Health insurance renewal is a critical aspect of maintaining continuous coverage and ensuring financial protection against medical expenses. Typically, health insurance policies are renewed annually, and policyholders must decide whether to continue with their current plan or explore other options. The renewal process often involves reviewing the terms, conditions, and premiums of the existing policy, as insurers may update coverage details or adjust costs based on factors like inflation, healthcare trends, or individual claims history. It’s essential for policyholders to assess their health needs, compare available plans, and understand any changes to avoid lapses in coverage. Additionally, some insurers may automatically renew policies unless explicitly canceled, while others require active confirmation from the policyholder. Being proactive during the renewal period can help individuals secure the most suitable and cost-effective health insurance for the upcoming year.

| Characteristics | Values |

|---|---|

| Automatic Renewal | Most health insurance policies renew automatically unless canceled. |

| Renewal Period | Typically annual, but some plans may offer multi-year renewals. |

| Premium Changes | Premiums may increase or decrease based on inflation, claims history, or policy changes. |

| Policy Changes | Insurers may update coverage, exclusions, or terms at renewal. |

| Open Enrollment | Renewal often coincides with open enrollment periods for changes. |

| Guaranteed Renewal | In many regions, renewal is guaranteed unless non-payment or fraud occurs. |

| Notice Requirement | Insurers must notify policyholders of renewal terms and changes in advance. |

| Grace Period | A grace period (e.g., 30 days) is often provided for premium payment after renewal. |

| Portability | Policies may be portable across jobs or regions, depending on regulations. |

| Age-Based Adjustments | Premiums may increase with age or change in health status. |

| Regulatory Compliance | Renewals must comply with local healthcare laws and regulations. |

| Cancellation Rights | Policyholders can cancel during the renewal period without penalty. |

| Renewal Documentation | Insurers provide updated policy documents and terms upon renewal. |

| Pre-Existing Conditions | Coverage for pre-existing conditions continues uninterrupted at renewal. |

| Network Changes | Provider networks may change at renewal, affecting in-network coverage. |

| Policyholder Consent | Some policies require explicit consent for renewal, especially for changes. |

Explore related products

What You'll Learn

![]()

Auto-renewal policies and procedures

Auto-renewal policies in health insurance are designed to streamline the continuation of coverage, ensuring policyholders remain protected without the hassle of manual renewals. Typically, insurers initiate this process 30 to 60 days before the policy expires, sending a renewal notice that outlines updated terms, premiums, and coverage details. Policyholders must review this document carefully, as changes in premiums or benefits can occur annually due to factors like inflation, medical cost trends, or shifts in the policyholder’s health status. For instance, a 45-year-old individual might see a 5-10% premium increase due to age-related risk adjustments, while a family plan could reflect added pediatric dental coverage mandated by regulatory updates.

While auto-renewal simplifies continuity, it’s not without pitfalls. One common issue is the lack of proactive comparison shopping. Since auto-renewal defaults to the existing plan, policyholders may miss out on more cost-effective or comprehensive alternatives in the market. For example, a policyholder might pay $400 monthly for a plan with a $3,000 deductible, unaware that a competitor offers similar coverage for $350 with a $2,500 deductible. To avoid this, experts recommend using the renewal notice as a reminder to evaluate at least three competing plans annually, leveraging tools like Healthcare.gov or private insurance marketplaces.

Another critical aspect of auto-renewal is understanding the opt-out process. Insurers are required by law to provide a clear cancellation procedure, but the timeline varies. Most require a 15- to 30-day notice before the renewal date to avoid automatic enrollment and subsequent billing. Policyholders should document cancellation requests in writing and retain proof of submission, such as email receipts or certified mail tracking numbers. Failure to do so can result in unintended coverage continuation and financial penalties, particularly if the policyholder has already secured alternative insurance.

