FHA loans are a type of mortgage that is insured by the government and issued by a bank or lender approved by the Federal Housing Administration (FHA). These loans are designed to help low- to moderate-income families attain homeownership, and they are particularly attractive to first-time homebuyers due to their low minimum down payment requirements and flexibility with credit scores. When it comes to homeowners insurance, FHA loans have specific requirements that must be met. Borrowers are typically required to purchase mortgage insurance, which includes two types of mortgage insurance premiums (MIPs) – one paid upfront and the other paid monthly. Additionally, the property being purchased must have homeowners insurance in effect on the day of closing. This insurance protects against fires, theft, or disasters and covers the dwelling and belongings. The consumer can choose their insurance carrier, and the insurance policy must meet certain FHA requirements.

| Characteristics | Values |

|---|---|

| Insurance requirements | The property being purchased must have homeowners insurance in effect on the day of closing. |

| Insurance policy | The insurance policy must remain in effect as long as there is a mortgage on the property. |

| Insurance payment | The insurance policy will be paid as part of the monthly mortgage payment. |

| Insurance carrier | The consumer can choose their own insurance carrier as long as the policy meets FHA requirements. |

| Switching insurance carriers | The consumer can switch insurance carriers at any time by notifying the mortgage servicer. |

| Cancelling insurance policy | If a consumer cancels an insurance policy without replacing it with a new carrier, the mortgage servicer will find an insurance carrier for the consumer. |

| Mortgage insurance premium (MIP) | FHA loans require the borrower to pay a mortgage insurance premium (MIP). |

| Mortgage insurance costs | The cost of mortgage insurance is recalculated each year based on the average outstanding loan balance. |

| Mortgage insurance premium reduction | On March 20, 2023, the Department of Housing and Urban Development (HUD) reduced FHA annual mortgage insurance premiums (MIP) for new borrowers. |

