Car insurance rates are determined by a multitude of factors, including age, gender, location, vehicle type, and driving history. While it is generally observed that insurance rates decrease as drivers gain experience, with significant drops around the ages of 19, 21, and 25, this is not always the case. Age is just one of many factors that insurance companies consider when determining rates. Other factors, such as driving history, location, and vehicle type, can also have a significant impact on insurance costs. It is important to note that insurance rates vary across different companies, and there is no one-size-fits-all answer when it comes to insurance rates. By maintaining a clean driving record, eliminating unnecessary coverage, and shopping around for multiple quotes, drivers can work towards obtaining lower insurance rates.

Explore related products

What You'll Learn

![]()

Car insurance rates for 25-year-olds

Car insurance rates typically decrease for 25-year-olds compared to younger drivers. This is because insurance companies consider drivers under 25 to be less experienced and more likely to get into accidents, making them riskier to insure. By 25, drivers are no longer considered "youthful operators" and are generally viewed as having more experience behind the wheel, resulting in lower rates.

However, it's important to note that age is just one factor among many that insurance companies consider when determining rates. Other factors include driving history, the type of car insured, and location. For example, some states, like Hawaii and Massachusetts, do not allow age to be a factor in determining insurance premiums. Additionally, driving infractions such as speeding tickets and accidents can significantly increase insurance costs, even for 25-year-olds.

The cost of car insurance for 25-year-olds can vary depending on the insurance company and the specific circumstances of the driver. On average, 25-year-olds pay $132 less per month for full coverage compared to 20-year-olds. USAA offers the cheapest rates for most 25-year-olds, with full coverage costing around $152 per month, but it is only available to military members, veterans, or their families. State Farm is another insurer with competitive rates for 25-year-olds, offering full coverage for approximately $159 per month.

To get the best rates, 25-year-olds should shop around and compare quotes from multiple insurance companies. They can also consider eliminating unnecessary coverage and asking for discounts. Maintaining a clean driving record is crucial, as it can significantly impact insurance rates. Additionally, 25-year-olds can benefit from staying on their parents' insurance policy if possible, as this can result in significant savings.

In summary, while car insurance rates typically decrease for 25-year-olds, it is not a guarantee, and other factors, such as driving history and location, also play a significant role in determining insurance costs.

U-Haul Insurance: Broken Strap, Big Trouble

You may want to see also

Explore related products

![]()

How to lower insurance rates at 25

While insurance rates typically decrease when you turn 25, this is not always the case. Here are some ways to lower your insurance rates at 25:

Shop around for quotes

Compare prices from different insurance companies to find the best rate for you. Get at least three quotes, either by calling companies directly or using online resources. Check your state insurance department's website for comparisons of prices charged by major insurers. Remember to consider the financial health and stability of the insurance company when making your decision.

Review your coverage

Consider eliminating unnecessary coverage. For example, if you drive an older car, you may want to drop collision and comprehensive coverage. Review your coverage at renewal to ensure it aligns with your current needs. You can also ask your insurer about discounts or ways to reduce your premium, such as increasing your deductible.

Bundle your insurance policies

Some companies offer discounts if you purchase multiple types of insurance, such as auto and home insurance, from them. You may also get a reduction if you have more than one vehicle insured with the same company.

Maintain a clean driving record

A good driving record can help you secure lower insurance rates. Avoid accidents, speeding tickets, and other driving infractions, as these can increase your cost of coverage. If you are a new driver at 25, consider taking a defensive driving course, which can result in a discount on your insurance.

Take advantage of group plans

Some companies offer reduced rates to drivers who get insurance through a group plan from their employers or other associations. Ask your employer and inquire with any groups or clubs you are a part of to see if this is an option.

It's important to note that insurance rates are complex and depend on various factors besides age. These factors include your driving history, credit history (where applicable), location, and the type of vehicle you drive. By being proactive and exploring different options, you can work towards lowering your insurance rates at 25.

Auto Insurance Companies: Billions Made, but How?

