When it comes to purchasing a home, there are a multitude of factors to consider. One of the most crucial aspects is securing a mortgage, which entails evaluating various types of insurance. While medical insurance itself may not be a deciding factor in obtaining a mortgage, it can indirectly impact the process. This is because medical debt, if unpaid, can affect your credit score, which lenders consider when evaluating your eligibility for a loan. Additionally, mortgage protection insurance, also known as MPI or mortgage life insurance, is an option for homeowners to safeguard their investment and protect their families from financial hardship in the event of their death or disability. This type of insurance is designed to cover the remaining balance of the mortgage, providing peace of mind and ensuring that loved ones do not inherit debt.

| Characteristics | Values |

|---|---|

| Do mortgage companies look at medical insurance? | No, medical insurance is not considered by mortgage companies. |

| Do mortgage companies look at medical debt? | No, medical debt is not considered by mortgage companies except in the case of credit score. |

| What is Mortgage Protection Insurance (MPI)? | An insurance policy that pays off the remainder of your mortgage if you pass away or become disabled and unable to work. |

| Who does MPI pay out to? | MPI pays out to the mortgage lender, not the policyholder's family. |

| What is Private Mortgage Insurance (PMI)? | A type of mortgage insurance that protects the mortgage lender if the borrower stops making payments. |

| What is Federal Housing Administration mortgage insurance premium (MIP)? | A form of mortgage insurance imposed on all loans by the Federal Housing Administration (FHA). |

Explore related products

What You'll Learn

![]()

