When filing taxes in the United States, the topic of health insurance often arises due to the Affordable Care Act (ACA), which requires most taxpayers to have qualifying health coverage or face a penalty. The IRS includes questions about health insurance on tax forms, specifically Form 1040, to determine compliance with the ACA's individual mandate. Taxpayers must indicate whether they had health insurance during the tax year, claim exemptions if applicable, or pay the shared responsibility payment if uninsured. Additionally, those who purchased insurance through the Health Insurance Marketplace may need to report advance premium tax credits or reconcile them on their return. Understanding these requirements is crucial to accurately completing tax filings and avoiding potential penalties.

| Characteristics | Values |

|---|---|

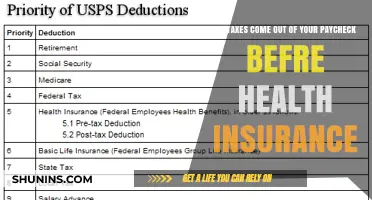

| Tax Filing Requirement | When filing federal taxes in the U.S., taxpayers are required to indicate whether they had health insurance coverage during the tax year. |

| Individual Shared Responsibility Payment (ISRP) | The ISRP penalty for not having health insurance was reduced to $0 starting in 2019, but some states (e.g., California, Massachusetts, New Jersey, Rhode Island, and Washington D.C.) have their own mandates and penalties. |

| Form 1095 Series | Taxpayers may receive Form 1095-A (Health Insurance Marketplace), 1095-B (Health Coverage), or 1095-C (Employer-Provided Health Insurance) to report health insurance coverage. |

| Line 61 on Form 1040 | Taxpayers must check a box on Line 61 of Form 1040 to indicate if they had health insurance coverage for the entire year. |

| Exemptions | Certain individuals may qualify for exemptions from the health insurance requirement, such as those with low income, members of certain religious sects, or those experiencing hardships. |

| State-Specific Requirements | Some states have their own health insurance mandates and may require additional reporting or documentation on state tax returns. |

| Premium Tax Credit (PTC) | Taxpayers who purchased health insurance through the Marketplace may be eligible for the PTC, which can be claimed or reconciled on their tax return using Form 8962. |

| Reporting Changes | Taxpayers must report changes in health insurance coverage, income, or household size to the Marketplace throughout the year to avoid discrepancies during tax filing. |

| IRS Verification | The IRS verifies health insurance coverage through data matching with insurance providers, employers, and the Health Insurance Marketplace. |

| Penalties for Non-Compliance | In states with mandates, penalties for not having health insurance can vary and are typically assessed on state tax returns. |

Explore related products

What You'll Learn

- ACA Individual Mandate: Does tax filing require proof of health insurance under the Affordable Care Act

- Tax Penalties: Are there penalties for not having health insurance when filing taxes

- Premium Tax Credits: How do health insurance premiums affect tax credits or deductions

- Form 1095: What is Form 1095, and is it necessary for tax filing

- Health Savings Accounts: How do HSAs impact taxable income and deductions

![]()

ACA Individual Mandate: Does tax filing require proof of health insurance under the Affordable Care Act?

Under the Affordable Care Act (ACA), the individual mandate initially required most Americans to have qualifying health insurance or pay a penalty when filing taxes. This penalty, known as the Shared Responsibility Payment, was enforced through the tax system, with filers reporting their health insurance status on Form 1040. However, starting in 2019, the federal penalty for not having health insurance was reduced to $0, effectively eliminating the financial consequence for non-compliance at the federal level. Despite this change, some states, like California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia, have implemented their own individual mandates with associated penalties, which may still require proof of health insurance during tax filing.

For federal tax purposes, the IRS no longer requires individuals to provide proof of health insurance or pay a penalty for lacking coverage. This shift means that taxpayers are no longer obligated to report their health insurance status on their federal tax returns. However, it’s crucial to understand that the ACA’s requirement to maintain health insurance remains in place, even without a federal penalty. This distinction highlights the importance of staying informed about state-specific mandates, as they can significantly impact your tax obligations.