You may want to see also

Explore related products

![]()

Why insurance rates are high for under-25s

Insurance rates are high for under-25s due to a number of factors. One of the most significant factors is age. Younger drivers, especially teens, are considered to be high-risk by insurance companies due to their lack of driving experience and propensity for risk-taking on the road. This perception is supported by statistics, which show that younger drivers are more likely to be involved in accidents, with drivers aged 16 to 19 having almost three times as many fatal accidents per mile driven compared to other age groups. As a result, insurers charge higher rates to offset the potential costs associated with claims made by these younger drivers.

Another factor contributing to higher insurance rates for under-25s is gender. In states where insurers are allowed to consider gender when setting premiums, male drivers often face higher insurance costs than female drivers, especially before the age of 25. This is because young men tend to have more accidents than any other demographic, and insurance companies view males under 25 as more likely to engage in risky behaviour.

The type of vehicle driven can also impact insurance rates for under-25s. Higher-risk vehicles, such as sports cars, often lead to higher insurance premiums. This is because collision and comprehensive coverage amounts are typically higher for these types of vehicles. Additionally, if a young driver has only recently obtained their driver's license, they may be seen as a higher-risk client by insurers, resulting in higher rates.

It is important to note that insurance rates are not solely determined by age. Other factors, such as driving history, claims history, location, and credit history, can also influence insurance rates. Additionally, some states, such as Hawaii and Massachusetts, do not allow age to be considered when determining insurance premiums. However, for most under-25s, age is a significant factor in insurance rates, and they can expect to see a reduction in their insurance costs once they reach 25 years of age.

AAA Auto Insurance: Understanding Towing Coverage

You may want to see also

Explore related products

![]()

States with different insurance regulations

Car insurance rates typically decrease when individuals turn 25, as they are considered less risky drivers compared to younger drivers. However, this is not a guarantee, as rates are determined by various factors, including driving history, gender, and state regulations. Speaking of state regulations, let's take a look at how insurance regulations vary across different states in the US:

While almost every state in the US requires drivers to have car insurance, the specific regulations and minimum coverage levels vary. Here are some examples of how insurance regulations differ across states:

- Hawaii and Massachusetts: These two states prohibit the use of age as a factor in determining car insurance premiums. This means that insurance companies cannot charge higher rates based on age alone.

- California and Texas: These states differ in their minimum liability coverage requirements. California requires 15/30/5 coverage, while Texas offers higher protection with 30/60/25 coverage.

- Florida: As a no-fault insurance state, Florida requires insurance policies to cover the policyholder's injuries and damages, regardless of fault in an accident.

- New Hampshire: This is the only state that does not require car insurance. Instead, drivers must prove they have sufficient funds to cover accident-related costs, or they risk losing their driving privileges.

- Virginia: Previously, Virginia allowed drivers to opt out of traditional insurance by paying a $500 uninsured motorist fee.

- States with Health Insurance Mandates: The Affordable Care Act (ACA) of 2010 requires health insurance plans to extend coverage to children aged 18 to 26 years under their parents' policies. Prior to the ACA, 34 states had already enacted similar laws, with some states extending eligibility beyond 26 years and imposing premium caps.

These examples highlight the diverse insurance regulations across different states in the US. It's important to stay informed about the specific requirements and regulations in your state, especially if you're considering moving to a new state or purchasing a new insurance policy.

Auto-Insurance Auto-Cancellation: Understanding the Fine Print

You may want to see also

Explore related products

![]()

Other factors affecting insurance rates

While age is one of the biggest factors affecting insurance rates, there are several other factors that come into play when determining insurance rates.

Driving Experience

The more driving experience a person has, the less likely they are to get into an accident. This makes driving experience a significant factor in determining insurance rates. Drivers who start driving at 16 will have more experience by the time they turn 25, which is reflected in their insurance rates.

Driving History

A person's driving history, including accidents, speeding tickets, and other driving infractions, is a critical factor in determining their insurance rates. A clean driving record will result in lower rates, while a history of accidents or violations will lead to higher rates as insurers consider such individuals as high-risk drivers.