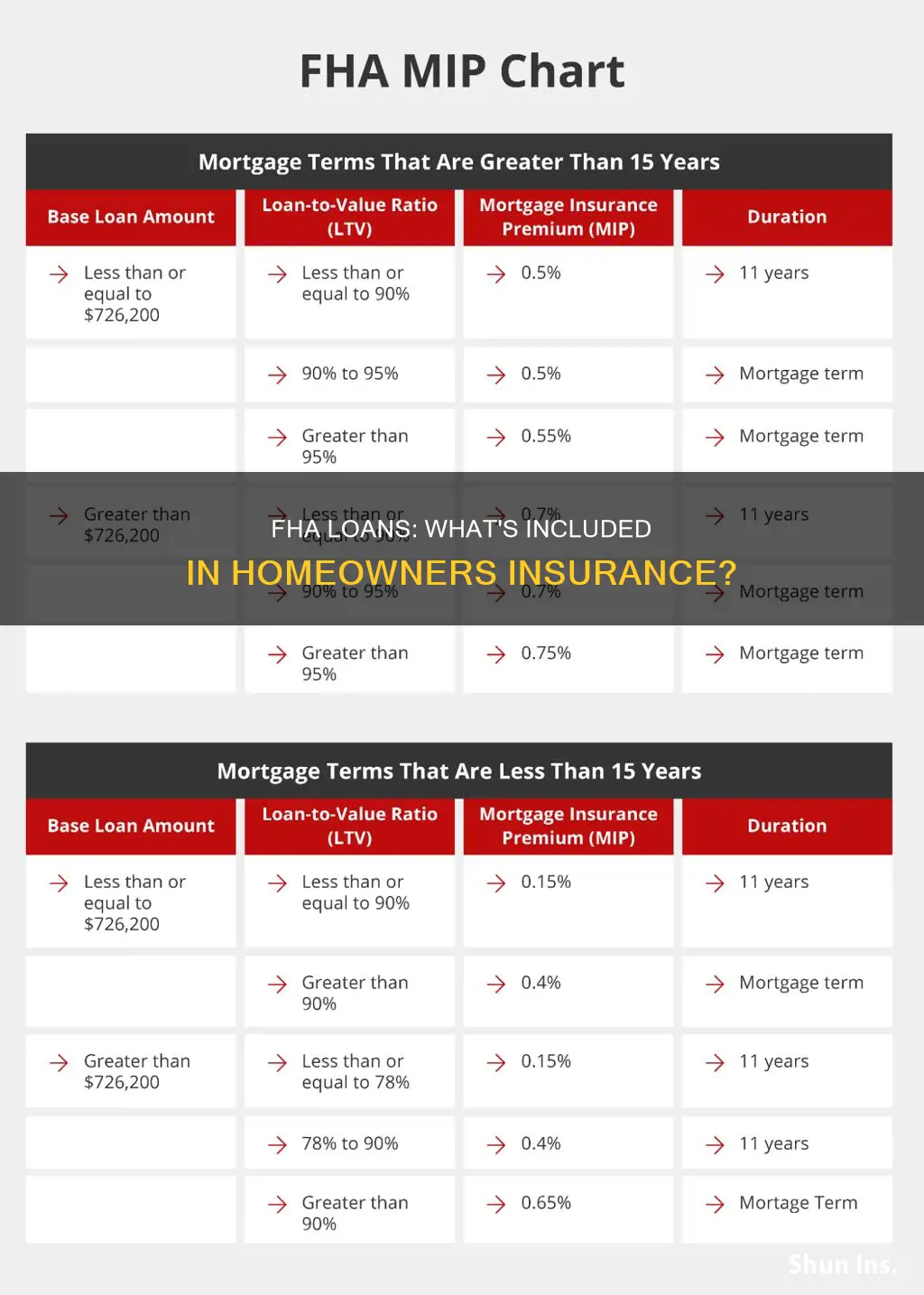

| Mortgage insurance premium upfront cost | The upfront mortgage insurance premium is equal to 1.75% of the base loan amount. |

| Mortgage insurance premium annual cost | The annual cost of mortgage insurance depends on the loan amount, loan-to-value ratio, and mortgage term. |

| Mortgage insurance duration | For recent FHA loans, borrowers will need to pay insurance premiums for at least 11 years and may need to pay them for the life of the loan. |

| Hazard insurance | Hazard insurance is not always a requirement but may be required by the lender. |

| Flood insurance | Flood insurance may be required if the property is located in a Special Flood Hazard Area (SFHA). |

| Earthquake insurance | The cost of a separate earthquake policy will depend on the likelihood of earthquakes in the area. |

| Homeowner's insurance | Homeowner's insurance protects against losses and damage to the residence and can also cover furnishings and other assets in the home. |

Explore related products

What You'll Learn

![]()

FHA loans require homeowners insurance

The homeowner's insurance policy must include specific items, such as a Replacement Cost Estimator (RCE) if the insurance amount is lower than the loan amount. The insured person(s) must match the person(s) on the loan, and the Mortgagee Clause of the lender, including the loan number, must be included in the Mortgagee section. These items must match the loan documents exactly.

In addition to homeowners insurance, certain properties may require additional insurance coverages, such as flood insurance, which will be determined during the loan process. The lender's standards for insurance requirements must be followed as long as they are in accordance with FHA loan guidelines, state law, and federal law.

Borrowers are required to purchase mortgage insurance, specifically a mortgage insurance premium (MIP), which includes an upfront premium and monthly premiums. The cost of mortgage insurance is recalculated each year based on the outstanding loan balance, and borrowers may need to pay premiums for the life of the loan.

Homeowner's insurance provides financial protection against fires, theft, or disasters suffered at the home, covering the dwelling itself and the belongings within it. It is recommended to shop around for the right policy, as prices and services offered can vary.

Orthodontic Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Mortgage insurance premium (MIP)

FHA loans require mortgage insurance in the form of a Mortgage Insurance Premium (MIP). MIP is a type of mortgage insurance required of homeowners who take out loans backed by the Federal Housing Administration (FHA). Unlike conventional loans, which usually only require private mortgage insurance (PMI) if a home down payment is less than 20% of the purchase price, all FHA loans require MIP. This is because FHA loans are aimed at higher-risk borrowers, who are more likely to default on loans, due to the low down payment of 3.5% and a credit score as low as 580.

MIP is paid by the borrower monthly, with the annual premium divided by 12 months, along with the principal payment. The total MIP or PMI premiums will be listed in box 5 of the Form 1098 Mortgage Interest Statement, which your lender is required to send to you and the IRS. This form lists your mortgage payments over the past year and can affect your income tax.

For FHA loans originated between December 31, 2000, and June 3, 2013, if you have paid off at least 78% of the loan-to-value amount, you may ask the lender to cancel the MIP. For loans originated after June 3, 2013, if you made a down payment of less than 10% of the home's value, you must pay the MIP for the life of the loan. The only way to remove the MIP on an FHA loan is to refinance it into a non-FHA product.

Upfront MIP is required for most FHA single-family mortgage insurance programs. Lenders must pay this within 10 calendar days of the mortgage closing or disbursement date, whichever is later.

