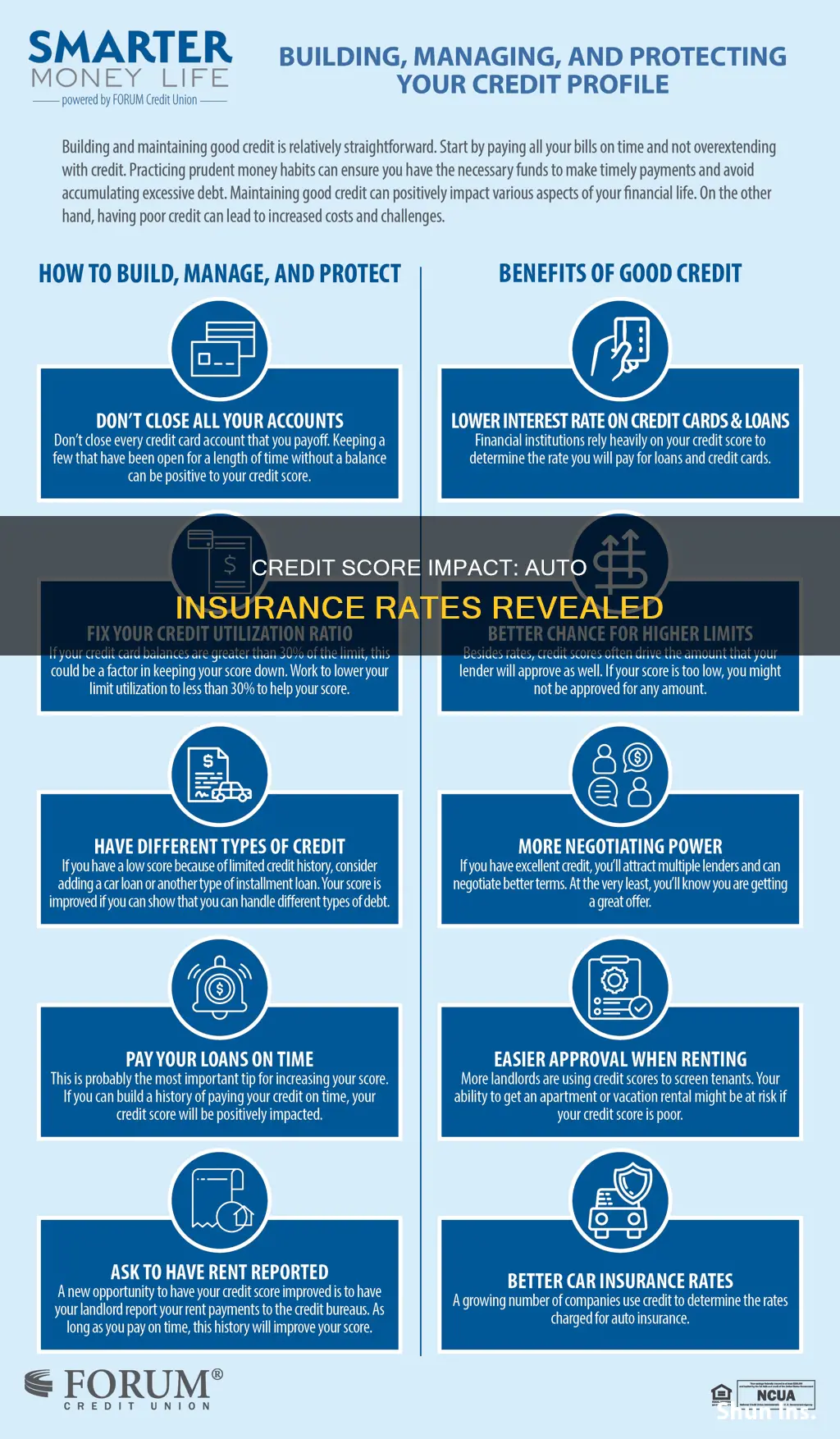

A bad credit score can have a significant impact on automobile insurance rates. While it may not directly affect insurance premiums, it is considered by insurers in most states when determining rates and whether to deny, cancel or refuse to renew a policy. Statistics show that drivers with poor credit are more likely to file claims, resulting in higher rates. Conversely, drivers with good credit may pay lower rates. The impact of a bad credit score on insurance varies across states, with some states banning the use of credit scores in pricing insurance. Improving one's credit score through timely bill payments, minimizing hard inquiries, and responsible credit management can positively influence insurance rates.

