If you are disabled and on Medicare, you may be eligible for supplemental insurance to cover the cost gaps in original Medicare. People with disabilities can be enrolled in Medicare before the age of 65 if they have received Social Security Disability Insurance (SSDI) benefits for 24 months or have specific disabilities such as End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS). Those who qualify for Medicare Part A (hospital insurance) can purchase Medicare Part B (medical insurance). Supplemental insurance options include a Medigap plan or a Medicare Advantage plan, although enrollment restrictions may apply for those under 65. Additionally, Medicaid can serve as supplemental coverage for those who qualify, and some beneficiaries may be eligible for state assistance with expenses.

| Characteristics | Values |

|---|---|

| Who is eligible for Medicare? | People with certain disabilities who are under the age of 65 and have received Social Security Disability Insurance (SSDI) benefits for 24 months or have End Stage Renal Disease (ESRD) or Amyotropic Lateral Sclerosis (ALS). |

| Requirements for Medicare eligibility for people with ESRD and ALS | ESRD – Generally eligible 3 months after a course of regular dialysis begins or after a kidney transplant; ALS – eligible immediately upon collecting SSDI benefits. |

| Enrollment period for buying Supplemental Medical Insurance | During the initial enrollment period (the month they are notified about the end of premium-free health insurance and the following seven months); during the annual general enrollment period (January 1 through March 31 of each year); or during a special enrollment period if covered under an employer group health plan. |

| Supplemental insurance options | Medigap (enrollment may be limited for people under 65); Medicare Advantage plan; Medicaid; or a Marketplace plan (but this will result in losing any premium tax credits and other savings for the Marketplace plan). |

| Cost considerations | Medicare Part A (hospital insurance) is premium-free; Medicare Part B (medical insurance) coverage requires premiums or co-pays, unless covered by an employer's insurance. |

Explore related products

What You'll Learn

![]()

Eligibility criteria for people with disabilities

Medicare

Medicare is available for certain people with disabilities who are under 65. To be eligible for Medicare before turning 65, individuals must meet one of the following criteria:

- Receive Social Security Disability Insurance (SSDI) benefits for 24 months.

- Have End-Stage Renal Disease (ESRD).

- Have Amyotrophic Lateral Sclerosis (ALS), also known as Lou Gehrig's disease.

For individuals with ESRD, Medicare eligibility generally starts three months after the initiation of regular dialysis or a kidney transplant. For those with ALS, Medicare coverage begins immediately upon collecting Social Security Disability benefits. People who meet the criteria for Social Security Disability are typically automatically enrolled in Medicare Parts A (hospital insurance) and B (medical insurance).

It is important to note that there is a five-month waiting period after an individual is deemed disabled before they can begin collecting Social Security Disability benefits. During this 24-month qualifying period, beneficiaries may be eligible for health insurance through a former employer.

Medicaid

Medicaid can act as supplemental insurance to cover out-of-pocket costs for those who qualify for low-income benefits. Eligibility rules for Medicaid vary by state. In some states, individuals who receive Supplemental Security Income (SSI) Disability may automatically receive Medicaid coverage, while in other states, they may need to apply.

