Health insurance coverage for STD testing is a critical aspect of sexual health and preventive care, but the extent of coverage can vary widely depending on the insurance plan, provider, and location. Many health insurance plans, particularly those compliant with the Affordable Care Act (ACA) in the United States, cover STD testing as part of preventive services without requiring a copay or deductible. However, coverage specifics may differ based on factors such as the type of test, frequency of testing, and whether the service is provided in-network. Additionally, some plans may require pre-authorization or limit coverage to certain age groups or high-risk individuals. Understanding your policy’s details and consulting with your insurance provider or healthcare professional is essential to ensure you receive the necessary testing without unexpected costs.

Explore related products

What You'll Learn

![]()

STD Testing Coverage Basics

Health insurance plans often cover STD testing, but the extent of coverage varies widely based on factors like plan type, location, and preventive care mandates. Under the Affordable Care Act (ACA), most private insurance plans must cover FDA-approved preventive services, including STD screenings, without out-of-pocket costs if performed by an in-network provider. However, not all STDs are explicitly listed as covered preventive tests, and frequency of testing may depend on age, gender, and risk factors. For example, annual chlamydia and gonorrhea screenings are recommended for sexually active women under 25, while syphilis and HIV testing may be covered for high-risk individuals. Always verify with your insurer to confirm which tests are included and under what conditions.

Navigating coverage requires understanding the difference between preventive and diagnostic testing. Preventive tests, such as routine screenings for asymptomatic individuals, are typically fully covered under ACA-compliant plans. Diagnostic tests, ordered when symptoms are present or after a positive screening, may be subject to deductibles or copays. For instance, if a routine chlamydia test comes back positive, follow-up tests to confirm the diagnosis or monitor treatment might incur costs. To minimize expenses, ask your provider to code the test as preventive if it aligns with recommended guidelines, such as the CDC’s STI Treatment Guidelines.

Medicaid and Medicare also cover STD testing, though specifics differ by state and plan. Medicaid programs generally follow ACA preventive care guidelines, offering no-cost screenings for eligible STDs. Medicare Part B covers HIV screenings once every 12 months for beneficiaries at increased risk and may cover other STD tests if deemed medically necessary. For those without insurance, community health clinics often provide low-cost or free testing, though availability varies by location. Planned Parenthood, for example, offers income-based sliding scale fees for STD services, including testing and treatment.

Employer-sponsored plans may include additional restrictions or exclusions, particularly in grandfathered plans not required to comply with ACA mandates. Some plans might limit coverage to specific STDs or require pre-authorization for certain tests. Group plans often provide summary plan descriptions (SPDs) detailing covered services, so review this document or contact your HR department for clarity. If your plan denies coverage for a recommended test, appeal the decision by citing CDC or USPSTF guidelines, which insurers often reference when determining preventive care coverage.

Practical tips can help maximize coverage and reduce costs. Schedule tests during your annual wellness visit to ensure they’re billed as preventive care. Use in-network labs or clinics to avoid surprise bills, and confirm coverage for at-home testing kits, which some insurers now include. Keep a record of test dates and results to track compliance with recommended screening intervals. For uninsured individuals, consider purchasing short-term health insurance plans, which may cover STD testing, or explore state-specific programs that subsidize STI services. Proactive communication with providers and insurers is key to navigating the complexities of STD testing coverage.

How to File a Complaint Against Your Insurance Company: A Guide

You may want to see also

Explore related products

![]()

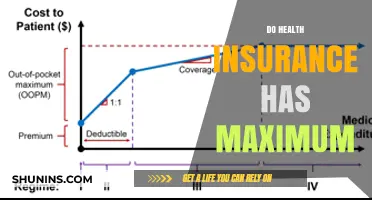

In-Network vs. Out-of-Network Costs

Health insurance coverage for STD testing varies widely, but one critical factor that determines your out-of-pocket costs is whether you use in-network or out-of-network providers. In-network providers have negotiated rates with your insurance company, often resulting in lower costs for you. For example, a routine STD panel at an in-network clinic might cost you a $20 copay, while the same test at an out-of-network facility could leave you responsible for 50% of the total bill, which can easily exceed $200. Understanding this difference is essential for managing healthcare expenses effectively.

To illustrate, consider a 25-year-old individual with a PPO plan seeking chlamydia and gonorrhea testing. If they visit an in-network urgent care center, the test is typically covered as preventive care under the Affordable Care Act, meaning no copay is required. However, if they choose an out-of-network lab, the insurance might reimburse only 60% of the cost, leaving the patient with a bill of $150 or more. This disparity highlights the importance of verifying a provider’s network status before scheduling an appointment.

From a practical standpoint, here’s a step-by-step approach to minimize costs: First, contact your insurance provider to confirm coverage for STD testing and request a list of in-network facilities. Second, use your insurer’s online portal or app to locate nearby in-network clinics or labs. Third, if you must use an out-of-network provider, ask for a detailed cost estimate upfront and inquire about potential reimbursement rates. Finally, keep records of all communications and bills for future reference or disputes.