| Characteristics | Values |

|---|---|

| Credit score impact on car insurance | Drivers with bad credit pay $166 more per month for full coverage than those with good credit, on average. |

| Credit score impact on insurance premiums | Drivers with poor credit pay 104% more for full coverage car insurance than those with excellent credit. |

| Very poor credit scores | Under 523 |

| Exceptional credit scores | 823 and above |

| Average insurance rate increase for very poor credit scores | $4,581 per year |

| Average insurance rate for very poor credit scores | $6,254 per year |

| Average insurance rate for exceptional credit scores | $1,673 per year |

| Average national credit score | 715 |

| Percentage of people with the worst credit scores | 13% |

| States that ban insurance companies from using credit scores to determine insurance rates | California, Hawaii, Massachusetts, Michigan |

| States that don't allow insurance companies to charge more for a lack of credit history | New Jersey, Rhode Island |

| States where poor credit more than doubles insurance rates | Connecticut, Georgia, Indiana, Kentucky, Maine, Minnesota, Mississippi, Missouri, New Jersey, New York, South Carolina, Texas, Washington D.C. |

| Factors that influence credit-based insurance scores | Payment history, amount owed, length of credit history, mix of credit types, new credit |

Explore related products

What You'll Learn

![]()

Credit scores impact insurance premiums

Insurance companies consider a customer's credit-based insurance score when determining insurance rates. This score is calculated based on the customer's payment history, including the consistency of payments and any delinquencies or late payments. A pattern of late payments or credit delinquencies may signal to insurers a potential risk in financial management and a higher likelihood of claim submissions for minor damages. As a result, customers with poor credit scores may face higher insurance rates as insurers consider them more likely to file claims.

The impact of credit scores on insurance premiums varies across different states and insurance companies. In the United States, four states (California, Hawaii, Massachusetts, and Michigan) have banned insurance companies from using credit scores to determine insurance rates. In these states, companies base rates on driving records, location, and other characteristics. However, in most other states, insurance companies are allowed to consider credit scores when setting insurance premiums. The impact of credit scores on insurance rates also varies among insurance companies, with each company having different ranges for determining rates based on credit scores.

It is important to note that improving overall credit scores may not directly impact insurance scores. However, certain strategies, such as consistently paying bills on time, minimizing hard inquiries on credit reports, and maintaining low credit card balances, can positively impact both credit and insurance scores. These strategies demonstrate responsible financial management, which is favourable to insurers when determining insurance rates.

Auto Insurance Discounts: Who Qualifies and Why?

You may want to see also

Explore related products

![]()

Poor credit raises rates in certain states

A poor credit score can have a significant impact on automobile insurance rates, with drivers with bad credit often paying much higher premiums than those with good credit. This is because insurers consider customers with poor credit scores to be more likely to file claims.

While getting a quote won't affect your credit score, and improving your credit score may not directly impact your insurance score, the two are often linked. Insurers use credit-based insurance scores to determine rates, which take into account factors such as payment history, credit history, and credit mix.

In most states, insurance companies are allowed to consider customers' credit scores when setting rates. However, there are exceptions. Four states—California, Hawaii, Massachusetts, and Michigan—have banned insurance companies from using credit scores to price insurance policies. Instead, companies in these states base rates on driving records, location, and other factors. Some states, like New Jersey and Rhode Island, also prohibit companies from charging higher rates due to a lack of credit history.

Among the states that allow credit to influence insurance rates, the impact of poor credit varies. In Washington, D.C., bad credit drivers pay more than twice as much as those with good credit. Twelve other states—Connecticut, Georgia, Indiana, Kentucky, Maine, Minnesota, Mississippi, Missouri, New Jersey, New York, South Carolina, and Texas—see their rates more than double due to poor credit.

Overall, drivers with poor credit can pay thousands of dollars more per year for car insurance, even with clean driving records. This effect is not limited to a single company, as 92% of insurers consider credit when calculating premiums.

Insurance Rates: What's the Deal?

You may want to see also

Explore related products

![]()

Paying bills on time improves credit scores

A bad credit score can have a significant impact on automobile insurance, with drivers with poor credit scores paying thousands more per year than those with good credit scores, even if they have the same driving record. This is because insurance companies are often free to consider customers' credit scores when determining rates and whether to deny, cancel, or refuse to renew a policy.

