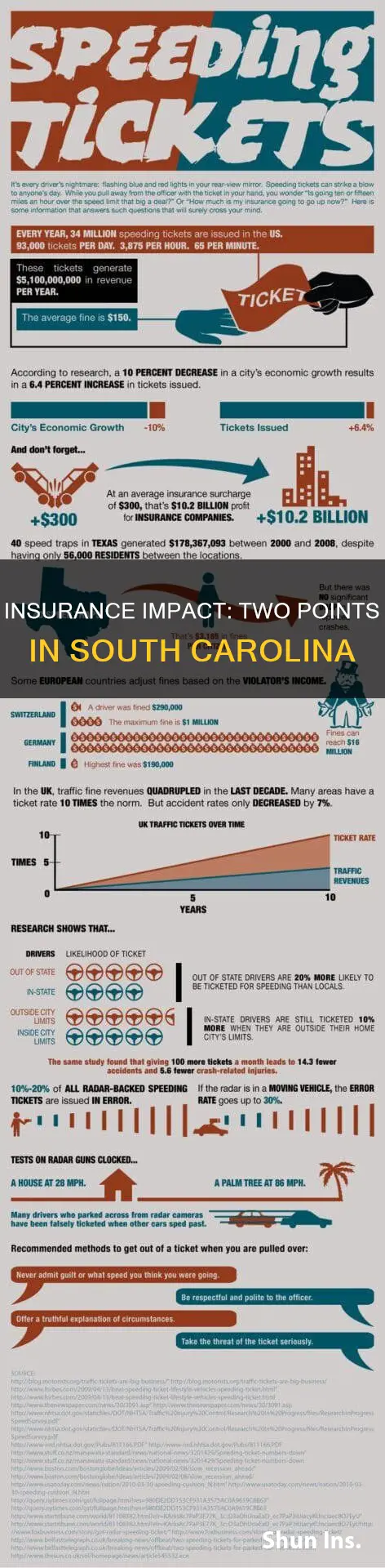

In South Carolina, points on your driving record can lead to higher insurance premiums. While insurance companies do not directly use a driver's license points to determine quotes, they do conduct their own checks into each potential customer's driving history. Speeding tickets can result in two points if you were going less than 10 mph over the limit or cited for too fast for conditions. These points can remain on your record for up to two years, and while they are active, they can contribute to an increase in insurance costs. However, there are ways to reduce the impact, such as taking a defensive driving course or comparing quotes from multiple insurance companies.

| Characteristics | Values |

|---|---|

| Number of points for driving less than 10 mph over the speed limit or for "too fast for conditions" | 2 points |

| Number of points for driving between 11 and 25 mph over the posted limit | 4 points |

| Number of points for driving clocked at 26 mph or more over the limit | 6 points |

| Number of points for a "Super Speeder violation" | Not specified |

| Number of points for a typical speeding ticket | 4 points |

| Number of points leading to a license suspension | 12 points |

| Number of points for license suspension and a Driving Under Suspension ticket | Not specified |

| Time after which points are dropped from the driving record | 2 years |

| Time after which points on the license are cut in half | 1 year |

| Time period for which insurers factor a speeding ticket into the premium | 3 to 5 years |

| Factors affecting insurance premium | Age, driving history, years of driving, past claims, time since the last claim, time since the last ticket |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

Speeding tickets and insurance premiums

Speeding tickets can have a significant impact on insurance premiums. While a single ticket may not always affect your insurance rate, multiple speeding tickets will likely lead to higher premiums. The increase in insurance rates due to speeding tickets can vary depending on several factors, including the number of tickets, the speed over the limit, the time since the last ticket, and state laws.

In South Carolina, speeding tickets come with points that are added to your driving record. The number of points depends on how far over the speed limit you were driving. For example, going less than 10 mph over the limit will result in 2 points, while driving 26 mph or more over the limit will result in 6 points. These points remain on your record for up to two years, and they can lead to an increase in your insurance premiums. Most insurers in South Carolina will factor a speeding ticket into your premium for three to five years, depending on the severity and your overall driving history.

To reduce the impact of speeding tickets on your insurance premiums, you can consider taking a defensive driving course to remove points from your record. Additionally, comparing quotes from multiple insurance companies can help you find a more favourable rate, as insurers may vary in how they treat speeding violations.

It is worth noting that insurance companies in South Carolina also consider other factors, such as credit scores, when determining insurance rates. Improving your credit score and bundling different types of insurance policies under the same provider can help lower your overall insurance premiums.

Commercial Insurance Rates: Post-Loss Adjustments and Impacts

You may want to see also

Explore related products

![Spigen Car Registration and Insurance Card Holder for All Cars [Tesla Model Y Juniper (2025/26) & 3/Y/S/X/Cybertruck] Store Card Keys, ID License Holder, Essential Documents - Black](https://m.media-amazon.com/images/I/61yTRHM9RZL._AC_UL320_.jpg)

![]()

Defensive driving courses

In South Carolina, defensive driving courses are often taken to reduce points on a driver's record and lower insurance premiums. Points can be earned on a South Carolina driver's license for various traffic violations, including speeding. The number of points assigned depends on the severity of the violation, with speeding tickets typically ranging from 2 to 6 points, depending on how far over the speed limit the driver was travelling. These points can lead to higher insurance premiums and even license suspension if too many are accumulated.

Several organisations in South Carolina offer defensive driving courses, including the National Safety Council, DriveSafe Online, and SCDMV-certified driving schools. The National Safety Council offers an 8-hour defensive driving course that is highly interactive and comprehensive. This course is accepted by the South Carolina Department of Motor Vehicles (SCDMV) for point reduction, and successful completion can reduce up to four points from a driver's license. DriveSafe Online also offers a highly-rated defensive driving course that can be completed at the student's own pace and has been known to save drivers hundreds of dollars on their auto insurance annually.

