Banks still issue mortgage insurance, which is a type of insurance that protects the lender in case the borrower defaults on their loan. It is usually required when the borrower makes a down payment of less than 20% of the purchase price of the home. Mortgage insurance can be private mortgage insurance (PMI) or a mortgage insurance premium (MIP), depending on the loan type. While it helps borrowers secure a loan with a smaller down payment, it increases the overall cost of the loan by adding to the monthly payments and/or closing costs.

| Characteristics | Values |

|---|---|

| Who does mortgage insurance protect? | The lender, not the borrower. |

| Who pays for mortgage insurance? | The borrower. |

| When is mortgage insurance required? | When the down payment is less than 20% of the purchase price of the home. |

| What is the purpose of mortgage insurance? | To lower the risk to the lender and allow borrowers to qualify for loans they might not otherwise be able to get. |

| What are the different types of mortgage insurance? | Private mortgage insurance (PMI) and mortgage insurance premiums (MIP). |

| Are there alternatives to mortgage insurance? | Yes, some lenders may offer a “piggyback” second mortgage or a loan with a higher interest rate. |

| Can mortgage insurance be cancelled or dropped? | Yes, once the loan balance reaches a certain level, the borrower can request to cancel or drop the insurance. |

| Are there any costs associated with mortgage insurance? | Yes, mortgage insurance increases the overall cost of the loan and is included in the monthly payments and/or closing costs. |

| Do all loans require mortgage insurance? | No, some loans such as VA loans and USDA loans do not require mortgage insurance but may have other fees. |

Explore related products

What You'll Learn

![]()

Private mortgage insurance (PMI)

PMI rates vary according to the down payment amount and credit score but are generally cheaper than FHA rates for borrowers with good credit. Most private mortgage insurance is paid monthly, with little to no initial payment required at closing. However, PMI can also be paid with a one-time upfront premium at closing, or with both upfront and monthly payments. The upfront premium is shown on the Loan Estimate and Closing Disclosure, and the monthly premium is shown in the Projected Payments section of these documents.

Lenders are required to cancel PMI when the mortgage balance reaches 78% of the home's original value or once the borrower is halfway through their loan term, whichever comes first. To avoid paying PMI, borrowers may consider saving up to make a 20% down payment.

Garmin SAR Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Mortgage insurance premium (MIP)

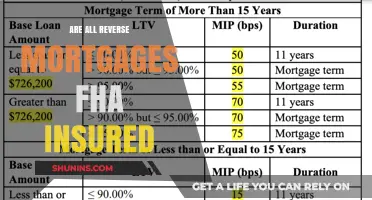

FHA mortgage insurance includes both an upfront cost, paid as part of the closing costs, and a monthly cost included in the borrower's monthly payment. The upfront mortgage insurance premium for FHA loans is 1.75% of the total loan amount and is due at closing. Borrowers can choose to roll this fee into their mortgage if they cannot afford the upfront cost, but this will increase the overall cost of the loan.

For FHA loans originated between December 31, 2000, and June 3, 2013, borrowers who have paid off at least 78% of the loan-to-value amount may request the lender to cancel the MIP. However, for loans originated after June 3, 2013, if the down payment is less than 10% of the home's value, the borrower must pay the MIP for the entire duration of the loan. The only way to remove MIP on an FHA loan is to refinance it into a non-FHA product.

While mortgage insurance premiums were previously tax-deductible for the years 2018, 2019, and 2020, they are no longer deductible as of 2023. Lenders are required to send Form 1098 Mortgage Interest Statement to borrowers and the Internal Revenue Service (IRS), which includes the total MIP or PMI premiums in box 5.

Track Day Insurance: Is the Cost Justified?

You may want to see also

Explore related products

![]()

Federal Housing Administration (FHA) loans

FHA loans are typically more expensive than conventional loans because they require the borrower to pay for mortgage insurance, which protects the lender in the event of borrower default. Mortgage insurance is mandatory for FHA loans and is included in the total monthly payment made to the lender. The cost of mortgage insurance is the same for all borrowers, regardless of credit score, with a slight increase for down payments of less than 5%.

FHA loans are available for single-family, multifamily, manufactured home, and hospital properties. They are also available for mobile homes located in mobile home parks or those where the borrower owns the land.

For seniors aged 62 and above who own their homes or have a low loan balance, the FHA Reverse Mortgage product enables them to convert a portion of their equity into cash.

FHA loans have been helping people become homeowners since 1934. Borrowers can find an FHA-approved lender or contact a HUD-approved housing counsellor for more information.

Understanding Tax Implications: Reporting Insurance 1099

You may want to see also

Explore related products

![]()

Lender-paid mortgage insurance

With LPMI, the lender covers the cost of mortgage insurance and recoups the cost by charging a higher interest rate on the loan. This higher interest rate is usually lower than the monthly payments for private mortgage insurance (PMI), but it may cost more over the life of the loan. LPMI cannot be cancelled and remains in effect until the loan is paid off or refinanced.

Borrowers with excellent credit may pay a quarter-point more in interest with LPMI. However, this cost is still significantly lower than the cost of PMI. For example, for a $400,000 loan, the borrower would pay an extra $66 per month with LPMI, compared to an extra $365 per month for PMI.

LPMI is a good option for borrowers who want to keep their monthly payments affordable and are willing to accept a higher interest rate over the life of the loan. It is important to compare several lenders to find the most suitable option.

Alfa Insurance Joins the Farmers Insurance Family: Expanding the Horizons of Coverage

You may want to see also

Explore related products

![]()

Split-premium mortgage insurance

Mortgage insurance is designed to protect lenders in the event that the borrower defaults on their loan. Typically, borrowers who make a down payment of less than 20% of the purchase price of the home are required to pay for mortgage insurance. While it lowers the risk for lenders, it increases the cost of the loan for borrowers.

The upfront payment for split-premium mortgage insurance is paid to the mortgage insurance company at closing, with the remaining amount paid in monthly instalments from the borrower's escrow account. This option offers flexibility to borrowers, reducing the cash needed at closing and securing lower monthly payments. For example, a homebuyer purchasing a home for $250,000 may pay 1.0% upfront ($2,500) to the mortgage insurance company. As a result, their monthly mortgage insurance drops to $83 per month, from $123. In this case, it would take five years to make back the upfront payment.

It is important to note that the single premium is non-refundable. If rates drop and the borrower refinances in a few years, they may lose the upfront payment or have a higher loan amount. Therefore, it is crucial to consider the potential risks and weigh them against the benefits of lower monthly payments.

Is USPS Insurance Worth the Cost?

You may want to see also

Frequently asked questions

Mortgage insurance protects the lender in case the borrower defaults on the loan. It lowers the risk to the lender of issuing a loan, so borrowers may qualify for a loan that they might not otherwise be able to get.

Yes, banks still issue mortgage insurance. However, it is not always compulsory. If you can afford a 20% down payment on a property, you may not need mortgage insurance.

There are two main types of mortgage insurance: private mortgage insurance (PMI) and mortgage insurance payments (MIP).

Your lender will arrange PMI, and private insurance companies will issue the policy. Mortgage insurance is usually required for Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans.