 2021. Hospitals in expansion states also saw a 40% reduction in uncompensated care costs, freeing resources for improved services. Texas, meanwhile, spends billions annually on uncompensated care, costs that are often shifted to insured patients through higher premiums. Cruz’s opposition to expansion thus perpetuates a system where taxpayers indirectly subsidize care without addressing root access issues.

For advocates of expansion, the solution is clear: close the coverage gap by accepting federal funds, which cover 90% of expansion costs under the ACA. This would not only insure more Texans but also create an estimated 285,000 jobs and stimulate $130 billion in economic activity over a decade. Cruz’s counterargument—that federal funds are unsustainable—ignores the fact that Texas already forgoes $100 billion in federal funding by rejecting expansion, effectively exporting taxpayer dollars to other states.

Ultimately, Cruz’s vote against Medicaid expansion reflects a philosophical commitment to limited government over pragmatic healthcare solutions. While he frames his stance as fiscally responsible, the human and economic costs in Texas tell a different story. For those in the coverage gap, the debate isn’t abstract—it’s a daily struggle to access care. Until Texas reconsiders its position, Cruz’s votes will remain a defining factor in denying health insurance to millions.

Higher Pay vs. Health Insurance: What Will Companies Offer?

You may want to see also

Explore related products

![]()

Cruz's Alternative Healthcare Plan

Ted Cruz has been a vocal critic of the Affordable Care Act (ACA), often voting against measures that expand government-funded healthcare. However, his alternative healthcare plan, which he has championed in various legislative proposals, focuses on market-based solutions rather than outright denial of coverage. Cruz’s approach emphasizes deregulation, expanded health savings accounts (HSAs), and the sale of insurance across state lines to increase competition and lower costs. While critics argue this could leave vulnerable populations uninsured, Cruz frames it as a way to empower consumers and reduce federal intervention.

One key component of Cruz’s plan is the expansion of HSAs, which allow individuals to save pre-tax dollars for medical expenses. For example, under his proposal, HSA contribution limits would increase to $12,000 for individuals and $24,000 for families annually, with no income restrictions. This is significantly higher than the current limits of $4,150 for individuals and $8,300 for families in 2023. Cruz argues that this would incentivize personal responsibility and provide a safety net for unexpected medical costs. However, critics note that such plans favor higher-income earners who can afford to maximize contributions, potentially widening healthcare disparities.

Another pillar of Cruz’s plan is allowing insurers to sell policies across state lines. He claims this would increase competition and drive down premiums by eliminating state-specific regulations that often mandate coverage for specific services. For instance, a Texan could purchase a plan from a Wyoming insurer with fewer mandated benefits, potentially saving money. Yet, this approach raises concerns about consumer protections, as out-of-state insurers might not comply with local regulations, such as coverage for pre-existing conditions or maternity care.

Cruz also advocates for association health plans (AHPs), which allow small businesses and self-employed individuals to band together to purchase insurance at lower group rates. These plans would be exempt from many ACA regulations, such as essential health benefits requirements. While this could reduce costs for some, it could also lead to skimpier coverage and higher out-of-pocket expenses for enrollees. For example, an AHP might exclude mental health services or prescription drug coverage, leaving individuals vulnerable to high costs in those areas.

Practical implementation of Cruz’s plan would require careful consideration of its trade-offs. For those under 30 or in good health, the flexibility of HSAs and stripped-down policies might be appealing. However, older adults or those with chronic conditions could face higher premiums or limited coverage options. To mitigate risks, individuals should compare policies closely, focusing on deductibles, copays, and excluded services. Additionally, pairing high-deductible plans with robust HSA contributions could provide a buffer against unexpected medical expenses.

In summary, Cruz’s alternative healthcare plan prioritizes market-driven solutions over government-mandated coverage. While it offers potential cost savings and flexibility for some, it also carries risks for vulnerable populations. Understanding its specifics—such as HSA limits, cross-state insurance sales, and AHPs—is crucial for evaluating its feasibility and impact on individual healthcare access.

