A certificate of insurance (COI) is a crucial document that provides proof of insurance coverage, outlining key details such as policyholder information, coverage limits, and effective dates. It serves as a snapshot of an insurance policy, often required by businesses, contractors, or clients to verify that adequate insurance is in place. While the exact format may vary by insurer, a typical COI includes the insured party’s name, the insurance company’s details, the type of coverage, policy numbers, and the duration of coverage. Understanding what a certificate of insurance looks like is essential for ensuring compliance and mitigating risks in professional and contractual relationships.

Explore related products

What You'll Learn

![]()

Key Elements on a Certificate

A Certificate of Insurance (COI) is a crucial document that provides proof of insurance coverage. It outlines key details about the policyholder’s insurance policy in a concise and standardized format. Understanding the key elements on a certificate is essential for verifying coverage, ensuring compliance, and protecting all parties involved. Below are the critical components typically found on a COI.

First and foremost, the policyholder’s information is a key element. This section includes the name and address of the individual or entity that holds the insurance policy. It clearly identifies who is insured and ensures that the certificate pertains to the correct party. Additionally, the insured’s contact details may be included to facilitate communication regarding the policy. This information is vital for confirming the identity of the policyholder and ensuring the certificate is valid.

Another essential element is the insurance provider’s details. This includes the name, address, and contact information of the insurance company issuing the policy. It also lists the policy number, a unique identifier for the insurance policy. The policy number is critical for referencing the specific coverage terms and conditions. Alongside this, the effective and expiration dates of the policy are clearly stated, indicating the period during which the coverage is active. These dates are crucial for verifying that the insurance is current and valid.

The type and limits of coverage are also prominently featured on a COI. This section specifies the kinds of insurance provided, such as general liability, property, or workers’ compensation. It details the coverage limits, which define the maximum amount the insurer will pay for a covered claim. For example, general liability coverage might list limits like $1,000,000 per occurrence and $2,000,000 in the aggregate. Understanding these limits is essential for assessing whether the coverage meets contractual or legal requirements.

Lastly, a COI often includes additional insureds and certificate holders. An additional insured is a party that is also covered under the policy, typically added through an endorsement. This is common in contracts where one party requires protection under another’s insurance. The certificate holder, on the other hand, is the entity requesting proof of insurance, such as a client or landlord. Their name and address are listed to confirm that they have been provided with the necessary documentation. Both elements ensure transparency and compliance with contractual obligations.

In summary, the key elements on a certificate of insurance include the policyholder’s information, insurance provider’s details, policy number, coverage dates, type and limits of coverage, and details about additional insureds and certificate holders. These components collectively provide a clear and comprehensive overview of the insurance policy, ensuring all parties can verify coverage and meet their respective obligations. Familiarizing oneself with these elements is essential for effectively using and interpreting a COI.

FEGLI Term Life Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

How to Verify Authenticity

When verifying the authenticity of a certificate of insurance, the first step is to examine the document’s format and design. A legitimate certificate of insurance typically includes a professional layout with the insurer’s logo, contact information, and policy details clearly displayed. Look for consistency in fonts, colors, and branding elements that align with the insurance company’s official materials. Counterfeit certificates often have inconsistencies, such as blurry logos, mismatched fonts, or poor-quality printing. Compare the document to samples available on the insurer’s website or request a template from the company to ensure it matches their standard format.

Next, verify the policy information listed on the certificate. This includes the policy number, effective and expiration dates, coverage limits, and the names of the insured and the certificate holder. Cross-reference these details with any other documentation or agreements you have. For example, if you’re a business owner verifying a contractor’s insurance, ensure the policy dates and coverage types align with the scope of the project. Inconsistencies or missing details could indicate a fraudulent document. Additionally, check for typos or errors in the policyholder’s name or other critical information, as these are common red flags.

A crucial step is to contact the insurance company directly to confirm the certificate’s validity. Use the contact information provided on the certificate or the insurer’s official website—do not rely on contact details given by the person presenting the certificate, as they could be falsified. When calling, provide the policy number and other relevant details to the insurer’s representative. They can verify whether the policy is active, if the coverage matches what’s stated, and if the certificate is genuine. Be cautious if the insurer has no record of the policy or if the contact information leads to an unresponsive or suspicious entity.

Another method to verify authenticity is to check for security features that are common on legitimate insurance certificates. Many insurers include holograms, watermarks, or unique identification numbers to prevent fraud. Hold the document up to the light to look for watermarks or embedded security features. Additionally, some certificates may have QR codes or barcodes that link to the insurer’s verification portal. Scan these codes using a trusted device to confirm the document’s legitimacy. If the certificate lacks these features or they appear tampered with, it may be fraudulent.

Finally, be wary of red flags that suggest the certificate might be fake. These include overly generic language, missing or incomplete information, and pressure from the presenter to accept the document without verification. If the certificate is provided as a digital file, inspect the metadata for signs of recent creation or editing, which could indicate forgery. Trust your instincts—if something feels off, take the time to thoroughly investigate. Remember, verifying authenticity is not just about protecting yourself but also ensuring compliance with legal and contractual requirements.