For those with dynamic health needs, auto-renewal demands extra scrutiny. Pregnant individuals, for instance, should verify that prenatal and postnatal care remain covered under the renewed plan, as some insurers adjust maternity benefits annually. Similarly, policyholders managing chronic conditions like diabetes or hypertension should confirm that prescription drug formularies haven’t changed, as shifts in tier placement can significantly impact out-of-pocket costs. A practical tip is to consult a broker or use online benefit checkers to cross-reference medication coverage across plans.

In conclusion, while auto-renewal policies offer convenience, they require active engagement to maximize value. Policyholders should treat the renewal notice as a call to action: review changes, compare alternatives, and verify alignment with current health needs. By doing so, they can ensure continuity of care without overpaying or sacrificing essential benefits. Remember, auto-renewal is a tool, not a set-it-and-forget-it solution—its effectiveness hinges on informed decision-making.

Understanding Primary Insurance: PPO vs. Medicare

You may want to see also

Explore related products

![]()

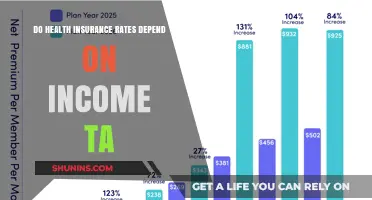

Premium changes and adjustments

Health insurance premiums rarely remain static from one year to the next. Insurers adjust rates based on a complex interplay of factors, leaving policyholders to navigate a landscape of potential increases or, occasionally, decreases. Understanding these adjustments is crucial for anticipating costs and making informed decisions during renewal.

Health insurance premiums are not set in stone. Each year, insurers meticulously evaluate a multitude of factors to determine adjustments, ensuring their plans remain financially viable while reflecting the evolving healthcare landscape. This process, while complex, directly impacts the amount policyholders pay for coverage.

Several key drivers influence premium changes. Firstly, claims experience plays a significant role. If an insurer experiences a surge in claims within a specific demographic or geographic area, premiums for those groups may rise to offset the increased payouts. Conversely, a year with lower-than-expected claims could potentially lead to premium stability or even reductions. Medical inflation, the rising cost of healthcare services, medications, and technology, is another major factor. Insurers must account for these escalating costs when setting premiums to ensure they can cover the expenses associated with policyholders' medical needs. Lastly, regulatory changes can significantly impact premiums. New mandates requiring coverage for specific services or changes in government subsidies can directly affect the cost of insurance plans.

Proactive Steps for Policyholders:

While premium adjustments are largely outside individual control, policyholders can take steps to mitigate their impact. Reviewing plan options annually during the open enrollment period is crucial. Insurers often introduce new plans or modify existing ones, potentially offering more cost-effective alternatives. Comparing premiums and benefits across different plans allows individuals to identify the best value for their needs. Additionally, considering high-deductible health plans (HDHPs) paired with Health Savings Accounts (HSAs) can be a strategic move for healthy individuals. HDHPs typically have lower premiums but higher out-of-pocket costs, making them suitable for those who rarely require medical care.

Negotiating with insurers is another avenue worth exploring. While not always successful, policyholders can attempt to negotiate premiums, especially if they have a good claims history or are considering switching providers. Finally, maintaining a healthy lifestyle can indirectly influence premiums. By reducing the risk of chronic conditions, individuals may qualify for lower rates or avoid premium surcharges associated with certain health factors.

Unemployed and Uninsured: Getting Medical Insurance Coverage

You may want to see also

Explore related products

$164.06 $245.95

![]()

Coverage updates and modifications

Health insurance policies are not static; they evolve annually to reflect changes in healthcare costs, medical advancements, and regulatory requirements. Coverage updates and modifications are a critical aspect of this evolution, ensuring that policies remain relevant and effective for policyholders. These changes can range from adjustments in premiums and deductibles to the inclusion or exclusion of specific treatments and services. Understanding these updates is essential for policyholders to make informed decisions during the renewal process.