Medigap

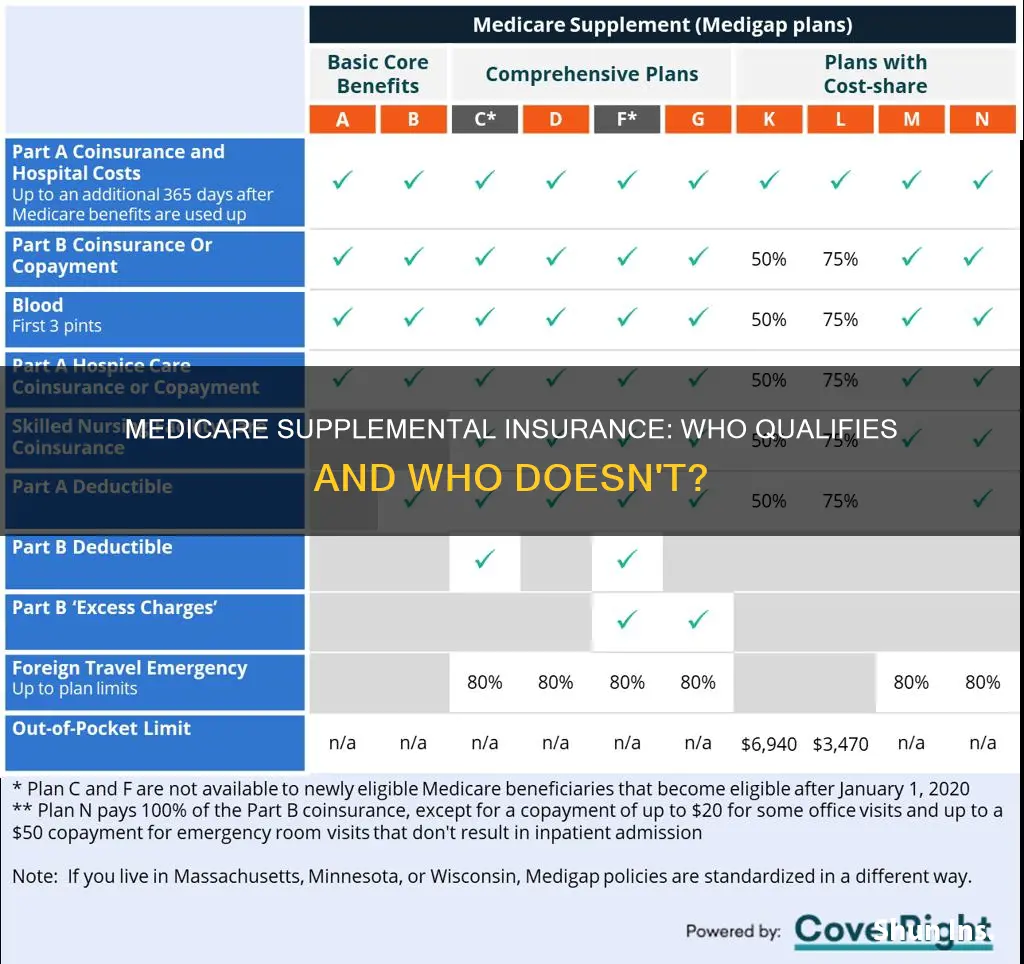

Medigap is a supplemental policy that helps cover the cost gaps in original Medicare. Enrollment in Medigap plans for individuals under 65 is limited in many states.

Medicare Advantage

Medicare Advantage is a privately managed health plan that typically covers all services, including prescription drug coverage. This can be an option for individuals without employer insurance or those seeking to cover cost gaps in original Medicare.

Supplemental Insurance through an Employer

Individuals with disabilities can also obtain supplemental insurance through their employer. If an individual's employer has more than 100 employees, they are required to offer health insurance to individuals and spouses with disabilities. Medicare will be the secondary payer in this case. For smaller employers offering health insurance to persons with disabilities, Medicare will be the primary payer.

Quality Insurance: Medical Care's Future

You may want to see also

Explore related products

![]()

Purchasing supplemental insurance

Supplemental insurance is additional insurance that can be purchased to help pay for services and out-of-pocket expenses not covered by your regular major medical health insurance. This includes deductibles, copayments, and coinsurance. Some supplemental insurance plans will pay for out-of-pocket costs associated with your health insurance plan, while others may provide you with a cash benefit paid out over time or as a lump sum. This cash benefit can be used for expenses such as food, housing, and childcare.

Medicare Supplement Insurance, or Medigap, is a type of supplemental insurance that helps pay for out-of-pocket costs in Original Medicare (Part A and Part B). Generally, you must have Original Medicare to buy a Medigap policy. However, it's important to note that Medigap plans might not be available to individuals under 65 who are enrolled in Medicare due to a disability, depending on their location. Additionally, only Medigap plans C and F cover the Part B deductible, and these plans are only available to individuals who became eligible for Medicare before 2020.

When considering purchasing supplemental insurance, it's important to evaluate your current health insurance coverage, the deductible amount, and your specific needs. Supplemental insurance can provide additional peace of mind and help with out-of-pocket medical expenses. However, it's essential to understand the limitations and benefits of any policy before purchasing it, as duplicate coverage may be unnecessary in some cases.

Individuals with disabilities who are eligible for Medicare can consider purchasing supplemental insurance to enhance their coverage. Medicare Part A (Hospital Insurance) is premium-free for those who qualify, while Part B (Medical Insurance) typically requires premiums. If an individual's employer has more than 100 employees, the employer is required to offer health insurance to individuals with disabilities, and Medicare will be the secondary payer. Supplemental insurance can be purchased at any time of the year, and there are various options available, such as Medigap policies, Marketplace plans, and private health insurance plans.

Medical Insurance in MS: Average Costs Explored

You may want to see also

Explore related products

![]()

Supplemental insurance for low-income beneficiaries

Supplemental insurance can be purchased by those who qualify for Social Security Disability Insurance (SSDI) benefits. This includes people with disabilities who are under 65 and have received Social Security Disability benefits for 24 months, or have End Stage Renal Disease (ESRD) or Amyotropic Lateral Sclerosis (ALS). There is a 24-month waiting period for Medicare coverage after the beneficiary is determined to be disabled.

Medicare Part A (Hospital Insurance) is premium-free for those who qualify. However, Medicare Part B (Medical Insurance) requires the beneficiary or a third party to pay premiums. Supplemental insurance, or Medigap, can be purchased from a private health insurance company to help cover out-of-pocket costs. To purchase a Medigap policy, one must already have Medicare Part A and Part B.

Low-income beneficiaries may be eligible for state assistance with the cost of supplemental insurance. Additionally, Medicaid and the Children's Health Insurance Program (CHIP) provide free or low-cost health coverage to low-income individuals, including those with disabilities. Eligibility for Medicaid is generally based on income, with mandatory coverage for low-income families, pregnant women, children, and individuals receiving Supplemental Security Income (SSI).