A cautionary note: Some insurance plans require pre-authorization for out-of-network services, and failing to obtain this can result in denied claims. Additionally, out-of-network providers may bill for amounts exceeding the insurer’s approved rate, a practice known as balance billing. While some states have laws to protect patients from this, it’s still a risk to be aware of. Always clarify these details with your insurer to avoid unexpected financial burdens.

In conclusion, the choice between in-network and out-of-network providers can significantly impact the cost of STD testing. By prioritizing in-network options and understanding your plan’s specifics, you can ensure access to affordable care without compromising your financial stability. Remember, preventive care is a cornerstone of health management, and navigating insurance complexities is a crucial part of that process.

Affordable Medical Insurance for Two: Monthly Costs Explored

You may want to see also

Explore related products

![Bartovation Super Taster Test Genetics Lab Kit with Instructions, Phenylthiourea (PTC), Sodium Benzoate [Each Vial Includes 100 Paper Strips]](https://m.media-amazon.com/images/I/81QKSPsClsL._AC_UL320_.jpg)

![]()

Preventive Care vs. Diagnostic Testing

Health insurance coverage for STD testing hinges on whether the test is classified as preventive care or diagnostic testing. Preventive care, such as annual screenings for chlamydia and gonorrhea in sexually active individuals under 25, is typically covered without cost-sharing under the Affordable Care Act (ACA). These tests are recommended by organizations like the CDC to identify asymptomatic infections early, preventing complications like infertility or pelvic inflammatory disease. Diagnostic testing, however, is triggered by specific symptoms or exposure risks and may incur copays or deductibles, depending on the plan’s structure.

Consider a 22-year-old college student who requests an STD panel during a routine checkup. If the test is billed as preventive—aligned with CDC guidelines for their age group—insurance must cover it fully. But if the same individual seeks testing after experiencing genital discharge or a partner’s positive diagnosis, the test shifts to diagnostic. In this case, the insurer may require a copay or apply it to the deductible, even if the result is negative. This distinction underscores the importance of understanding how tests are coded and billed to avoid unexpected costs.

From a policy perspective, the preventive vs. diagnostic divide reflects a broader tension in healthcare: prioritizing population health versus individual treatment. Preventive STD testing aligns with public health goals by curbing transmission rates, while diagnostic testing addresses immediate clinical concerns. Insurers often incentivize preventive care through zero-cost coverage, recognizing its long-term cost savings. For example, untreated chlamydia can lead to $1.5 billion annually in healthcare expenses due to complications, whereas early detection costs roughly $20 per test. Advocates argue that expanding preventive coverage could reduce this disparity, but diagnostic testing remains essential for symptomatic patients who cannot wait for routine screenings.

Practical tips for navigating this system include verifying how your provider bills the test beforehand. Ask whether the visit and lab work will be coded as preventive or diagnostic—some clinics default to diagnostic billing unless explicitly instructed otherwise. Additionally, leverage telehealth platforms that offer flat-fee STD testing kits, bypassing insurance complexities altogether. For those with high-deductible plans, inquire about cash prices, which can be as low as $50 for a comprehensive panel compared to $200+ through insurance when billed diagnostically. Understanding these nuances empowers individuals to access care without financial surprises.

Ultimately, the preventive-diagnostic dichotomy highlights a system designed to balance collective and individual needs. While preventive care offers a cost-effective pathway to STD management, diagnostic testing remains critical for timely treatment. Patients must advocate for accurate billing, while policymakers could bridge gaps by expanding preventive coverage criteria. Until then, staying informed about guidelines, costs, and alternatives ensures that financial barriers do not deter essential testing.

Medical Insurance and Pharmacy: What's Covered?

You may want to see also

Explore related products

![[Single Test] ETG Test Strip - 80 Hour Detection Time, Rapid Detection with high Sensitivity, Instant Read, Results Within 5 Minutes](https://m.media-amazon.com/images/I/41iPfMgGZrL._AC_UL320_.jpg)

![]()

Insurance Plan Exclusions for STDs

Health insurance plans often exclude certain sexually transmitted disease (STD) tests or treatments, leaving policyholders with unexpected out-of-pocket costs. For instance, while most plans cover basic STD screenings like chlamydia and gonorrhea, they may exclude tests for less common infections such as syphilis or herpes unless symptoms are present. This exclusion stems from insurers categorizing these tests as "preventive" or "diagnostic," with the latter often requiring higher cost-sharing. To avoid surprises, review your plan’s Summary of Benefits and Coverage (SBC) for specific exclusions and consult your provider about potential costs before testing.

Analyzing the rationale behind these exclusions reveals a cost-management strategy by insurers. Less common STD tests, though critical for public health, are deemed low-priority for blanket coverage due to their perceived rarity. For example, herpes testing, which involves IgG and IgM antibody tests, is frequently excluded unless a patient exhibits symptoms like sores or outbreaks. Similarly, HIV RNA early detection tests, which can cost upwards of $150, are often not covered until 90 days post-exposure, despite their value in early diagnosis. Understanding these exclusions helps policyholders advocate for coverage expansions or seek affordable testing alternatives, such as public health clinics.