If you reside in a state with its own individual mandate, tax filing becomes more complex. For example, California residents must report their health insurance status on state tax forms and may face a penalty if they lack qualifying coverage. To comply, individuals must obtain Form 1095, which documents their health insurance coverage for the year. This form is typically provided by employers, insurance companies, or the health insurance marketplace. Failure to provide proof of coverage in these states can result in fines, making it essential to retain and submit the necessary documentation during tax season.

Practical tips for navigating this requirement include keeping detailed records of your health insurance coverage throughout the year, including policy numbers, provider names, and coverage periods. If you purchase insurance through the marketplace, ensure you understand whether your plan qualifies under your state’s mandate. Additionally, consult a tax professional or use tax software that accounts for state-specific requirements to avoid errors. While the federal mandate no longer imposes a penalty, state-level mandates underscore the continued relevance of health insurance in tax filing for certain taxpayers.

In summary, while federal tax filing no longer requires proof of health insurance due to the elimination of the ACA’s penalty, state mandates in specific regions demand compliance. Taxpayers in these states must be diligent in reporting their coverage to avoid penalties. Understanding the interplay between federal and state requirements is key to navigating this aspect of tax filing accurately and efficiently.

Adding Your Spouse to Health Insurance After Job Loss: A Guide

You may want to see also

Explore related products

![]()

Tax Penalties: Are there penalties for not having health insurance when filing taxes?

In the United States, the Affordable Care Act (ACA) introduced a shared responsibility payment, often referred to as the individual mandate, which required most individuals to have qualifying health insurance coverage or face a tax penalty. This penalty was designed to encourage widespread insurance enrollment and reduce the number of uninsured individuals. However, the Tax Cuts and Jobs Act of 2017 effectively eliminated this federal penalty starting in 2019, meaning that as of the 2020 tax year, there is no longer a federal tax penalty for not having health insurance.

Despite the elimination of the federal penalty, some states have implemented their own health insurance mandates to ensure residents maintain coverage. For instance, California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia have enacted state-level penalties for uninsured individuals. These penalties vary in structure and amount, often mirroring the previous federal model. For example, California’s penalty for 2023 is calculated as either a flat fee of $800 per adult and $400 per child, or 2.5% of household income above the state’s tax filing threshold, whichever is greater. Taxpayers in these states must report their health insurance status on their state tax returns and may face penalties if they lack qualifying coverage.

For those filing federal taxes, the absence of a penalty does not mean health insurance is irrelevant. The IRS still requires taxpayers to indicate whether they had health insurance coverage during the tax year. This is done by checking a box on Form 1040, the primary tax return form. While there is no federal penalty for being uninsured, this information helps the IRS track compliance with state mandates and other health-related tax provisions, such as premium tax credits for those purchasing insurance through the Health Insurance Marketplace.

Understanding the interplay between health insurance and taxes is crucial, especially for residents of states with individual mandates. For example, if you live in Massachusetts and go without health insurance for three consecutive months, you could face a penalty of up to 50% of the premium for the least expensive available plan. To avoid such penalties, individuals should explore coverage options, including employer-sponsored plans, Medicaid, or plans purchased through state or federal marketplaces. Additionally, keeping detailed records of insurance coverage throughout the year can simplify the tax filing process and ensure compliance with state requirements.

In conclusion, while the federal tax penalty for not having health insurance has been eliminated, state-level penalties remain a significant consideration for many taxpayers. Being proactive about understanding both federal and state regulations can help individuals avoid unexpected financial consequences. For those in states without mandates, maintaining health insurance is still advisable to protect against high medical costs. Consulting a tax professional or using reputable tax software can provide personalized guidance tailored to your specific situation and location.