Why Insurance Companies Swab Your Mouth: Uncovering the Science Behind It

You may want to see also

Explore related products

![]()

Public Reaction to His Vote

Ted Cruz's vote on health insurance, particularly his stance against the Affordable Care Act (ACA), sparked a polarized public reaction that underscored deep ideological divides. Supporters of Cruz’s vote hailed it as a defense of free-market principles, arguing that government intervention in healthcare stifles competition and inflates costs. They viewed his actions as a necessary step to dismantle what they perceived as an overreaching federal program. Conversely, critics lambasted the vote as a callous disregard for the millions of Americans who rely on the ACA for affordable coverage, particularly those with pre-existing conditions. This dichotomy in public sentiment reflects broader disagreements about the role of government in healthcare, with Cruz’s vote serving as a lightning rod for these debates.

The immediate aftermath of Cruz’s vote saw a surge in grassroots activism, particularly among healthcare advocates and progressive groups. Social media platforms became battlegrounds for public outrage, with hashtags like #HealthcareNotWealthCare trending as users shared personal stories of how the ACA had saved lives and livelihoods. Protests erupted in Cruz’s home state of Texas and beyond, with constituents demanding town hall meetings to confront their senator directly. These actions were not merely symbolic; they pressured Democratic lawmakers to capitalize on the momentum and push for further healthcare reforms, while also galvanizing Republican defenders to double down on their opposition to government-led healthcare initiatives.

Analyzing the demographic breakdown of public reaction reveals nuanced insights. Younger voters, who disproportionately benefit from ACA provisions like staying on parental insurance until age 26, were among the most vocal critics of Cruz’s vote. Conversely, older, more conservative voters often supported his stance, echoing concerns about rising premiums and government overreach. This generational divide highlights the differing priorities and experiences shaping public opinion on healthcare policy. For instance, a 2017 Kaiser Family Foundation poll found that 58% of adults under 30 viewed the ACA favorably, compared to just 39% of adults over 65, illustrating how age-specific impacts of the law influenced reactions to Cruz’s vote.

Practical tips for engaging in this debate include focusing on specific policy impacts rather than partisan rhetoric. For example, discussing how eliminating the ACA’s pre-existing conditions protections could affect a 45-year-old cancer survivor’s ability to obtain insurance is more compelling than abstract arguments about socialism. Advocates on both sides can also leverage data, such as the Congressional Budget Office’s projections that repealing the ACA would leave 22 million more Americans uninsured by 2026, to ground their arguments in tangible consequences. By centering discussions on real-world outcomes, individuals can navigate this contentious issue with greater clarity and empathy.

Ultimately, the public reaction to Ted Cruz’s vote on health insurance serves as a case study in how policy decisions resonate beyond Capitol Hill. It underscores the power of personal narratives in shaping public opinion and the importance of understanding the diverse needs of constituents. While Cruz’s vote may have aligned with his conservative base, it also mobilized a broad coalition of opponents, demonstrating the high stakes of healthcare policy in American politics. Moving forward, both lawmakers and citizens must grapple with the complexities of this issue, balancing ideological principles with the practical realities of ensuring access to care for all.

Commonwealth Insurance: Uncovering the Worst Customer Experiences and Complaints

You may want to see also

Frequently asked questions

Ted Cruz has voted in favor of legislation that would repeal or replace the Affordable Care Act (ACA), which could have reduced access to health insurance for some individuals. However, he has not voted explicitly to "deny" health insurance but rather to change the healthcare system.

Yes, Ted Cruz has consistently supported efforts to repeal or replace the ACA, often referred to as Obamacare, arguing that it increases costs and limits choices for Americans.

Ted Cruz has opposed the expansion of Medicaid under the ACA, citing concerns about federal spending and state autonomy. His votes reflect his stance against broader government involvement in healthcare.

Ted Cruz has supported legislation that critics argue could weaken protections for pre-existing conditions, such as the Graham-Cassidy bill. However, he maintains that his goal is to lower costs and increase competition, not to deny coverage.

Ted Cruz has voted against policies that expand government-funded health insurance programs like Medicaid, which primarily serve low-income families. His votes align with his belief in reducing federal involvement in healthcare.