Medical debt and mortgage qualification

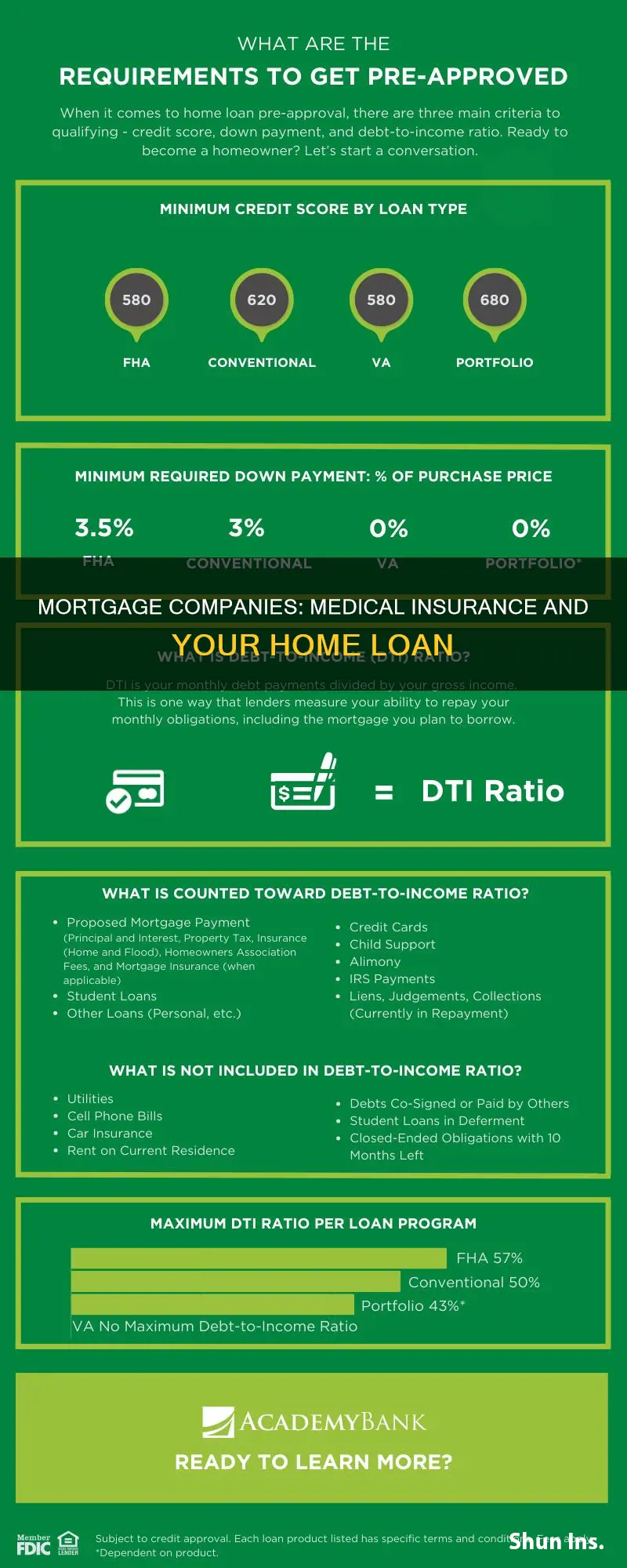

Medical debt can impact your ability to qualify for a mortgage, but it depends on several factors. Firstly, it's important to understand that medical debt is treated differently from other types of debt by lenders and credit bureaus. Medical debt is often the result of unforeseen circumstances and is not indicative of a borrower's financial responsibility. As a result, FICO scoring models, such as FICO 9, give less weight to unpaid medical collections and disregard paid collection accounts. This change can significantly improve an individual's credit score and increase their chances of mortgage approval.

However, it's worth noting that not all lenders use the latest credit scoring models, and some may still consider medical debt when evaluating a borrower's creditworthiness. Additionally, while medical debt may not be a direct factor in mortgage qualification, it can impact your overall credit score and debt-to-income ratio, which are crucial factors in the mortgage approval process. A poor credit score or a high debt-to-income ratio may make it more challenging to qualify for a conventional mortgage.

To improve your chances of mortgage qualification despite medical debt, it is advisable to review your credit reports and ensure the accuracy of any medical collections listed. If you find errors or debts that you do not owe, dispute them promptly. Additionally, consider taking advantage of healthcare savings opportunities, such as health savings accounts (HSAs) or flexible spending accounts (FSAs), to cover qualified medical expenses and reduce your out-of-pocket costs.

Furthermore, seeking alternative financing options, such as personal loans or medical credit cards with special financing offers, can help manage medical expenses without accumulating high-interest debt. It is also worth exploring mortgage options that are less dependent on traditional credit scores, such as Federal Housing Administration (FHA)-backed mortgages, which have eliminated medical debt from their underwriting considerations.

In summary, while medical debt may not be a direct barrier to mortgage qualification, it can impact your overall financial profile. By taking proactive steps to manage your medical debt and exploring alternative financing options, you can enhance your chances of qualifying for a mortgage and achieving your dream of homeownership.

How Insurance Can Contest Your Medical Bills

You may want to see also

Explore related products

![]()

Mortgage protection insurance

In the United States, if you buy a home with a loan backed by the Federal Housing Administration (FHA), you will owe a 1.75% upfront mortgage insurance premium, which you can pay when you close or add to your loan. You will also pay an annual premium, usually through your monthly payments. If you get a conventional loan, your lender may arrange for private mortgage insurance with a private company.

Prescription Refills: Insurance-Free Options for Patients

You may want to see also

Explore related products

![]()

Private mortgage insurance

PMI is arranged by the lender and provided by private insurance companies. It is required if you take out a conventional loan with a down payment of less than 20% of the purchase price. PMI can help you qualify for a loan that you might not otherwise be able to get. However, it increases the cost of your loan and does not protect you from foreclosure or a decrease in your credit score if you fall behind on payments.

You can avoid PMI by making a 20% down payment. Alternatively, you can consider a government-backed loan, such as a Federal Housing Administration (FHA) or U.S. Department of Agriculture (USDA) loan, which does not require PMI but has its own associated fees. You can also cancel your PMI under certain circumstances, such as when your mortgage balance reaches 78% of your home's value.

Mortgage protection insurance (MPI), also known as mortgage life insurance, is another type of insurance that covers your remaining home loan balance if you die before it is fully paid off. MPI can help protect your home and prevent your heirs from assuming payments or losing the home. However, it may not be the right choice for everyone as the death benefit is restricted to paying off the home loan and does not help with other expenses related to the borrower's passing.