Calculating Mortgage Indemnity Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Hazard insurance

FHA loans require that the property being purchased has homeowners insurance in effect on the day of closing. This insurance policy must remain in effect as long as there is a mortgage on the property. The consumer can choose their insurance carrier, as long as the policy meets FHA requirements. The consumer can also switch insurance carriers at any time, as long as they notify the mortgage servicer of any changes.

Now, the term "hazard insurance" is often used by mortgage lenders to describe dwelling coverage under a homeowners insurance policy. It is not a standalone policy but a component of the broader homeowners insurance policy. This type of insurance covers the physical structure of your home and protects it against damage caused by perils like natural disasters and vandalism. It also covers personal property, liability, and additional living expenses in case of a covered loss. For example, if a fire or wind damages your personal items, hazard insurance can help repair or replace them.

To summarise, while homeowners insurance is a requirement for FHA loans, hazard insurance is not always mandatory. However, it is often included as a component of homeowners insurance and may be required by the lender depending on the specific circumstances and location of the property.

Reporting Insurance Proceeds: 1120-S Compliance

You may want to see also

Explore related products

![]()

Flood insurance

FHA loans require that the property being purchased has homeowners insurance in effect on the day of closing. In addition to homeowners insurance, certain properties may require additional insurance coverages, such as flood insurance, which will be determined during the loan process.

The National Flood Insurance Reform Act of 1994 requires the owner of a property located in a community participating in the NFIP and mapped in a Special Flood Hazard Area (SFHA) to purchase flood insurance as a condition of receiving a mortgage backed by the Federal National Mortgage Association (Fannie Mae) or the Federal Home Loan Mortgage Corporation (Freddie Mac), or FHA.

As of December 21, 2022, the US Department of Housing and Urban Development (HUD), through the Federal Housing Administration (FHA), allows homeowners with FHA-insured mortgage financing to obtain flood insurance policies that conform to FHA requirements from private insurance providers. This update to the HUD's rule has significantly expanded the flood insurance choices for FHA borrowers. FHA loan holders can now choose either flood insurance through the National Flood Insurance Program or the private flood insurance market.

The mortgagee may determine that a private flood insurance policy meets the definition of private flood insurance without further review of the policy if the following statement is included within the policy or as an endorsement to the policy: "This policy meets the definition of private flood insurance contained in 24 CFR 203.16a(e) for FHA-insured mortgages."

It is important to note that flood insurance can be costly, and the cost depends on several factors such as the type of structure on the property, its age, and whether it is occupied. One way to determine the flood risk for a potential property is to look at the appropriate flood map at FEMA's online Flood Map Service Center.

How Much Is Your Insurance Agency Worth?

You may want to see also

Explore related products

![]()

Choosing a homeowners insurance policy

FHA loans require that the property being purchased has homeowners insurance in effect on the day of closing. The insurance policies required need to remain in effect as long as there is a mortgage on the property. The consumer can choose their insurance carrier, as long as the policy meets FHA requirements.

- Shop around for the best policy: Compare quotes from several companies, considering deductibles, coverage limits, and benefits. Asking neighbours about their policies can be a good starting point, but their policy might not be the cheapest for you.

- Consider the coverage options: Determine the amount of personal liability, medical payments, and umbrella insurance you may need. For example, if you often host guests, you may want a higher liability limit. If you have expensive personal belongings, you may want to add valuable items coverage.

- Check for discounts: Many companies offer discounts for things like installing a home security alarm, having a fire sprinkler system, or bundling your home policy with auto or life insurance.

- Know the exclusions: Home insurance policies often exclude liability coverage for injuries caused by certain dog breeds, such as pit bulls, German shepherds, or Rottweilers. If this applies to you, seek out a home insurer that offers coverage.

- Understand the requirements: FHA loans require a mortgage insurance premium (MIP) to be paid. Additionally, certain properties may require additional insurance coverages, such as flood insurance, which will be determined during the loan process.

Protect Your Remodel: Insurance for Homeowners

You may want to see also

Frequently asked questions

Yes, FHA loans require homeowners insurance. The insurance policy must be in effect on the day of closing and remain in effect for as long as there is a mortgage on the property.

Homeowners insurance protects you financially against fires, theft, or disasters suffered at your home. It covers the dwelling itself and your belongings.

In addition to homeowners insurance, certain properties may require additional insurance coverages, such as flood insurance or earthquake insurance. This will depend on the lender's standards and the location of the property.