Persuasively, insurers should reconsider these exclusions given the rising STD rates and the long-term costs of untreated infections. The CDC reports over 2 million annual cases of chlamydia, gonorrhea, and syphilis, yet many individuals delay testing due to cost concerns. Excluding tests like HPV genotyping or trichomoniasis screening undermines preventive care, leading to more severe health outcomes and higher treatment expenses. For instance, untreated gonorrhea can cause pelvic inflammatory disease (PID), increasing infertility risks and healthcare costs. By covering comprehensive STD testing, insurers could reduce long-term expenditures and improve public health outcomes.

Comparatively, Medicaid and Medicare offer more inclusive STD coverage than private plans, particularly for high-risk populations. Medicaid, for example, covers all FDA-approved STD tests for eligible individuals under its preventive services mandate, including screenings for syphilis, hepatitis B and C, and HIV. Medicare Part B covers annual HIV screenings and hepatitis B tests for at-risk individuals, such as those aged 75–79 or with multiple partners. Private insurers could emulate these models by expanding coverage to include all CDC-recommended STD tests, ensuring equitable access to care regardless of income or plan type.

Descriptively, navigating exclusions requires proactive steps. First, identify your risk factors—age, number of partners, and sexual practices—to determine necessary tests. For example, individuals under 25 or with multiple partners should prioritize chlamydia and gonorrhea screenings, typically covered under preventive care. Second, use in-network labs to minimize costs; out-of-network facilities often charge higher rates, even for covered tests. Third, explore community health centers or Planned Parenthood, which offer sliding-scale fees for uninsured or underinsured individuals. Finally, document all communications with your insurer regarding coverage denials, as appeals can sometimes reverse exclusions based on medical necessity.

Who Oversees Health Insurers? Key Regulatory Bodies Explained

You may want to see also

Explore related products

![]()

Confidentiality and Privacy Concerns

Health insurance coverage for STD testing often raises questions about confidentiality and privacy, especially for individuals concerned about sensitive health information. Under the Health Insurance Portability and Accountability Act (HIPAA), healthcare providers and insurers are legally obligated to protect patient data. However, gaps in understanding and implementation can lead to unintended disclosures. For instance, if an STD test is billed to insurance, the procedure code may appear on an Explanation of Benefits (EOB) statement, which could be mailed to a shared address or accessed by policyholders, potentially revealing private health details to family members or employers.

To mitigate these risks, patients have several proactive steps they can take. First, inquire about direct billing options or pay out-of-pocket for the test to avoid insurance documentation altogether. Many clinics offer sliding-scale fees or reduced rates for self-pay patients, making this a viable option for those prioritizing privacy. Second, request that the provider use a generic billing code or note "sensitive services" on the claim to minimize explicit details on insurance records. While not all insurers accommodate this, it’s worth asking. Lastly, consider using a confidential testing service, such as Planned Parenthood or local health departments, which often have stricter privacy protocols and may not require insurance involvement.

Comparing confidentiality risks between insurance-covered and self-pay testing reveals a trade-off between cost and privacy. Insurance coverage reduces financial burden but increases the likelihood of documentation exposure. Self-pay eliminates this risk but may be cost-prohibitive for some. For example, an uninsured individual might pay $50–$200 for an STD panel, while insured patients face minimal copays but potential privacy breaches. This comparison underscores the importance of weighing personal circumstances when deciding how to proceed.

A persuasive argument for policy reform emerges from these concerns. Insurers should adopt more discreet billing practices, such as excluding sensitive procedures from EOBs or providing digital-only statements with opt-out options. Additionally, expanding access to free or low-cost confidential testing services could reduce reliance on insurance altogether. Such measures would not only protect individual privacy but also encourage more people to seek testing without fear of unintended disclosure, ultimately benefiting public health.

In conclusion, while HIPAA provides a baseline for privacy protection, practical challenges persist in ensuring confidentiality for STD testing. Patients must navigate these complexities by understanding their options and advocating for themselves. Meanwhile, systemic changes in billing practices and service accessibility could alleviate these concerns, fostering a more private and supportive healthcare environment.

Understanding Co-Insurance: When It Applies and Why

You may want to see also

Frequently asked questions

Yes, most health insurance plans cover STD testing as part of preventive care services, especially under the Affordable Care Act (ACA) in the U.S. However, coverage may vary depending on your plan and provider.

In many cases, STD testing is fully covered without out-of-pocket costs if it’s considered preventive care. However, if testing is done as part of a diagnostic visit or if your plan doesn’t cover it, you may incur costs like copays or deductibles.

Insurance typically covers STD testing through healthcare providers, but anonymous or confidential testing through specialized clinics may not be covered. Check with your insurance provider or the testing facility for details.