One common area of modification is the scope of covered services. For instance, insurers may add new preventive care measures, such as expanded screenings for certain age groups (e.g., colorectal cancer screening starting at age 45 instead of 50) or coverage for emerging therapies like gene-based treatments for rare diseases. Conversely, some services may be removed from coverage if they are deemed experimental or no longer cost-effective. Policyholders should carefully review these changes to ensure their anticipated healthcare needs are still met. For example, if a family is planning to expand and the insurer reduces maternity coverage, exploring alternative plans or supplemental policies might be necessary.

Another significant aspect of coverage updates is the adjustment of cost-sharing parameters, such as copayments, coinsurance, and out-of-pocket maximums. Insurers often tweak these figures to balance affordability for policyholders with the need to manage rising healthcare costs. For instance, a plan might increase the copay for specialist visits from $40 to $50 while lowering the deductible by $200. Such changes can impact overall healthcare expenses, particularly for individuals with chronic conditions requiring frequent medical attention. A practical tip is to calculate your expected annual healthcare costs under the updated terms to assess the financial implications of these modifications.

Coverage modifications also frequently involve changes to provider networks. Insurers may add or remove healthcare providers, hospitals, and clinics from their networks, which can affect access to preferred doctors or specialists. For example, a policyholder might discover that their current primary care physician is no longer in-network, necessitating a switch to a new provider or paying higher out-of-network costs. To mitigate this, policyholders should cross-reference their preferred providers with the updated network list provided by the insurer during renewal.

Finally, regulatory changes often drive coverage updates, particularly in response to new laws or mandates. For instance, the inclusion of telehealth services became more widespread during the COVID-19 pandemic, with many insurers permanently expanding coverage for virtual consultations. Similarly, mental health parity laws may require insurers to offer equivalent coverage for mental health treatments as for physical health conditions. Staying informed about such regulatory-driven updates ensures that policyholders can fully leverage their benefits. A proactive approach, such as subscribing to insurer newsletters or attending informational webinars, can help policyholders stay ahead of these changes.

In summary, coverage updates and modifications are a dynamic and multifaceted aspect of health insurance renewals. By carefully reviewing changes to covered services, cost-sharing parameters, provider networks, and regulatory-driven updates, policyholders can ensure their insurance continues to meet their healthcare needs effectively. Taking a proactive and analytical approach to these modifications is key to making informed decisions during the renewal process.

Where to Sign Your Title When Submitting to Insurance Company

You may want to see also

Explore related products

![]()

Renewal deadlines and grace periods

Health insurance renewal deadlines are not just arbitrary dates—they are critical milestones that determine your coverage continuity. Missing these deadlines can lead to a lapse in insurance, leaving you vulnerable to unexpected medical expenses. Most insurers set renewal deadlines 30 to 60 days before the policy expires, though this varies by provider and plan type. For instance, employer-sponsored plans often align with the company’s fiscal year, while individual market plans may follow a calendar year. Understanding your specific deadline is the first step in avoiding coverage gaps.

Grace periods are a safety net, but they are not a long-term solution. Typically ranging from 15 to 90 days, these periods allow you to renew your policy after the deadline without losing coverage. However, relying on grace periods can be risky. During this time, you may still be uninsured, and any medical claims filed could be denied. Additionally, some insurers charge late fees or require a reinstatement process, adding unnecessary stress and cost. Proactive renewal ensures uninterrupted protection and avoids these complications.

For those with chronic conditions or ongoing treatments, missing a renewal deadline can be particularly detrimental. For example, a lapse in coverage could mean losing access to prescribed medications or specialist care, potentially exacerbating health issues. Seniors and individuals with pre-existing conditions should prioritize timely renewals, as reapplying for coverage after a lapse may involve stricter underwriting or higher premiums. Setting calendar reminders or enrolling in auto-renewal options, where available, can help mitigate these risks.

