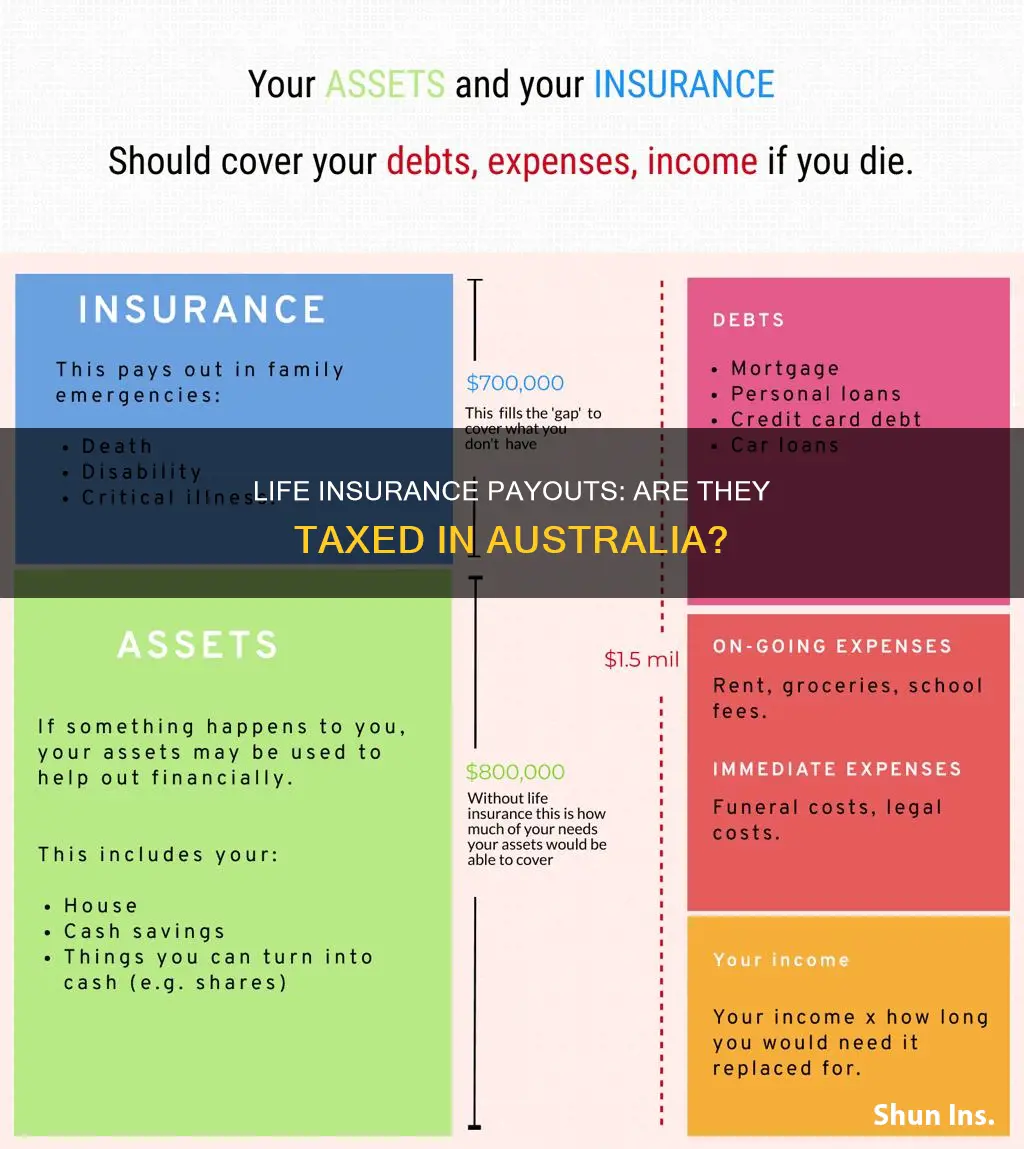

Life insurance can provide a financial safety net for your family when you die, but are they taxed on that money in Australia? The short answer is: it depends. If your policy is held outside of superannuation, your beneficiaries will generally not pay taxes on a life insurance payout. However, if your cover is held inside superannuation, your beneficiaries may be taxed on the payout if they are not financially dependent on you.

| Characteristics | Values |

|---|---|

| Are life insurance payouts taxed in Australia? | Generally, life insurance payouts are tax-free, especially when they are going to a financial dependent such as a spouse or child. |

| Are life insurance premiums tax-deductible? | Life insurance, critical illness and TPD insurances purchased outside your superannuation are not tax-deductible. TPD insurance purchased within your superannuation is tax-deductible. Income protection insurance is usually tax-deductible regardless of how you purchased it. |

| How does tax apply to life insurance payouts or benefits? | It depends on the policy ownership structure: inside or outside of superannuation. For instance, a life insurance benefit paid directly to your spouse or child is generally not subject to taxation when the policy is held outside of superannuation. |

Explore related products

What You'll Learn

![]()

Life insurance payouts are generally tax-free

If a life insurance policy is held outside of superannuation, the payout is generally tax-free when paid to nominated beneficiaries. However, if the policy is held inside superannuation, the payout can be taxed at a rate of 30% or more if paid to a financial non-dependent, such as an adult child or business partner. In this case, the beneficiary may be liable for taxes.

