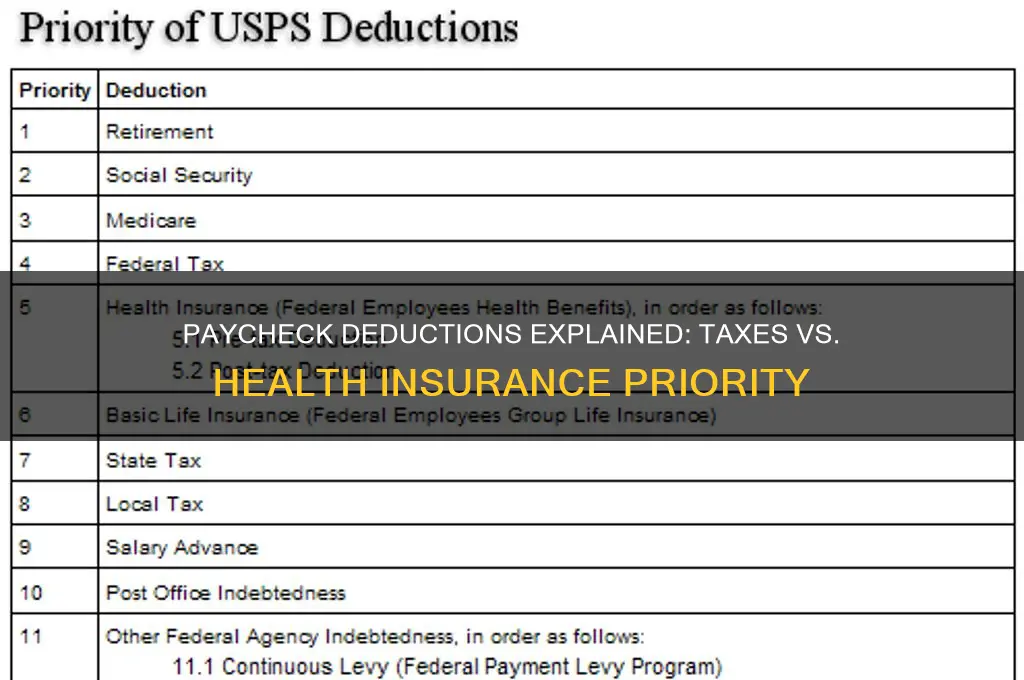

When examining your paycheck, it's essential to understand the order in which deductions are taken, as this can impact your take-home pay. One common question is whether taxes are deducted before health insurance premiums. Generally, federal, state, and local taxes are withheld from your gross income first, followed by pre-tax deductions such as health insurance premiums, which are typically taken out before taxes are calculated. This means that your taxable income is reduced by the amount of your health insurance premium, potentially lowering your overall tax liability. Understanding this sequence can help you better comprehend your pay stub and make informed decisions about your benefits and financial planning.

| Characteristics | Values |

|---|---|

| Tax Withholding Order | Taxes are generally deducted from your paycheck before health insurance premiums. This is because tax withholdings (federal, state, Social Security, Medicare) are mandatory and prioritized by law. |

| Deduction Priority | 1. Taxes (Federal, State, FICA) 2. Pre-tax deductions (e.g., 401(k), HSA) 3. Health insurance premiums 4. Post-tax deductions (e.g., Roth 401(k), wage garnishments) |

| Pre-tax Health Insurance | If health insurance is offered through your employer and paid with pre-tax dollars, it is deducted after taxes but before post-tax deductions. |

| Post-tax Health Insurance | Rarely, health insurance premiums may be deducted post-tax, but this is less common and depends on the employer's plan setup. |

| Impact on Taxable Income | Pre-tax health insurance premiums reduce your taxable income, lowering your overall tax liability. |

| Employee vs. Employer Contributions | Employer contributions to health insurance are generally not taxed, while employee contributions may be pre- or post-tax depending on the plan. |

| Pay Stub Visibility | Your pay stub will typically show taxes deducted first, followed by health insurance premiums and other deductions. |

| Legal Requirement | Employers are required to withhold taxes first, as per IRS regulations, before any other deductions. |

Explore related products

What You'll Learn

![]()

Pre-tax deductions vs. post-tax deductions

Understanding the difference between pre-tax and post-tax deductions is crucial for maximizing your take-home pay and minimizing your tax liability. Pre-tax deductions are taken from your gross income before taxes are calculated, effectively lowering your taxable income. Common examples include contributions to health insurance, retirement plans like a 401(k), and flexible spending accounts (FSAs). For instance, if your annual salary is $60,000 and you contribute $3,000 to a health savings account (HSA) pre-tax, your taxable income drops to $57,000. This reduction can lower your overall tax burden, leaving you with more money in your pocket.