Comparatively, grace periods differ significantly across regions and insurers. In the U.S., the Affordable Care Act mandates a 90-day grace period for marketplace plans, but private insurers may offer shorter windows. In contrast, countries with universal healthcare systems often have more flexible renewal processes, as coverage is tied to residency rather than individual policies. Regardless of location, the takeaway is clear: treat renewal deadlines as non-negotiable and use grace periods as a last resort, not a strategy.

To navigate renewal deadlines effectively, follow these steps: first, mark your renewal date on all calendars you use—physical, digital, and mobile. Second, review your policy details at least 60 days in advance to assess any changes in premiums, coverage, or network providers. Third, prepare necessary documents and payment details early to avoid last-minute delays. Finally, confirm your renewal with your insurer to ensure processing. By staying organized and proactive, you can secure your health coverage without unnecessary stress or risk.

Anesthesia Coverage: Dental Work and Medical Insurance

You may want to see also

Explore related products

![]()

Impact of claims on renewal terms

Health insurance renewal terms are not set in stone; they are dynamic, influenced significantly by the claims history of the policyholder. Insurers meticulously review past claims to assess risk and adjust premiums or coverage conditions accordingly. A single high-value claim or multiple frequent claims can trigger premium hikes, reduced coverage, or even policy non-renewal. Conversely, a claim-free year often results in discounts or favorable renewal terms. This practice underscores the importance of understanding how claims directly impact future insurance costs and conditions.

Consider a 45-year-old policyholder who files a ₹5 lakh claim for a critical illness. At renewal, the insurer may increase the premium by 15-20% due to the perceived higher risk. Alternatively, a policyholder in their 30s with two minor claims (e.g., outpatient treatments totaling ₹30,000) might face a 10% premium increase or a higher deductible. Insurers use actuarial data to quantify risk, ensuring that policyholders with higher utilization bear a proportionate cost. This approach maintains the financial viability of the insurance pool while rewarding low-risk individuals.

To mitigate adverse renewal terms, policyholders can adopt strategic claim management. For instance, avoiding small claims (below ₹10,000) by paying out-of-pocket can preserve the no-claim bonus, which typically offers a 5-50% premium discount cumulatively over claim-free years. Additionally, opting for a voluntary deductible (e.g., ₹5,000-₹20,000) can reduce premiums by 10-25%. Policyholders should also review their sum insured annually, ensuring it aligns with their health needs without overpaying for unused coverage.

Comparatively, group health insurance policies often face different renewal dynamics. Employers may absorb premium increases or negotiate terms based on the collective claims experience of employees. However, individual policyholders lack this bargaining power, making proactive claim management essential. For example, a policyholder with a chronic condition like diabetes should prioritize preventive care to minimize claims, as frequent hospitalizations can lead to policy exclusions or non-renewal.

In conclusion, claims history is a pivotal factor in health insurance renewals, directly shaping premiums, coverage, and policy continuity. Policyholders must balance immediate claim needs with long-term renewal implications. Practical steps include strategic claim filing, opting for voluntary deductibles, and regular policy reviews. By understanding this relationship, individuals can navigate renewals effectively, ensuring sustainable and affordable health coverage.

Why 30-Day Insurance Policies Persist in the Auto Industry

You may want to see also

Frequently asked questions

Yes, most health insurance policies automatically renew for the following year unless you or the insurer decide to cancel or make changes to the policy. However, it’s important to review the terms and conditions, as some insurers may require explicit renewal confirmation.

Premiums may increase at renewal due to factors like inflation, changes in your age, medical history, or updates to the insurer’s pricing structure. It’s advisable to review the renewal notice for any changes in costs or coverage.

Yes, renewal is a good time to assess your coverage needs. You can often make changes to your plan, such as increasing or decreasing coverage, adding dependents, or switching to a different policy offered by the same insurer.

Missing the renewal deadline may result in a lapse of coverage. Some insurers offer a grace period, but if you fail to renew within that time, you may need to reapply for a new policy, which could involve additional underwriting or waiting periods. Always renew on time to avoid gaps in coverage.