It is important to note that defensive driving courses may not remove all points from a driver's record, and the reduction may only be applied once every three years. Additionally, while these courses can help reduce insurance premiums, insurance companies also consider other factors such as credit scores and driving history when determining rates. Therefore, it is recommended to compare quotes from multiple insurance providers and explore various options for reducing insurance costs.

Auto Glass Repair Billing: Unraveling the Insurance Company's Process

You may want to see also

Explore related products

![]()

Driving record and history

A driving record, also known as an Abstract of Driving Record (ADR), is a history of violations, convictions, collisions, and actions received by a driver over a period of time. These records are confidential and are only provided to those authorized by law, such as insurance companies, employers, and government bodies. While the specific contents of a driving record may vary by state and country, there are some common elements that are typically included.

In the United States, driving records typically include information such as license issuances, exams passed, driver education, and guilty dispositions of traffic violations. The retention period for traffic violations can vary, with most non-moving or moving violations having a retention period of 3 to 5 years, while more serious violations can have retention periods of 10 years, 15 years, or even up to 75 years in some cases. Additionally, driving records may include crash entries when a traffic citation was issued as a result of the crash, as well as open or closed suspensions, revocations, and cancellations.

In some states, such as Florida, driving records also include information on failure to comply (D-6 suspensions), which remain on the record for 1 year from the reinstatement date and are then converted to a correspondence entry for an additional 2 years. Florida also allows individuals to make up to eight traffic school elections within their lifetime and once in a 12-month period to avoid points for traffic citations.

Maintaining a clean driving record is essential for lower auto insurance rates. In some states, such as South Carolina, speeding tickets can add points to your driving record, leading to higher insurance premiums. These points can accumulate quickly and result in license suspension if not managed properly. To remove points from your record, individuals can take defensive driving courses or enroll in traffic education programs, although these options may be limited to once every three years.

In conclusion, a driving record is a comprehensive history of an individual's driving behavior and actions. It plays a crucial role in determining insurance rates and can have significant consequences on driving privileges if not maintained properly. It is important for individuals to understand their driving record and take appropriate steps to ensure a clean record.

Auto Owners: Competitive Insurance Rates?

You may want to see also

Explore related products

![]()

License suspension

In South Carolina, accumulating points on your license can lead to a suspension. While two points can affect your insurance rates in the state, it is not clear if this number of points alone can lead to a license suspension. However, if you accumulate six or more points, your driving privileges will be suspended for six months for excessive points. This is especially true for those holding a beginner's permit, conditional, or special restricted driver's license.

The South Carolina points system aims to encourage problem drivers to improve their driving habits and protect other road users from careless and reckless drivers. By law, certain traffic violations result in points on your driving record. These points are reduced by half after one year from the violation date. For instance, four points received in June would be reduced to two points in the following June.

If you accumulate points, you can take additional driving courses to reduce them. The National Safety Council offers an 8-hour Defensive Driving Course, which can help remove up to four points from your record. However, this course can only be taken once every three years, and completion does not reinstate a suspension for excessive points.

It is important to note that certain violations, such as driving under the influence, carry a mandatory license suspension and are not subject to the point system. Additionally, a “failure to appear” on your driving record can also result in a license suspension, along with potential fines and driving classes.

Metromile Auto Insurance: Available in Arizona?

You may want to see also

Explore related products

![]()

Insurance quotes and comparisons

In South Carolina, two points on your driving record can affect your insurance rates. These points are typically incurred for speeding violations, with the number of points depending on how far over the speed limit the driver was going. While these points typically drop off your record after two years, insurance companies may consider them for up to five years when determining your premium.

To find the best insurance rates, it is important to compare quotes from multiple insurance providers. Online quote-comparison tools, such as Insurify, The Zebra, and Progressive, can help you efficiently compare rates and coverages from various insurers. These platforms often require basic information, such as your address, vehicle details, driving history, and credit score, to generate accurate quotes.

When comparing insurance quotes, it is crucial to ensure that you are providing consistent information across insurers. This includes details about your vehicle, such as its make, model, and year, as well as your driving history, including any accidents. Being honest about any previous claims or motoring offenses is essential, as it can impact your coverage.

Additionally, consider factors beyond just the quoted rate. Insurance companies may offer bundling discounts if you have multiple policies with them, such as home and auto insurance. Your credit score can also influence your premium, with higher scores typically resulting in lower premiums. Furthermore, some companies offer lower rates to policyholders with a college education.

By comparing quotes, coverages, and considering various factors, you can make an informed decision to find the right insurance policy that suits your needs and budget.

How to Get the Best Auto Insurance Coverage

You may want to see also

Frequently asked questions

Yes, having any points on your driving record will likely cause your insurance premiums to increase. While insurance companies do not directly use driver's license points to determine quotes, they do conduct their own checks into each potential customer's driving history, which includes any claims and tickets received.

In South Carolina, points remain on your driving record for up to two years before they are removed. After one year, the points on your license are halved. One way to get points removed more quickly is to take additional driving courses, such as a defensive driving course.

The number of points you get depends on how far over the speed limit you were driving. You will get 2 points if you were going less than 10 mph over the limit or were cited for "too fast for conditions". You will get 4 points for speeding between 11 and 25 mph over the posted limit, and 6 points if you were clocked at 26 mph or more over the limit.

Points remain on your driving record for up to two years before they are removed. After one year, the points on your license are halved.

There are a few ways to potentially get cheaper car insurance in South Carolina. Firstly, you can improve your credit score, as South Carolina companies charge more for car insurance for people with bad credit. Another way is to bundle your home and auto insurance, or another type of policy, under the same provider, as this can often get you discounts.