Navigating New Job Insurance: Must You Wait for Coverage to Begin?

You may want to see also

Explore related products

![]()

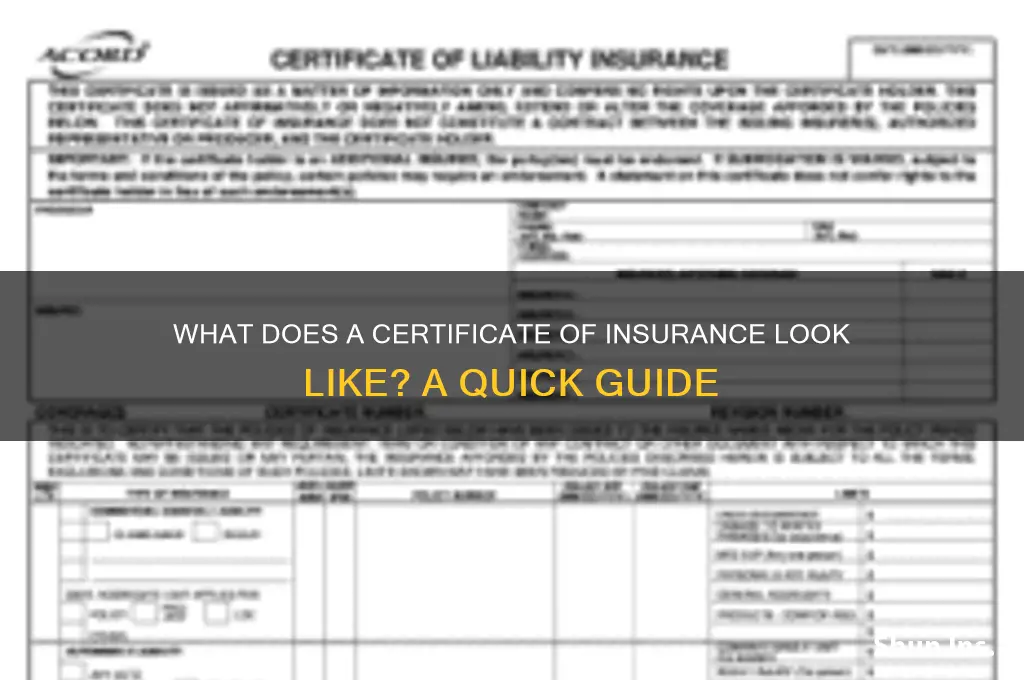

Common Formats and Layouts

When examining the common formats and layouts of a Certificate of Insurance (COI), it’s important to recognize that while the specific design may vary by insurance provider or industry, there are standard elements and structures that most COIs adhere to. Typically, a COI is a single-page document, though it can occasionally span multiple pages depending on the complexity of the coverage. The layout is often clean and professional, with a clear division of sections to ensure readability and accessibility of information. Most COIs follow a top-down or left-to-right flow, starting with the insurance provider’s details and ending with the policy limits and coverage periods.

One of the most common formats includes a header section at the top of the document, which prominently displays the insurance company’s name, logo, and contact information. This section often includes a statement confirming that the document is a Certificate of Insurance, along with a unique certificate number for reference. Directly below this, the insured’s information is listed, including the policyholder’s name, address, and policy number. This ensures that the certificate is clearly tied to the correct individual or entity.

The coverage details are typically presented in a table or list format, with columns or rows dedicated to the type of coverage (e.g., general liability, property, or auto), policy limits, and effective and expiration dates. This section is critical as it outlines the scope of protection provided by the policy. Additional insureds, if any, are often listed here or in a separate section, clearly identifying parties who are also covered under the policy. The layout of this section is usually straightforward, with bold headings and clear delineation between different types of coverage to avoid confusion.

Another standard feature is the declarations or statements section, which includes important disclaimers or notes about the certificate. This may include language stating that the COI is for informational purposes only and does not alter the terms of the policy. It may also highlight that the insurance company is not responsible for updating the certificate if changes occur during the policy period. This section is often placed at the bottom of the document, in smaller font, but remains easily readable.

Finally, the signature or authorization section is a common element in many COIs, though not all certificates include a physical signature. This area confirms the authenticity of the document and may include the name, title, and signature of an authorized representative from the insurance company. In digital formats, this section might instead feature a digital stamp or verification code. The placement of this section varies but is typically found at the bottom of the document, providing a formal closure to the certificate.

In summary, while the exact design of a Certificate of Insurance can differ, the common formats and layouts prioritize clarity, organization, and professionalism. Key sections such as the insurance provider’s details, insured’s information, coverage specifics, declarations, and authorization are consistently included, ensuring that the document serves its purpose effectively. Understanding these standard layouts can help individuals and businesses quickly verify the validity and details of a COI.