Post-tax deductions, on the other hand, are taken from your income after taxes have been withheld. These deductions do not reduce your taxable income but may offer other benefits. Examples include Roth 401(k) contributions, wage garnishments, and certain voluntary benefits like life insurance. For example, if you earn $50,000 annually and contribute $2,000 post-tax to a Roth 401(k), your taxable income remains $50,000, but the Roth contribution grows tax-free, providing a different long-term advantage.

A key takeaway is that pre-tax deductions are generally more advantageous for reducing immediate tax liability, while post-tax deductions may offer benefits like tax-free growth or flexibility in certain financial planning scenarios. For instance, if you expect to be in a higher tax bracket in retirement, a Roth 401(k) (post-tax) might be preferable. Conversely, if you’re in a high tax bracket now, pre-tax contributions to a traditional 401(k) could save you more in taxes today.

To optimize your paycheck, evaluate your financial goals and tax situation. If you’re unsure, consult a tax professional or use online calculators to compare scenarios. For example, contributing the maximum allowed to pre-tax accounts like an HSA ($3,850 for individuals in 2023) can significantly reduce your taxable income while providing a tax-free fund for medical expenses. Conversely, if you’re focused on tax-free retirement income, prioritize post-tax options like a Roth IRA or Roth 401(k).

In practice, review your pay stub to ensure deductions are applied correctly. Mistakes in categorization (e.g., a pre-tax deduction coded as post-tax) can cost you money. For instance, if your health insurance premium is mistakenly treated as post-tax, you’ll pay unnecessary taxes on that amount. Regularly audit your payroll deductions and adjust contributions annually based on changes in income, tax laws, or personal circumstances. This proactive approach ensures you’re leveraging pre-tax and post-tax deductions to their fullest potential.

Herpes Medication Costs Without Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Health insurance premiums and payroll taxes

Payroll deductions for health insurance premiums and taxes follow a specific hierarchy, often leaving employees wondering about the sequence. Typically, payroll taxes—such as federal income tax, Social Security, and Medicare—are deducted before health insurance premiums. This order is governed by IRS regulations and employer payroll systems, ensuring compliance with tax laws. Understanding this sequence is crucial for budgeting and financial planning, as it directly impacts your take-home pay.

Consider the mechanics of payroll processing. When your employer calculates your gross pay, deductions are applied in a predetermined order. Payroll taxes are prioritized because they are statutory obligations, meaning they must be withheld to avoid penalties. Health insurance premiums, while essential, are voluntary contributions based on your election during open enrollment. For example, if your gross pay is $2,000 biweekly, approximately 7.65% is deducted for Social Security and Medicare, followed by federal and state income taxes, before your health insurance premium of, say, $150 is subtracted.

From a financial planning perspective, this sequence has practical implications. Since payroll taxes reduce your taxable income, they indirectly lower the amount available for health insurance premiums. For instance, if you’re in the 22% federal tax bracket, every dollar withheld for taxes reduces your premium contribution pool. To optimize your budget, calculate your net pay after taxes and then allocate funds for health insurance. Tools like payroll calculators or consultations with HR can provide clarity on exact deductions.

A comparative analysis reveals that while both payroll taxes and health insurance premiums reduce your paycheck, their purposes differ. Payroll taxes fund public programs like Social Security and Medicare, offering long-term benefits. Health insurance premiums, on the other hand, provide immediate access to healthcare services, protecting against high medical costs. For employees aged 26–65, balancing these deductions is critical, especially as healthcare costs rise. For example, opting for a high-deductible health plan (HDHP) with a Health Savings Account (HSA) can offset tax burdens while managing premiums.

In conclusion, payroll taxes take precedence over health insurance premiums in paycheck deductions, driven by legal requirements and payroll processing protocols. This order influences your financial decisions, from budgeting to selecting health plans. By understanding this hierarchy and its implications, you can better navigate your compensation structure and make informed choices to maximize your financial well-being.