Now, onto the impact of paying bills on time on credit scores. Paying bills on time is indeed beneficial for improving credit scores, particularly for credit-related bills. Late payments on credit cards, loans, or mortgages can negatively affect credit scores, although a single late payment is likely to have only a minor impact. Consistent, on-time payments for these credit-related bills will help to boost your credit score over time. However, it is important to note that not all bill payments are treated equally. Non-credit-related bills such as rent, utilities, and medical expenses are generally not reported to credit bureaus and therefore do not directly impact credit scores unless they become very late or go into collections.

While paying bills on time is essential, it is not the only factor that determines your credit score. Credit utilization, or the amount of credit used compared to the total credit available, also plays a significant role. Aiming to use less than 30% of your available credit, and ideally keeping it below 10%, can help improve your credit score. Additionally, it is worth noting that on-time payments on certain types of loans, such as "buy now, pay later" (BNPL), may not always be reported to credit bureaus and may not have a positive impact on your credit score.

To summarize, paying bills on time is crucial for maintaining and improving your credit score, especially for credit-related bills. However, it is just one piece of the puzzle. To achieve and maintain a good credit score, it is essential to also manage your credit utilization effectively and understand the various factors that can influence your credit score.

Amicorp Insurance: Rated and Reviewed in America

You may want to see also

Explore related products

![]()

Credit history is factored into insurance scores

A person's credit score is a crucial factor in many aspects of their financial life. A high credit score can open many doors, while a low score can make everything more difficult and expensive. A credit score is a number that estimates how safe it is for a company to lend money to a person. The higher the score, the more likely a bank will think that the person will pay back the money.

Credit scores are based on five primary factors: payment history, the amount owed, length of credit history, the mix of credit types, and new credit. A pattern of late payments or credit delinquencies might signal to insurers a potential risk in financial management, possibly indicating a higher likelihood of claim submissions for minor damages. A timely payment of bills and consistently paying them on or before the due date can positively impact a person's credit score and, consequently, their insurance scores.

In most states, insurance companies are allowed to consider their customers' credit scores when determining rates and whether to deny, cancel or refuse to renew a policy. Insurance companies generally don't just look at the number on a person's credit score; they consider the full credit report to come up with a credit-based insurance score. This score helps them determine how much of a risk it would be to insure a person's vehicle. Since statistics show that drivers with poor credit are more likely to file claims, they may find that their rate is higher.

However, it is important to note that four states in the US—California, Hawaii, Massachusetts, and Michigan—have banned insurance companies from using credit scores to price or deny insurance policies. Instead, companies in these states base rates on a driver's record, location, and other characteristics.

Mercedes vs Honda: Who Pays More for Insurance?

You may want to see also

Explore related products

![]()

Credit scores impact insurance rates differently

Insurance companies consider your full credit report to come up with your credit-based insurance score. This score helps them determine the risk of insuring your vehicle. Statistics show that drivers with poor credit are more likely to file claims, so they may pay higher rates. Conversely, a driver with good credit may pay a lower rate. The impact of credit scores on insurance rates varies across states. In some states, insurance companies are not allowed to use credit scores to determine insurance rates. Instead, they base rates on driving records, locations, and other characteristics.

Improving your overall credit score may not directly impact your insurance score, but certain strategies can positively affect both. Consistently paying your bills on time and minimizing hard inquiries on your credit report can help improve your credit health and potentially lead to more favorable insurance premium rates. Additionally, keeping your credit card balances low relative to your credit limits can positively impact both your credit and insurance scores.

It is worth noting that insurance companies do not all view credit scores in the same way. Each company has slightly different ranges that they use to base car insurance rates. Therefore, it is essential to shop around and compare rates from different insurance providers.

Auto Club: Home Insurance for Peace of Mind

You may want to see also

Frequently asked questions

Yes, a bad credit score can affect automobile insurance. A higher credit score generally decreases your car insurance rate, with drivers with poor credit paying, on average, $166 more per month for full coverage than those with good credit.

Drivers with bad credit pay, on average, $4,581 more per year than those with good credit. This number varies depending on the state and the insurance company. For example, State Farm has the biggest price hike for bad credit, with drivers paying $406 more per month with a low credit score.

Insurers use a credit-based insurance score to help them determine how much of a risk it would be to insure your vehicle. A pattern of late payments or credit delinquencies might signal to insurers a potential risk in financial management, possibly indicating a higher likelihood of claim submissions for minor damages.

Consistently paying your bills on time and minimising hard inquiries on your credit report can positively impact your credit-based insurance score.

Four states—California, Hawaii, Massachusetts, and Michigan—ban companies from using credit scores to determine insurance rates. Instead, companies in these states base rates on a driver's history, location, and other characteristics.