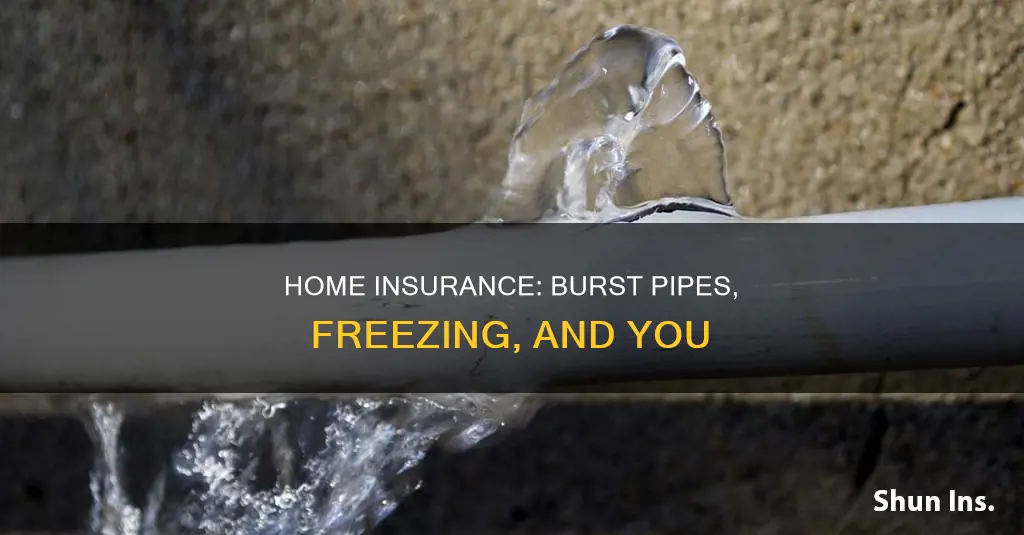

Homeowners insurance policies typically cover burst pipes, including those that have frozen, under certain conditions. Most policies cover sudden and accidental water damage that results from plumbing fixture failure or a burst pipe. However, insurance companies may deny claims if they determine that the damage resulted from negligence, such as failing to maintain heat in the property or properly maintain pipes. It is important to review your specific policy to understand the exclusions and circumstances under which coverage may apply. In the event of a burst pipe, it is recommended to act swiftly by turning off the water supply, cleaning up the water, documenting the damage, and contacting your insurance company for guidance on the claims process.

| Characteristics | Values |

|---|---|

| Coverage | Damage from burst pipes is usually covered if the policy contains the following or similar language: "Coverage is provided when it is determined damage resulted from a 'sudden and accidental' discharge from a plumbing source or system." |

| Caveats | Your insurance policy may not respond if it appears you neglected to take the proper steps to safeguard your property. Your policy usually requires that heat be maintained within the property, and some policies require that you maintain a certain temperature, even if the property is vacant, occupied or unoccupied. |

| Loss of use coverage | Loss of use coverage, also known as additional living expenses insurance, can help pay for the additional costs you incur for reasonable housing and living expenses if a covered event makes your house temporarily uninhabitable while it's being repaired or rebuilt. |

| Personal property coverage | Your personal property coverage protects the belongings in your home, like clothes, furniture, appliances, and electronics. |

| Dwelling coverage | The dwelling portion of your home insurance policy protects the structure of your home, such as carpeting, flooring, and walls. |

Explore related products

What You'll Learn

![]()

Home insurance covers burst pipes from freezing

Home insurance typically covers burst pipes from freezing. However, this depends on the specific circumstances and the terms of your policy. Most homeowner and commercial property insurance policies cover damage from frozen pipes that burst. This coverage usually applies when the damage is deemed "sudden and accidental", resulting from a plumbing source or system.

It is important to note that insurance policies may not provide coverage if it is determined that proper steps were not taken to safeguard the property. For example, if you turned off the heat when leaving your house for several days, causing the pipes to freeze, your claim may be denied due to negligence. Insurance companies often require maintaining heat within the property, and some policies specify maintaining a certain temperature even when the property is vacant or unoccupied.

In the event of a burst pipe, it is crucial to act swiftly. Turn off the main water valve to minimise damage, then call a plumber to address the issue promptly and effectively. Take pictures and create a detailed list of items that require repairs or replacements, including their brand, price, and other pertinent information. Contact your homeowners insurance company, and they will guide you through the claims process and explain the applicable coverages.

Additionally, loss of use coverage, or additional living expenses insurance, can help cover the costs of temporary housing and living expenses if your home becomes uninhabitable during repairs. This coverage can include expenses such as hotel stays and pet boarding while your home is being restored.

While home insurance typically covers water damage from burst pipes, it is important to review your specific policy for exclusions and circumstances where they may apply. Some policies may not cover the cost to repair the broken section of the pipe itself, and separate insurance policies or add-ons may be necessary for protection against flooding, backup, or sump pump failure.

Citations and Insurance: When to Report and Why

You may want to see also

Explore related products

![]()

But not if you neglected to take proper precautions

Homeowners insurance typically covers water damage and repairs due to a burst pipe. However, this assumes that reasonable care was taken to prevent such an incident. If it is determined that the damage was caused by negligence, your insurance provider may deny your claim.

For example, if you leave your house for a few days and do not turn on the heat in freezing weather, causing the pipes to freeze, your insurance claim may be rejected. This is because you did not take the proper precautions to safeguard your property. Most policies require that heat be maintained within the property, and some even stipulate a minimum temperature.