Does Your Health Insurance Cover Chiropractic Care? What to Know

You may want to see also

Explore related products

![]()

Order of paycheck deductions explained

Taxes and health insurance are two of the most significant deductions from your paycheck, but their order of subtraction isn’t arbitrary. Employers follow a structured sequence mandated by federal and state laws, ensuring compliance with tax regulations and benefit administration. Understanding this order clarifies why certain amounts appear before others on your pay stub. For instance, federal income tax is typically deducted first, followed by Social Security and Medicare taxes, before health insurance premiums are subtracted. This sequence prioritizes legal obligations over voluntary benefits, ensuring funds are allocated correctly.

The process begins with pre-tax deductions, which reduce your taxable income. These include federal, state, and local taxes, as well as contributions to retirement plans like a 401(k) or health savings accounts (HSAs). Health insurance premiums are often deducted pre-tax, lowering your taxable income and saving you money. For example, if your annual salary is $50,000 and your health insurance premium is $300 per month, contributing $3,600 annually pre-tax reduces your taxable income to $46,400. This strategic deduction order maximizes your take-home pay by minimizing tax liability.

After pre-tax deductions, post-tax deductions are applied. These include items like wage garnishments, certain retirement contributions (if Roth), or voluntary life insurance premiums. Notably, if you opt for a health insurance plan that isn’t pre-tax eligible (rare but possible), it would fall into this category. However, most employer-sponsored health plans are pre-tax, making this scenario uncommon. Understanding this distinction helps you anticipate how much of your gross pay remains after all deductions.

A practical tip for employees is to review your pay stub regularly to ensure deductions align with your elections. For instance, if you’ve chosen a high-deductible health plan with an HSA, confirm both the premium and HSA contribution are deducted pre-tax. Mistakes in deduction order can lead to overpayment of taxes or underfunding of benefits. Additionally, if you’re enrolled in multiple benefits (e.g., dental, vision, or disability insurance), verify their pre- or post-tax status, as this affects your net pay.

In summary, the order of paycheck deductions is a deliberate process designed to prioritize legal obligations and optimize tax efficiency. Taxes come before health insurance premiums, primarily because tax liabilities are non-negotiable, while health insurance is a benefit election. By understanding this sequence, you can better manage your finances, ensure compliance, and maximize the value of your compensation package. Always consult your HR department or a tax professional if you have questions about your specific deductions.

Do Insurance Agents Sell Health Insurance? Understanding Their Role and Services

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71OcM906MLL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![TurboTax Premier Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71ofxs16-9L._AC_UL320_.jpg)

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UL320_.jpg)

![]()

Impact of tax withholding on net pay

Tax withholding directly shapes your net pay, often more significantly than other deductions like health insurance. When your employer calculates your paycheck, federal and state income taxes, Social Security, and Medicare are typically withheld before any voluntary deductions, including health insurance premiums. This sequence means your taxable income is reduced by these mandatory withholdings first, which can lower the amount subject to additional deductions. For instance, if your gross pay is $5,000 and federal taxes withhold $800, your remaining income is $4,200 before health insurance premiums are deducted. Understanding this order is crucial for budgeting and financial planning.

The impact of tax withholding on net pay varies based on factors like your filing status, allowances claimed on your W-4, and taxable income. For example, a single filer earning $60,000 annually with one allowance might see 22% federal tax withholding, while a married filer with two allowances could have a lower rate. This difference can result in hundreds of dollars more or less in each paycheck. To optimize your net pay, review your W-4 annually, especially after life changes like marriage, divorce, or having a child. Adjusting allowances can reduce over-withholding, ensuring you’re not giving the IRS an interest-free loan.

A practical tip for managing tax withholding is to use the IRS Tax Withholding Estimator, a tool that helps you determine the right number of allowances or additional withholding to claim. For instance, if you consistently receive large refunds, consider increasing your allowances to boost your take-home pay throughout the year. Conversely, if you owe taxes annually, reduce allowances or request additional withholding to avoid penalties. Pairing this strategy with health insurance planning—like choosing a high-deductible plan with lower premiums—can maximize your net pay while maintaining coverage.

Comparatively, while health insurance premiums reduce your net pay, they are often more predictable and controllable than tax withholdings. Premiums are typically fixed monthly amounts, whereas tax withholding fluctuates based on income and deductions. For example, a $200 monthly health insurance premium remains constant, whereas tax withholding might increase if you receive a bonus or overtime pay. By focusing on tax withholding adjustments, you can achieve more immediate and significant changes to your net pay than by altering health insurance plans alone.