Medicaid and College Sports: Understanding Insurance Coverage Options

You may want to see also

Explore related products

![]()

Federal Housing Administration mortgage insurance premium

Mortgage insurance is a requirement for borrowers who make a down payment of less than 20% of the purchase price of the home. It lowers the risk to the lender of offering a loan to the borrower, but it increases the cost of the loan. Mortgage insurance, regardless of type, protects the lender, not the borrower, in the event that the borrower falls behind on their payments.

Federal Housing Administration (FHA) mortgage insurance premium, also known as MIP, is paid by homeowners as mortgage insurance for FHA loans. It is required for all FHA loans. If you buy a home with an FHA-backed loan, you will owe a 1.75% upfront mortgage insurance premium, which you can pay at closing or add to your loan. After that, you will pay an annual premium, usually through your monthly payments. The length of time you will need to pay MIP depends on your down payment. If you put down 10% or more, you will pay for 11 years; otherwise, you will pay MIP for the life of the loan. Similar to PMI, MIP protects the lender if you fall behind on payments.

FHA loans are "insured" by the FHA, meaning that if a borrower defaults on the mortgage, the agency will compensate the lender for the outstanding balance. FHA mortgage insurance premiums go to the Mutual Mortgage Insurance Fund (MMIF), which the FHA uses to pay out claims to lenders seeking to recoup losses. FHA loan applicants are deemed riskier because they have lower credit scores, make smaller down payments, or both. Therefore, MIP helps lenders mitigate the risk of providing mortgages to these applicants and makes the FHA program possible.

Medicaid to Private Insurance: Switching Options in Maryland

You may want to see also

Explore related products

![]()

Mortgage protection insurance pros and cons

Mortgage protection insurance, also known as mortgage life insurance, is a type of credit life insurance that pays off the remaining balance of your mortgage when you die. It is not a mandatory insurance policy, but it can be beneficial for homeowners who want to protect their investment and prevent their family members from facing financial troubles.

Pros

Mortgage protection insurance can provide peace of mind and emotional relief, as it ensures that your loved ones won't have to worry about making mortgage payments after your death. It can also be relatively easy to obtain, as it typically doesn't require a medical exam or underwriting procedures. The insurance company sends the money directly to the lender, saving your family from the hassle of handling payments. Additionally, it can help your beneficiaries eliminate significant debt, giving them access to more equity in the home.

Cons

One of the main drawbacks of mortgage protection insurance is its lack of flexibility. The payout from the insurance goes directly to the lender, and your beneficiaries have no control over how the money is spent. This means that it won't cover other expenses or debts that your loved ones may need help with. The payout also decreases over time as you pay down your mortgage, while your premiums usually remain the same. As a result, mortgage protection insurance can be more expensive than other types of insurance policies, such as term life insurance, which offer more coverage and flexibility.

While mortgage protection insurance can provide emotional relief and ensure your loved ones keep the house, it may not be the most cost-effective option. It's important to carefully consider your needs and explore alternative insurance policies, such as term life insurance, which can offer more flexibility and control over the payout.

Life Insurance and Medicaid: What Happens After Death?

You may want to see also

Frequently asked questions

No, mortgage companies do not look at medical insurance. However, they may require you to have homeowners insurance to protect your property and belongings from damage.

Mortgage protection insurance (MPI) is an insurance policy that helps your family make mortgage payments if you, the policyholder, die before your mortgage is fully paid off. MPI can also cover your mortgage payments for a limited time if you lose your job or become disabled after an accident.

MPI pays your lender the remaining mortgage balance after your death. The insurance company typically sends the money directly to the lender, so your family doesn't have to handle any payments.

MPI can provide peace of mind and emotional relief, knowing that your family won't be burdened with mortgage payments if something happens to you. It can also be easier to obtain than life insurance, as it usually doesn't require a medical exam or underwriting procedures.

MPI may not be a good deal financially, as the premium remains the same while the death benefit declines as your loan balance decreases. Additionally, the payout is restricted to the home loan, and your family may need the money for other expenses related to your passing.