Understanding Flexible Variable Life Insurance Policies

You may want to see also

Explore related products

![]()

Differences from Actual Policy

A Certificate of Insurance (COI) and the actual insurance policy serve different purposes and contain distinct information, which is crucial to understand when reviewing coverage. While a COI provides a snapshot of the insurance coverage, it is not a substitute for the detailed terms and conditions outlined in the actual policy. One key difference is that a COI is a concise document, typically one or two pages, summarizing the essential details of the policy, such as the policyholder’s name, policy number, coverage limits, effective and expiration dates, and the types of coverage included. In contrast, the actual policy is a comprehensive, legally binding contract that can span dozens of pages, detailing the rights, obligations, exclusions, and conditions of the coverage.

Another significant difference lies in the level of detail provided. A COI does not include the fine print, exclusions, or specific conditions that govern the policy. For example, it will not list scenarios where coverage is denied, the claims process, or the duties of the insured in the event of a loss. The actual policy, however, contains all these details, ensuring both the insurer and the insured understand their responsibilities. This is why relying solely on a COI can lead to misunderstandings about the extent of coverage, as it does not capture the nuances of the policy terms.

The legal status of these documents also differs. A COI is not a contract and does not confer any rights or alter the terms of the policy. It is merely a proof of insurance, often requested by third parties (e.g., landlords, contractors, or clients) to verify that coverage exists. The actual policy, on the other hand, is the legally binding agreement between the insured and the insurer, outlining the obligations and protections provided. Any disputes or claims must be resolved based on the terms of the policy, not the COI.

Additionally, a COI may not reflect real-time updates to the policy. If changes are made to the policy, such as adjustments to coverage limits or the addition of endorsements, the COI may not immediately reflect these updates. The actual policy is the definitive source of truth for the current terms and conditions of the coverage. Therefore, while a COI is a useful tool for verification, it should not be relied upon as the sole reference for understanding the scope of insurance protection.

Lastly, the intended audience for these documents varies. A COI is designed for third parties who need proof of insurance but are not entitled to the full policy details. The actual policy, however, is intended for the policyholder, who needs to understand their coverage fully to ensure compliance and adequate protection. In summary, while a COI provides a quick overview, the actual policy is the authoritative document that defines the insurance agreement in its entirety.

Who Can Be a Life Insurance Beneficiary: Sibling Edition

You may want to see also

Explore related products

$8.99 $9.54

![]()

Where to Obtain a Copy

If you're looking to obtain a copy of a certificate of insurance, there are several avenues you can explore depending on your role and the type of insurance involved. For policyholders, the most straightforward method is to contact your insurance provider directly. Most insurance companies offer online portals where you can log in to your account and download a copy of your certificate instantly. If you prefer a physical copy, you can request one via email, phone, or mail. Ensure you have your policy number handy to expedite the process. Many insurers also provide mobile apps that allow you to access and share your certificate digitally.

Business owners who require a certificate of insurance from a vendor, contractor, or partner should request it directly from the party in question. It is standard practice for businesses to provide proof of insurance upon request, especially in industries like construction, event planning, or transportation. Be specific about the coverage details you need, such as liability limits or additional insured status, to ensure the certificate meets your requirements. If the party is unwilling or unable to provide the certificate, consider it a red flag and verify their insurance status independently.

Third parties, such as clients or regulatory bodies, can often obtain a certificate of insurance through the insured party’s insurance broker or agent. Brokers typically act as intermediaries and can facilitate the issuance of certificates on behalf of their clients. If you’re working with a broker, provide them with the necessary details, including the name and address of the certificate holder and any specific coverage requirements. Brokers can also assist in verifying the authenticity of a certificate if you receive one directly from the insured party.

In some cases, public databases or online platforms may provide access to insurance certificates, particularly for certain professions or industries. For example, state licensing boards or industry associations may require professionals to submit proof of insurance, which can sometimes be accessed through their websites. However, this is less common and typically limited to specific scenarios. Always ensure the source is reputable and the information is up-to-date.

Lastly, if you’re unsure where to start, consult the contract or agreement that requires the certificate of insurance. Many contracts include clauses specifying how and from whom to obtain proof of insurance. This can save time and ensure compliance with the terms of the agreement. If all else fails, reach out to the party requiring the certificate for guidance on their preferred method of submission or verification.

Whole Life Insurance: What You Need to Know

You may want to see also

Frequently asked questions

A certificate of insurance (COI) is usually a one-page document that includes key details such as the policyholder's name, policy number, coverage limits, effective and expiration dates, and the name of the insurance company.

While there is no universal template, most COIs follow a standardized format, often using the Acord Certificate of Insurance form, which is widely recognized in the insurance industry.

Yes, a COI typically includes sections for policy information, insured and additional insured parties, coverage types, limits, and the signature of the authorized insurance representative.

A COI can be either physical (paper) or digital (electronic). Digital certificates are increasingly common and are considered valid as long as they contain all necessary information and are issued by the insurer.

To verify a COI, check for the insurance company’s contact information, confirm the policy details directly with the insurer, and ensure the document is not expired or altered.