In conclusion, tax withholding plays a pivotal role in determining your net pay, often more so than health insurance deductions. By understanding the order of deductions, adjusting your W-4, and using tools like the IRS Tax Withholding Estimator, you can take control of your take-home pay. Pairing these strategies with thoughtful health insurance choices creates a holistic approach to maximizing your financial well-being. Start by reviewing your current withholdings today—small adjustments can lead to substantial long-term benefits.

Blue Cross Medicare Supplemental Insurance: Annual Benefits?

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![]()

Employer role in payroll deductions

Employers play a pivotal role in managing payroll deductions, acting as intermediaries between employees and various withholding entities. Their responsibilities extend beyond simply issuing paychecks; they must accurately calculate, withhold, and remit deductions such as federal and state taxes, Social Security, Medicare, and voluntary contributions like health insurance premiums. This process requires meticulous attention to detail, as errors can result in financial penalties or employee dissatisfaction. For instance, federal income tax withholding is determined by the employee’s W-4 form, while health insurance deductions are based on the plan selected during open enrollment. Employers must prioritize these tax withholdings, as they are legally mandated and typically processed before voluntary deductions like health insurance.

Consider the sequence of payroll deductions: taxes are almost always prioritized over other withholdings. Federal and state taxes, along with Social Security and Medicare contributions, are deducted first because they are non-negotiable obligations. Health insurance premiums, on the other hand, are voluntary and come out of the employee’s net pay after taxes. For example, if an employee earns $1,000 biweekly, approximately 20-30% may be withheld for taxes, leaving around $700-$750 before health insurance deductions are applied. Employers use payroll software to automate this process, ensuring compliance with IRS regulations and reducing the risk of errors. This hierarchical approach ensures that legal obligations are met before discretionary benefits are funded.

From a practical standpoint, employers must stay informed about changing tax laws and benefit structures to avoid costly mistakes. For instance, the Tax Cuts and Jobs Act of 2017 altered federal withholding rates, requiring employers to update their payroll systems promptly. Similarly, health insurance premiums fluctuate annually, necessitating adjustments during open enrollment periods. Employers should communicate these changes clearly to employees, providing pay stubs that break down deductions for transparency. A proactive approach includes offering educational resources, such as workshops or online tools, to help employees understand their paychecks. This not only fosters trust but also reduces inquiries about discrepancies.

Comparatively, small businesses often face greater challenges in managing payroll deductions due to limited resources. Unlike large corporations with dedicated HR departments, small employers may rely on manual calculations or outsourced payroll services. This can lead to delays or inaccuracies, particularly during tax season or when updating benefit plans. To mitigate risks, small businesses should invest in user-friendly payroll software or consult tax professionals. For example, platforms like Gusto or QuickBooks offer automated tax filings and benefit management, streamlining the process for employers with fewer than 50 employees. By leveraging technology, even small businesses can fulfill their payroll obligations efficiently.

In conclusion, the employer’s role in payroll deductions is multifaceted, requiring precision, compliance, and communication. By prioritizing tax withholdings over voluntary deductions like health insurance, employers ensure legal obligations are met while supporting employee benefits. Whether through automated systems or educational initiatives, proactive management of payroll deductions fosters a transparent and trusting workplace. For employers, staying informed and utilizing available tools is key to navigating this complex responsibility successfully.

Nonprofit Reimbursement for Employee Medical Insurance: What's Allowed?

You may want to see also

Frequently asked questions

Yes, taxes are typically deducted from your paycheck before health insurance premiums are taken out. Payroll taxes, such as federal and state income taxes, Social Security, and Medicare, are prioritized and withheld first.

The order of deductions can slightly impact your take-home pay. Since taxes are deducted first, your taxable income is reduced before health insurance premiums are calculated. This may result in slightly lower tax withholding if your health insurance is deducted pre-tax.

No, the order of deductions is determined by your employer’s payroll system and federal regulations. Taxes are always deducted first, followed by pre-tax deductions like health insurance, and then post-tax deductions.

![TurboTax Business Desktop Edition 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71iKclcd6ML._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UL320_.jpg)

![TurboTax Deluxe Online Edition 2025, Federal Tax Return [Activation Code]](https://m.media-amazon.com/images/I/61bFazlntVL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)