Additionally, if your pipes did not receive proper maintenance, your insurance claim may also be denied. This includes situations where you failed to shut off the water supply and drain the system when the property was vacant or unoccupied. Pipe and appliance maintenance are generally the responsibility of the homeowner.

To prevent frozen pipes and potential water damage, there are several precautions you can take. Firstly, ensure that you maintain a sufficient level of heat within your property, especially when it is vacant or unoccupied. Secondly, consider installing water sensors, which can help prevent costly water damage by detecting leaks early on. Finally, when preparing your home for colder weather, remove garden hoses from outdoor water faucets, cover exterior faucets with inexpensive faucet covers, and insulate pipes near crawl spaces, attics, and exterior walls.

Ring Insurance: Is Peace of Mind Worth the Cost?

You may want to see also

Explore related products

![]()

You may need to prove you maintained heat in the property

Homeowner's insurance policies typically cover damage from burst pipes. However, your insurance policy may not respond if you neglected to take the necessary precautions to safeguard your property. Most policies require that heat be maintained within the property, and some even stipulate a minimum temperature.

If you turned off the heat when leaving your house for a few days, causing the pipes to freeze, your insurance claim may be rejected. To prevent this, you can take several precautions, such as setting your thermostat to a minimum of 55°F when you are away from home. If you plan to be away for an extended period, consider asking a friend or relative to check on your house and ensure the heat is functioning correctly.

In the case of Zimmerman v. Leatherstocking Coop. Ins. Co., the insurer argued that the homeowner failed to use reasonable care to maintain heat, citing insufficient electricity and gas usage as proof. The court refused to grant summary judgment, emphasizing that determining reasonable care is dependent on the specific circumstances of each case.

To ensure your insurance claim is successful, it is essential to review your policy carefully and take the necessary steps to maintain heat and protect your pipes.

Valife Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Or that you shut off the water supply and drained the system

Homeowner's insurance typically covers burst pipes resulting from freezing temperatures. However, insurance policies may deny coverage if proper precautions, such as maintaining heat within the property, were not taken. To prevent burst pipes due to freezing, it is essential to shut off the water supply and drain the system.

Shutting off the water supply is a crucial step in preventing further damage and giving you time to call a licensed plumber for repairs. The first step is to locate the main water shut-off valve, typically found near the meter. Once located, switch off the main water supply. It is important to ensure that the water supply has been successfully turned off by turning on a tap inside your home and checking if water still flows. If the water continues to leak, there may be an issue with the pipe insulation or installation, and a plumbing service should be contacted.

After shutting off the water supply, the next step is to drain the system. Open the lowest cold-water taps to drain any remaining water. Additionally, flush all toilets to drain the water from the cisterns. If you have a hot water system, turn off the electrical power or gas supply to the unit before draining the hot water taps.

Taking these steps to shut off the water supply and drain the system can help prevent burst pipes and minimize damage in the event of freezing temperatures. It is also important to regularly inspect your pipes for any signs of unusual water pressure or unusual noises, such as hissing or gurgling, which could indicate a blocked or burst pipe.

By being proactive and taking preventative measures, you can reduce the risk of costly water damage and the stress associated with plumbing emergencies. Knowing how to respond during a plumbing emergency is crucial for safeguarding your property and ensuring your peace of mind.

Stay Vigilant: Report Health Insurance Fraud

You may want to see also

Explore related products

![]()

Loss of use coverage can help pay for additional living expenses

Loss of use coverage, also known as additional living expenses (ALE) insurance, is a standard part of most homeowners insurance policies. It can help pay for additional living expenses incurred if your home is damaged by an insured event and becomes uninhabitable while it's being repaired or rebuilt. This coverage is designed to help you maintain your standard of living and cover costs you wouldn't ordinarily have if you were living in your own home.

For example, if a burst pipe has caused covered damage to your home, making it unlivable, loss of use coverage can help offset costs such as hotel expenses, home rentals, and boarding for your pet while repairs are being made. It can also cover additional food expenses, such as eating out more often due to a lack of kitchen access. It's important to note that loss of use coverage does not reimburse expenses you were already responsible for before the loss, such as your mortgage, insurance, or childcare expenses.

The amount of coverage provided by loss of use protection varies by insurance company and policy. Typically, it is offered as a percentage of your dwelling coverage. For example, if your dwelling coverage limit is $200,000 and your loss of use coverage limit is 30%, you would be covered for up to $60,000. You may also be responsible for a deductible for this coverage, so it's important to review your policy carefully.

To make a claim under loss of use coverage, you will typically need to submit receipts for your additional living expenses to your insurer for review. It's also a good idea to contact your insurance company if you need assistance finding temporary housing, as they may be able to help. While loss of use coverage can provide valuable financial support during a difficult time, it's important to remember that it may not cover all your additional expenses, and you may still need to pay for certain costs out of pocket.

Home Insurance: Whose Name Matters?

You may want to see also

Frequently asked questions

Yes, your homeowners insurance will likely cover burst pipes from freezing. This includes the cost of cleaning and necessary repairs due to water damage.

Homeowners insurance does not cover the cost of repairing the section of the broken pipe. It also does not cover water damage resulting from sewage backup, sump pump failure, or slow leaks that happen over more than a week.

First, turn off your water supply immediately to prevent additional damage. Then, contact a water restoration company or a plumber to make the necessary repairs. Take pictures of the damage and create a list of items that need repair or replacement. Finally, contact your homeowners insurance company.

Yes, loss of use coverage, also known as additional living expenses insurance, can help pay for reasonable housing and living expenses if your house is temporarily uninhabitable due to a covered event.

It depends. If you did not take the proper steps to safeguard your property, such as draining the pipes and shutting off the water supply, your insurance policy may not cover the damage.