Getting Medical Insurance for Your Children: A Guide

You may want to see also

Explore related products

![]()

Premium Tax Credits: How do health insurance premiums affect tax credits or deductions?

Health insurance premiums can significantly impact your tax situation, particularly through premium tax credits. These credits, designed to make health insurance more affordable, are a crucial aspect of the tax code for many individuals and families. Understanding how premiums influence these credits is essential for maximizing your tax benefits and ensuring compliance with IRS regulations.

Eligibility and Calculation: Premium tax credits are primarily associated with health insurance plans purchased through the Health Insurance Marketplace. To qualify, your household income must fall within a specific range, typically between 100% and 400% of the federal poverty level. The credit amount is calculated based on a sliding scale, meaning the lower your income, the larger the credit. For instance, a family of four with an income of $50,000 might receive a more substantial credit than a similar family earning $80,000. The IRS provides detailed tables and calculators to estimate your potential credit, ensuring you can plan your finances accordingly.

Impact of Premiums: The cost of your health insurance premium directly affects the tax credit calculation. The IRS uses the second-lowest-cost Silver plan in your area as a benchmark. If you choose a plan with a higher premium, you'll pay the difference, but if your plan's premium is lower, the credit will cover the entire cost, and any excess can be refunded or used to offset other taxes. For example, if the benchmark plan costs $400 per month, and your chosen plan is $500, you'll pay $100, and the credit will cover the remaining $400. This mechanism ensures that the credit adjusts to your specific insurance choices.

Advanced Payments and Reconciliation: Taxpayers have the option to receive premium tax credits in advance, directly reducing their monthly insurance payments. However, this requires careful estimation of your annual income. If your actual income differs significantly from the estimate, you may need to repay some of the credit when filing taxes. Conversely, if you've underpaid, you'll receive the additional credit as a refund. This process, known as reconciliation, highlights the importance of accurate income reporting and the potential for both benefits and liabilities when managing premium tax credits.

Strategic Considerations: To optimize your tax credits, consider the following strategies. First, review your income and family size annually to ensure you're applying for the correct credit amount. Second, compare health insurance plans not only based on coverage but also on how they interact with tax credits. Sometimes, a slightly more expensive plan might result in a larger credit, effectively reducing your overall costs. Lastly, if your income fluctuates, consider consulting a tax professional to navigate the complexities of premium tax credits and avoid potential pitfalls during tax season.

In summary, health insurance premiums play a pivotal role in determining the value of premium tax credits, offering a means to make healthcare more accessible. By understanding the interplay between premiums and credits, taxpayers can make informed decisions, potentially reducing their healthcare expenses and optimizing their tax returns. This knowledge is particularly valuable for those with variable incomes or those exploring different health insurance options.

Top ACA-Compliant Health Insurance Providers in Virginia: Your Guide

You may want to see also

Explore related products

![]()

Form 1095: What is Form 1095, and is it necessary for tax filing?

In the realm of tax filing, Form 1095 serves as a critical document for individuals and families who had health insurance coverage during the tax year. This form, provided by your insurance provider or employer, verifies that you and your dependents maintained minimum essential coverage, as required by the Affordable Care Act (ACA). There are three variants of Form 1095: 1095-A for marketplace coverage, 1095-B for coverage through an insurance provider, and 1095-C for employer-sponsored plans. Each version contains specific details about your coverage, including the period of coverage and the individuals insured.

Understanding whether Form 1095 is necessary for your tax filing depends on your situation. If you purchased insurance through the Health Insurance Marketplace, you must report information from Form 1095-A when filing taxes to reconcile any advance premium tax credits received. For those with employer-sponsored or private insurance, Forms 1095-B and 1095-C are primarily for your records, as the IRS uses them to confirm compliance with the individual mandate. While you generally don’t need to attach these forms to your tax return, retaining them is essential in case of an IRS inquiry.