Some states have expanded their Medicaid programs to cover nearly all low-income Americans under 65, while others have implemented additional state-only programs to assist certain low-income individuals who do not qualify for Medicaid. Furthermore, those who qualify for Medicaid may also be eligible for savings on a Marketplace plan, which can provide access to private health insurance at very low premiums and out-of-pocket costs.

Understanding Medical Insurance Surcharges: What You Need to Know

You may want to see also

Explore related products

![]()

Supplemental insurance through Medicaid

Supplemental insurance, also known as Medigap, is private health insurance designed to supplement Original Medicare. Medicare is available for certain people with disabilities who are under 65. These individuals must have received Social Security Disability Insurance (SSDI) benefits for 24 months, have End-Stage Renal Disease (ESRD), or Amyotrophic Lateral Sclerosis (ALS).

Medicaid, on the other hand, is a joint federal and state program that helps cover medical costs for people with low incomes, including those with disabilities. It is important to note that the rules for eligibility vary by state, and are generally based on income and household size.

If an individual has both Medicare and qualifies for full Medicaid coverage, they are considered ""dually eligible." In this case, Medicare pays first for Medicare-covered services, and Medicaid pays last, covering any remaining costs. Medicaid may also pay for other drugs and services that Medicare does not cover.

For those with Medicare who are considering a Medicare Supplement Insurance plan, it is generally discouraged due to the potential for redundancy in coverage. However, Medicaid and Medicare serve different purposes and populations, and can work together to provide comprehensive coverage for individuals who qualify for both.

In conclusion, while not everyone who is disabled and on Medicare will qualify for supplemental insurance, they may be eligible for Medicaid, which can provide additional coverage and benefits.

Accessing Prescribed Medication: Options Without Health Insurance

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Employer-provided supplemental insurance

Supplemental insurance is an additional insurance policy that provides extra coverage for specific situations not covered by a primary insurance plan. It is designed to fill in the gaps in an individual's primary insurance coverage and ensure they have more comprehensive protection. While Medicare provides health insurance coverage for people with disabilities, not all disabled individuals are eligible for Medicare. To qualify for Medicare, individuals under 65 must have received Social Security Disability Insurance (SSDI) benefits for 24 months, with some exceptions for those with End Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS).

Employers play a significant role in providing supplemental insurance options for their employees, which can be highly beneficial for individuals with disabilities. Here are some key points regarding employer-provided supplemental insurance:

Availability of Supplemental Insurance Plans: Employers often offer supplemental insurance plans as a benefit to their employees. These plans can include various options, such as short-term disability coverage, critical illness insurance, accidental injury coverage, and hospital care plans.

Cost-Effectiveness and Financial Support: Supplemental health benefits can provide cost-effective solutions for employees and their families. They offer financial support to help employees manage healthcare expenses and bounce back from health setbacks. This financial assistance is highly valued by employees and can enhance their overall well-being.

Personalized Health Support: Supplemental insurance plans can provide personalized health support to employees after an illness or injury. This support may include assistance with navigating the healthcare system, finding appropriate treatment options, and managing financial challenges related to their medical conditions.

Seamless Claims Processing: Some supplemental insurance providers offer streamlined claims processing, eliminating the need for employees to initiate multiple claims for different types of coverage. This simplifies the process for employees dealing with short-term disability, paid family leave, or state-mandated disability claims.

Group Rates and Discounts: Employers may be able to negotiate group rates and discounts for supplemental insurance plans, making these policies more affordable for employees. Group plans can also provide comprehensive coverage for employees and their families under one convenient umbrella.

Specialized Coverage: Certain supplemental insurance plans offer specialized coverage for specific situations. For example, coverage for preventive measures related to genetic mutations like BRCA1 or BRCA2, or earlier payouts for conditions like Alzheimer's, multiple sclerosis, and Parkinson's disease.

In summary, employer-provided supplemental insurance plans offer valuable additional coverage for employees with disabilities. These plans can provide financial support, personalized health assistance, streamlined claims processing, and specialized coverage for specific health needs. When considering supplemental insurance options, employees should review the specific benefits offered by their employers and choose the plans that best meet their individual needs and provide the most comprehensive protection.

Should You Retain or Cancel Old Medical Insurance?

You may want to see also

Frequently asked questions

Not everyone disabled and on Medicare will qualify for supplemental insurance. If you have a disability and are enrolled in original Medicare (Parts A and B), you may want additional coverage. You can get this through an optional supplemental policy to cover the cost gaps in original Medicare, such as a Medigap or Medicare Advantage plan. However, enrollment in Medigap is limited for people under 65 in many states.

To be eligible for Medicare before the age of 65, you must have received Social Security Disability Insurance (SSDI) benefits for 24 months, have End-Stage Renal Disease (ESRD), or Amyotrophic Lateral Sclerosis (ALS), also known as Lou Gehrig's disease. People with ESRD and ALS are exempt from the 24-month waiting period.

Yes, as long as your disabling condition still meets the requirements. If you purchase Part A, you may also purchase medical insurance (Part B).

Yes, you can sign up for Part B during a general enrollment period (January 1st through March 31st of each year) or a special enrollment period.