Vehicle Type

The type of vehicle driven also influences insurance rates. Luxury cars, sports cars, and vehicles with higher chances of inflicting damage in an accident tend to have higher premiums due to expensive repairs, higher replacement costs, and potential damage to other vehicles. In contrast, affordable and safe vehicles, such as a used Honda Civic, are generally cheaper to insure.

Location

Urban drivers often pay higher insurance prices than those in small towns or rural areas due to higher rates of vandalism, theft, and accidents. Additionally, where a car is parked (on the street or in a secure garage) and anti-theft features can also impact insurance rates.

Credit History

In most states, a person's credit history can influence their insurance rates. A lower credit score may result in higher insurance rates, as it predicts the likelihood of filing an insurance claim.

Gender

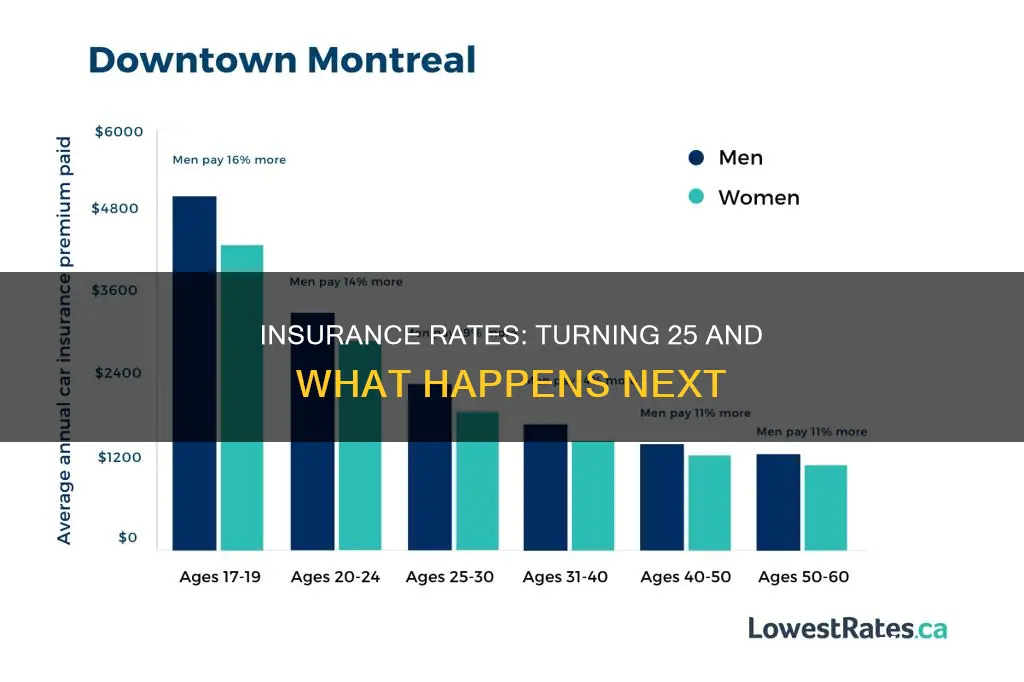

In states where insurers can factor gender into insurance rates, there is a difference in costs between male and female drivers. Car insurance rates for men decrease by 12% at age 25, while for women, the decrease is 9%.

It is important to note that insurance rates are complex and vary based on individual circumstances. These factors, along with age, play a significant role in determining insurance rates.

How Higher Deductibles Reduce Insurance Costs

You may want to see also

Frequently asked questions

Yes, insurance rates generally drop when a driver turns 25. This is because drivers under 25 are considered high-risk due to inexperience, whereas drivers aged 25 are likely to have more experience and are thus offered lower rates.

Aside from gaining driving experience, you can lower your insurance rates by improving your credit score, taking a defensive driving course, eliminating unnecessary coverage, shopping around for multiple quotes, and asking for discounts.

Insurance rates can increase due to factors such as driving history (e.g., accidents, speeding tickets), location, vehicle type, and age.