It is important to note that there are exceptions to these rules, and the Australian tax system is complex. Therefore, it is always recommended to consult a qualified professional, such as an accountant or financial adviser, when planning how to support your family after your death.

Imputed Life Insurance: Understanding Your Coverage Benefits

You may want to see also

Explore related products

$5.99 $19.99

![]()

Payouts from a personally-held life insurance policy

Your nominated beneficiaries will generally not pay taxes on a life insurance policy held outside of superannuation. However, they might be liable for taxes if your life cover is held inside superannuation and paid to a non-dependent. If there are no nominated beneficiaries on your policy, the death benefit is usually paid to your estate. The payout will then be distributed by the Executor of your Will.

Your beneficiaries might have to pay taxes if:

- Your policy is inside of Super, and your beneficiary(s) are not defined as financially dependent according to the Income Tax Assessment Act 1997. This typically includes children over the age of 18.

- The Executor of your Will holds onto the death benefits after your death. Any interest earned during the holding period could be taxable as part of your beneficiaries' income.

- A third party or business holds the ownership of your life insurance policy.

It is important to note that the Australian tax system is complex, and everyone's situation is different. Therefore, it is always recommended to seek expert advice from an accountant or tax adviser to understand how taxes apply to your specific circumstances.

Understanding Life Insurance: Choosing Your Beneficiaries

You may want to see also

Explore related products

![]()

Life insurance, critical illness and TPD insurance tax deductions

Life insurance, critical illness and total and permanent disability (TPD) insurance premiums purchased outside your superannuation are generally not tax-deductible. However, there are some exceptions.

Life Insurance

Life insurance premiums are generally not tax-deductible, whether purchased inside or outside superannuation. However, if you have a self-managed super fund (SMSF), the trustee (which could be you or someone else) may be able to claim a tax deduction on the premiums.

Critical Illness Insurance

Critical illness insurance, also known as trauma insurance, is also generally not tax-deductible when purchased outside superannuation. However, similar to life insurance, if purchased through an SMSF, the trustee may be able to claim a tax deduction on the premiums.

TPD Insurance

Like life insurance and critical illness insurance, TPD insurance premiums are generally not tax-deductible when purchased outside superannuation. However, if you purchase TPD insurance within your superannuation, it is tax-deductible.

Income Protection Insurance

Income protection insurance is usually tax-deductible, regardless of whether it is purchased inside or outside superannuation. This is because income protection insurance premiums are directly linked to your income.

Life Insurance: A Charitable Legacy Tool

You may want to see also

Explore related products

![]()

Tax on life insurance held inside Super

In Australia, the premiums on life insurance policies through superannuation are generally not tax-deductible, according to the Australian Tax Office (ATO). Super funds typically offer three types of life insurance to their members: life (or death) cover, total and permanent disability (TPD) insurance, and income protection insurance. Each of these types of cover is paid for through deductions from your pre-tax contributions, which have already received favourable tax treatment.

The ATO has ruled that no premiums paid for a life insurance policy that compensates against personal physical injury can be used as a tax deduction. However, it's worth noting that if you have a self-managed super fund (SMSF), the situation may be different and potentially more complex. The ATO states that a deduction may be available to the trustee of a complying super fund for insurance premiums. If your super is structured this way, it's recommended that you consult a financial advisor or tax accountant for specific guidance.

While life insurance benefits are often tax-free when paid out as a lump sum to the policyholder or to a spouse or financially dependent child, there may be tax implications for non-dependent beneficiaries. If the benefit is paid from a policy held within super to a non-financially dependent beneficiary, either as a lump sum or income stream, the beneficiary may be subject to tax on the benefit. Similarly, if the payment is made to a non-dependent beneficiary from a policy within an SMSF, tax implications may arise, as indicated by life insurer NobleOak. In such cases, it is advisable to seek professional advice to navigate the tax complexities.

Life Insurance: Testing for Tobacco and Nicotine

You may want to see also

Explore related products

![]()

Income protection insurance payouts and tax

In Australia, income protection insurance payouts are generally taxed in the same way as income. This means that if you receive income protection insurance payouts, you will need to declare them in your tax return. This is the case whether you receive a regular payment or a lump sum.

The amount of tax you pay is determined by the amount you earn per year and the resulting tax bracket you fit into. The ATO states that you must declare any amounts you receive for lost salary or wages under an income protection, sickness, or accident insurance policy or workers' compensation scheme. This includes any payment received as part of a workers' compensation scheme.

If you have made a personal injury claim and either agree to a settlement or receive a court order in your favour, you may receive compensation in the form of a lump-sum payment, structural (periodic) payments, or both. In this case, the payments may be tax-free if certain conditions are met.

The premiums you pay for income protection insurance are deductible. However, you cannot claim a deduction if the policy is through your superannuation fund and the premiums are deducted from your contributions.

Sarcoidosis: Life Insurance Considerations and Impacts

You may want to see also

Frequently asked questions

Life insurance payouts are generally tax-free, especially when they are going to a financial dependent, such as a spouse or child.

Life insurance payouts can be taxed if they are paid to financial non-dependants, such as a business partner or adult child.

Yes, life insurance held inside superannuation can be taxed at a rate of 30% or more if paid to a non-dependent. Payouts from a personally-held life insurance policy are generally tax-free.

Income protection insurance payouts are usually taxed on a monthly basis.

Life insurance premiums are not usually tax-deductible unless you have a Self-Managed Super Fund.