A common misconception is that Form 1095 is required for everyone. In reality, its necessity hinges on your health insurance source and whether you received subsidies. For instance, if you had Medicaid or Medicare, you won’t receive a Form 1095, as these programs are exempt from reporting requirements. Similarly, if you were uninsured for part of the year, you might face a penalty or qualify for an exemption, but Form 1095 wouldn’t apply. Thus, the form’s relevance is situational, not universal.

Practical tips for handling Form 1095 include verifying its accuracy upon receipt. Check names, coverage dates, and policy details against your records. Errors can lead to complications during tax filing or reconciliation of credits. If discrepancies arise, contact your provider or employer promptly for a corrected form. Additionally, keep all Form 1095 versions for at least three years, as they may be needed for future tax audits or amendments.

In conclusion, Form 1095 is a specialized document that bridges health insurance and tax obligations. While not everyone needs it for filing, its role in verifying coverage and reconciling subsidies makes it indispensable for certain taxpayers. By understanding its purpose, variants, and practical implications, you can navigate its requirements efficiently and avoid potential pitfalls during tax season.

Does Your Health Insurance Cover Gastric Bypass? What to Know

You may want to see also

Explore related products

![]()

Health Savings Accounts: How do HSAs impact taxable income and deductions?

Health Savings Accounts (HSAs) are a powerful tool for managing healthcare costs while offering significant tax advantages. Contributions to an HSA are tax-deductible, reducing your taxable income for the year. For instance, if you contribute $3,650 (the 2023 limit for individuals) to your HSA and fall in the 22% tax bracket, you save $803 in federal taxes. This deduction applies regardless of whether you itemize deductions or take the standard deduction, making HSAs uniquely beneficial.

Beyond the upfront deduction, HSAs provide tax-free growth and withdrawals when used for qualified medical expenses. This triple tax advantage—deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses—sets HSAs apart from other savings vehicles. However, it’s crucial to use funds for eligible expenses, such as doctor visits, prescriptions, or medical equipment. Non-qualified withdrawals before age 65 incur a 20% penalty plus income tax, though the penalty drops to ordinary income tax after age 65.

To maximize HSA benefits, consider your healthcare needs and financial goals. For example, if you’re healthy and have low medical expenses, treat your HSA as a long-term investment account. Let contributions grow tax-free, and pay current medical expenses out-of-pocket. This strategy allows your HSA to accumulate funds for future healthcare costs or even retirement, as HSAs can be used to cover Medicare premiums or long-term care expenses later in life.

One common mistake is failing to track eligible expenses. Keep detailed records of medical bills, prescriptions, and other qualified expenses to ensure you’re using HSA funds correctly. Additionally, if you’re self-employed or have a high-deductible health plan (HDHP), an HSA can be particularly advantageous. For 2023, HDHPs must have a deductible of at least $1,500 for individuals or $3,000 for families, making HSAs an ideal pairing for these plans.

In summary, HSAs offer a unique way to reduce taxable income, save for healthcare expenses, and invest for the future. By understanding their tax benefits, eligible expenses, and strategic use, you can leverage HSAs to optimize your financial health. Whether you’re saving for immediate needs or planning for retirement, an HSA is a versatile tool worth considering in your tax and healthcare strategy.

Is Your Health Insurance Affordable? A Simple Calculation Guide

You may want to see also

Frequently asked questions

Yes, the IRS requires you to report whether you had qualifying health insurance coverage for the tax year. This is done using Form 1095, which provides details about your health insurance coverage.

If you didn’t have health insurance and don’t qualify for an exemption, you may be subject to the Shared Responsibility Payment (penalty). However, as of 2019, the federal penalty for not having health insurance has been eliminated, though some states may still impose their own penalties.

You report health insurance coverage by checking the appropriate box on Form 1040 or 1040-SR. If you received a Form 1095-A, 1095-B, or 1095-C from your insurance provider or employer, you’ll use this information to verify your coverage status.